Educational only: This guide summarizes SSA, IRS, Morningstar, and Investor.gov material in general terms and is not financial, tax, or legal advice. Withdrawal-rate figures are research frameworks, not personal instructions. Customers should speak to a financial or tax advisor before making decisions. Goldco does not offer tax or legal advice. Past performance does not guarantee future results.

Quick Answer: What Makes a Retirement Portfolio Last?

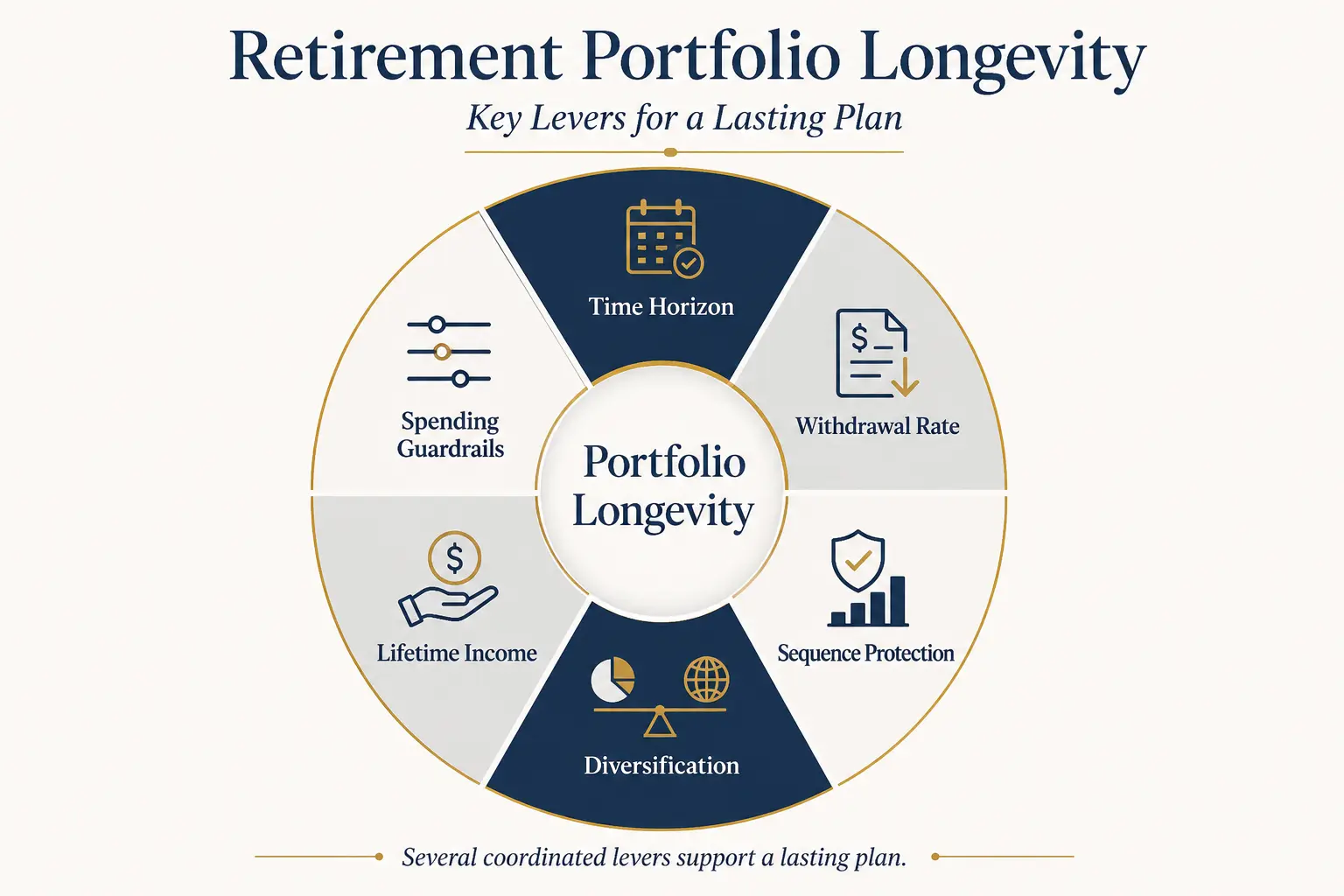

A retirement portfolio has a better chance of lasting when the plan uses a realistic time horizon, begins with a measured withdrawal rate, keeps enough growth assets for a long retirement, holds stabilizing assets for near-term spending, and allows modest spending changes after weak markets. The highest-priority levers are:

- Plan for a long horizon. Average life expectancy is a reference point, not an expiration date.

- Set a starting withdrawal rate from the full plan. Portfolio size, retirement length, taxes, pensions, Social Security, and spending flexibility all matter.

- Protect the early retirement years. Large losses near the start of withdrawals can do more damage than similar losses much later.

- Diversify the retirement asset allocation. Stocks, bonds, cash, and other assets can serve different jobs.

- Match stable income to essential costs. Social Security, pensions, and selected lifetime-income products can reduce pressure on the portfolio.

- Use spending guardrails. Smaller raises or temporary reductions can preserve assets after weak returns.

- Coordinate required minimum distributions and taxes. The required withdrawal is a tax rule, not a personalized spending target.

The Gold IRA Calculator can help organize precious-metals research, but it should sit inside a broader retirement-income plan rather than act as the plan itself.

Retirement Portfolio Longevity Starts With the Time Horizon

Longevity risk is the chance that retirement lasts longer than the financial plan expected. The correct response is not alarm — it is a planning horizon that leaves room for a long life. The Social Security Administration's 2023 period life table, used in the 2026 Trustees Report, shows average remaining life expectancy at age 65 of 18.12 years for males and 20.66 years for females. At age 70, the averages are 14.66 and 16.76 years. These figures describe averages under 2023 mortality rates, not the maximum length of an individual retirement (Social Security Administration).

A household may need a longer horizon than either individual average because the portfolio may need to support the surviving spouse. Health, family history, retirement age, and the desire to leave assets can also change the useful planning period. A retiree leaving work at 60 may test a 35- or 40-year horizon; a retiree starting at 70 may test a shorter base case while still allowing for life into the 90s. These are planning choices, not predictions. A practical longevity review asks how many years the portfolio should cover under a base case, what happens if retirement lasts five or ten years longer, which expenses continue for a surviving spouse, which costs rise faster than general inflation, which income sources continue for life, and which spending categories can change if returns disappoint. The answer to "how long will retirement savings last?" therefore comes from scenarios rather than one date.

The Withdrawal Rate: The 4 Percent Rule, Its Critics, and Dynamic Alternatives

The 4 percent rule is a planning framework, not a promise. The classic approach begins by withdrawing 4% of the starting portfolio in the first year, then adjusting that dollar amount for inflation in later years. Morningstar's discussion of withdrawal research notes that the framework traces to William Bengen's 1994 historical analysis (Associated Press, citing Morningstar). The framework is useful because it connects portfolio size with first-year spending: a $1 million portfolio produces a $40,000 first-year withdrawal at 4%, before taxes and outside income, and a $750,000 portfolio produces $30,000. Its weakness is that the result depends on assumptions — retirement length, stock and bond returns, inflation, allocation, fees, taxes, and spending behavior can all change portfolio survival.

Morningstar's 2024 research, published for 2025 planning, estimated a 3.7% starting rate for fixed inflation-adjusted withdrawals, a 30-year horizon, and a 90% modeled success rate. The estimate applied to portfolios with 20% to 50% in stocks under Morningstar's forward-looking return assumptions, and Morningstar stated the result was a baseline rather than an automatic rate for every retiree (Morningstar; Morningstar). A longer horizon usually supports less initial spending under the same model — Morningstar reported a 3.1% highest starting rate for a 40-year horizon in its fixed-real-spending base case. These research figures should be treated as frameworks, not personal instructions.

Fixed real spending starts with one dollar amount and raises it with inflation, creating smoother spending but ignoring portfolio conditions. Percentage-of-portfolio spending withdraws a set share of the current balance — it cannot drain the portfolio the same way as a fixed dollar rule, but annual income can move sharply. Spending guardrails set upper and lower boundaries: spending may rise after strong growth and pause or decline when withdrawals become too large relative to the balance. Morningstar found that flexible systems, including skipping an inflation raise after a losing year and using formal guardrails, supported higher modeled starting or lifetime withdrawals than its fixed-real base case, with the trade-offs being more year-to-year cash-flow variation and often smaller ending balances. A practical spending policy can divide expenses into three groups — essential (housing, food, insurance, utilities, core healthcare); important but adjustable (travel, gifts, hobbies, home projects); and optional (large discretionary purchases and upgrades) — which makes a temporary spending change easier to apply without treating every market decline as a financial emergency.

Customers should speak to a financial or tax advisor before making decisions about withdrawal rates, portfolio allocation, IRA distributions, or tax treatment. Goldco does not offer tax or legal advice. The 4 Percent Rule and Gold IRA guide provides a related review of withdrawal-rate assumptions.

Sequence-of-Returns Risk: Why the First Years Matter Most

Average return does not fully explain portfolio longevity during withdrawals. Sequence-of-returns risk occurs when poor market results arrive early in retirement — early losses reduce the balance while withdrawals continue, leaving fewer assets available for a later recovery. Morningstar describes this as a key risk for new retirees and notes that spending adjustments after weak markets can leave more of the portfolio available to recover (Associated Press, article provided by Morningstar). The order of returns matters because withdrawals remove shares: a market decline without withdrawals can recover if enough time remains, but a decline combined with withdrawals may require selling more shares at lower prices.

Several tools can reduce sequence risk: keep near-term withdrawals in cash or high-quality short-term bonds; rebalance from assets that have held up rather than automatically selling the weakest holding; skip an inflation raise after a negative portfolio year; delay a major optional purchase; use stable income for essential expenses; start with a lower withdrawal rate when the retirement horizon is long; and maintain enough growth exposure to support later decades. A cash reserve has a cost because cash may earn less than long-term growth assets — too much cash can increase inflation risk, too little can force sales after a market decline, and the useful amount depends on spending needs, other income, risk capacity, and allocation. The Need Cash From a Gold IRA guide explains why liquidity and distribution planning matter before retirement assets are needed.

Asset Allocation and Diversification for Portfolio Survival

Retirement asset allocation should balance three jobs: current spending, stability, and long-term growth. Cash and short-term bonds can fund near-term needs; high-quality bonds can reduce volatility and provide income; stocks can support growth over a long retirement but can produce large short-term losses. Investor.gov explains that diversification spreads exposure across investments — it cannot eliminate losses during a broad market decline, but it may reduce the damage compared with a concentrated portfolio (Investor.gov). Diversification in retirement should be tested across asset classes, industries, company sizes, U.S. and international markets, bond maturities and credit quality, taxable/tax-deferred/Roth accounts, liquid and less-liquid holdings, and sources of retirement income.

Where Precious Metals May Fit

Precious metals can be one diversification lever. They do not create income, and prices can be volatile; physical holdings can also involve premiums, storage, insurance, and transaction spreads. The World Gold Council, an industry organization, argues that gold can complement stocks and bonds by adding diversification and liquidity, but its 2026 research does not establish one allocation that fits every retiree (World Gold Council). A modest precious-metals position may be evaluated beside cash, bonds, stocks, Treasury Inflation-Protected Securities, real estate, and other diversifiers — the relevant test is whether the position improves the full portfolio's risk, liquidity, cost, and withdrawal plan. No "optimal" gold percentage was verified from a neutral primary source that fits every retiree; allocation should reflect the household's objectives, time horizon, other assets, income sources, and capacity for price swings. The How Much Gold Should Be Held in Retirement guide and Gold Allocation Backtest can support scenario research without replacing professional advice. Customers should speak to a financial or tax advisor before making decisions about retirement asset allocation, IRA holdings, or precious-metals exposure. Goldco does not offer tax or legal advice.

Lifetime-Income Products and Spending Guardrails

Stable income can lower the amount that must come from the portfolio. Social Security and pensions may cover part of essential spending, and some retirees also evaluate annuities or other lifetime-income products. Investor.gov describes an annuity as a contract with an insurance company that may provide periodic payments immediately or later; contracts can differ in costs, risks, features, surrender terms, and tax treatment, and the insurer's obligations depend on its financial strength and claims-paying ability (Investor.gov). A lifetime-income product can transfer part of longevity risk to an insurer, with trade-offs that may include lower liquidity, reduced access to principal, contract complexity, fees, inflation exposure, and less money left for heirs.

A practical income-floor process can estimate essential annual expenses, subtract Social Security and pension income, identify any remaining essential-income gap, compare a bond ladder / cash reserve / annuity / portfolio withdrawals for that gap, and keep flexible spending separate. Morningstar reported that stable income sources can help support flexible spending systems because they reduce dependence on portfolio withdrawals in weak markets (Morningstar). Spending guardrails can then apply mainly to optional expenses: a retiree may pause inflation increases, reduce travel, or delay a vehicle purchase when the portfolio crosses a lower boundary, while strong years may allow measured increases without turning one year of growth into a permanent spending commitment.

Required Minimum Distributions and Tax-Aware Withdrawal Ordering

Required minimum distributions affect cash flow and taxes, but they do not set a personalized spending rate. The IRS states that owners generally must begin RMDs from traditional IRAs, SEP IRAs, SIMPLE IRAs, and retirement plans at age 73; workplace-plan participants may delay plan RMDs until retirement unless they own 5% of the sponsoring business, and Roth IRAs and designated Roth accounts do not require owner-lifetime RMDs, although beneficiaries are subject to distribution rules (Internal Revenue Service). The IRS calculates an RMD by dividing the prior December 31 account balance by the applicable life-expectancy factor; IRA owners calculate each IRA separately but may take the combined IRA amount from one or more IRAs, while RMDs from 401(k) and 457(b) accounts generally must be taken separately from each plan.

An RMD can be spent on living costs, reinvested in a taxable account after taxes, used for charitable giving when qualified rules apply, held for future spending, or coordinated with portfolio rebalancing. Tax-aware withdrawal ordering may consider taxable accounts, traditional retirement accounts, Roth accounts, capital gains, Social Security taxation, Medicare income-related premiums, charitable goals, and future RMDs — the right order varies by household and year. The Gold IRA RMD Strategy guide covers distribution planning for physical metals; illiquid assets or physical holdings may require earlier preparation if an RMD must be funded with cash. Customers should speak to a financial or tax advisor before making decisions about RMDs, Roth conversions, taxable withdrawals, charitable distributions, or IRA assets. Goldco does not offer tax or legal advice.

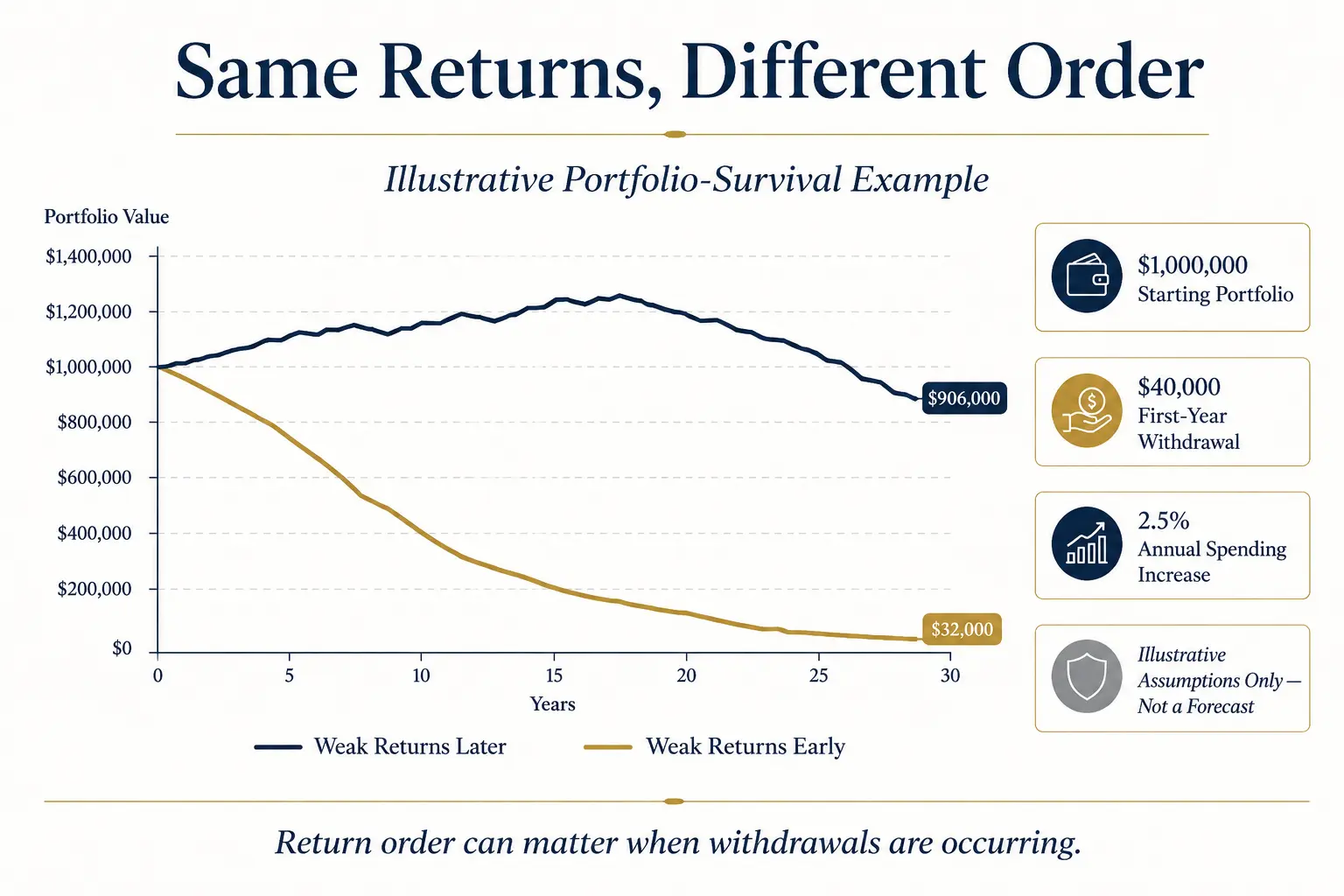

A Realistic Portfolio-Longevity Example

The following math is illustrative only. It is not a forecast, recommendation, or historical backtest. Assumptions: starting portfolio $1,000,000; first-year withdrawal $40,000; annual spending increase 2.5%; withdrawal at the start of each year; thirty annual returns consisting of five weak or mixed years and twenty-five years at 7%; taxes, fees, pensions, Social Security, and other cash flows excluded. Two scenarios use the same annual returns in a different order.

Scenario A — weak returns first. The first five returns are −20%, −10%, 0%, 5%, and 10%, followed by twenty-five years at 7%. Under these assumptions, the portfolio falls below zero during year 25: the poor early sequence combines with rising withdrawals and leaves a smaller base for later growth. Scenario B — weak returns last. The first twenty-five returns are 7%, followed by −20%, −10%, 0%, 5%, and 10%. Under these assumptions, the portfolio finishes year 30 with about $1.27 million. Both scenarios use the same list of returns and the same withdrawals — only the order changes, and the large outcome gap shows why portfolio survival cannot be estimated from an average return alone.

The example is intentionally simplified. Real portfolios have variable inflation, taxes, fees, rebalancing, dividends, interest, changing expenses, and more varied returns, and it assumes no spending guardrails — a temporary reduction after the early losses could improve Scenario A, while higher spending could weaken Scenario B. A useful annual longevity review tracks the current withdrawal rate, essential and optional spending, portfolio balance and allocation, cash reserve, stable income, tax brackets and RMDs, healthcare and housing changes, life-expectancy assumptions, bequest goals, and willingness to use guardrails. The Gold IRA Suitability Quiz can organize precious-metals questions within that wider review.

Frequently Asked Questions

What is retirement portfolio longevity?

Retirement portfolio longevity is the length of time savings can support withdrawals. It depends on the starting balance, retirement length, withdrawal pattern, market-return sequence, inflation, taxes, fees, asset allocation, other income, and spending flexibility.

Is the 4 percent rule still useful?

The 4 percent rule remains a useful starting framework, but it is not a personal spending promise. Morningstar's 2024 research estimated a 3.7% base-case rate under specific 30-year, fixed-spending, allocation, and success assumptions.

Why are early retirement losses especially harmful?

Early losses reduce the balance while withdrawals are occurring. Fewer assets remain to benefit from later gains, which can weaken portfolio survival even when the long-run average return appears reasonable.

Can spending guardrails make money last longer?

Guardrails can improve resilience by linking spending to portfolio conditions. Morningstar found that flexible methods supported higher modeled starting or lifetime spending than fixed-real withdrawals, but they also produced more variable cash flow and often lower ending balances.

Do required minimum distributions determine retirement spending?

No. RMDs are minimum tax-law withdrawals from specified retirement accounts. They do not measure the amount a retiree needs or can sustainably spend.

Can precious metals improve portfolio longevity?

Precious metals may add diversification in some portfolios, but they also have price, cost, liquidity, and storage considerations. No universal allocation was verified. The decision should be based on the full retirement asset allocation and withdrawal plan.

Conclusion

Making money last in retirement is a process, not a single percentage. The strongest retirement portfolio longevity plan combines a long planning horizon, a measured starting withdrawal rate, protection against early sequence risk, diversified assets, stable income for essential costs, spending guardrails, and tax-aware distribution planning. No lever works alone — several modest adjustments can be more durable than one large bet. Two interactive companions to this guide can help put numbers to it: the retirement income longevity calculator estimates how many years a portfolio might last under a chosen withdrawal and return, and the sequence-of-returns risk calculator shows why the order of returns matters once withdrawals begin. The plan should be reviewed at least annually and after major changes in health, housing, family needs, income, taxes, or markets. Calm, documented adjustments can improve portfolio survival without turning normal uncertainty into alarm.

Sources

- Social Security Administration. Actuarial Life Table (Period Life Table, 2023).

- Internal Revenue Service. Retirement Plan and IRA Required Minimum Distributions FAQs.

- Morningstar. What's a Safe Retirement Spending Rate for 2025?.

- Morningstar. How Retirees Can Determine a Safe Withdrawal Rate.

- Associated Press (citing Morningstar). The 4% rule and its origins.

- Associated Press (article provided by Morningstar). Sequence-of-returns risk for new retirees.

- Investor.gov. Diversify Your Investments.

- Investor.gov. Annuities.

- World Gold Council. The Relevance of Gold as a Strategic Asset (2026).

Article reviewed and edited by Daniel M. — editor, 401kToGoldIRA.org. A neutral decumulation guide sourced to the SSA, IRS, Morningstar, Investor.gov, and the World Gold Council; educational only, not financial, tax, or legal advice.