Affiliate disclosure: Some of the links in this article are from sponsors. The site owners may be compensated if customers request information from companies mentioned. Reviews may not be neutral or independent — readers should treat this site as a research starting point, not personalised financial advice. Read the full disclosure.

Quick Answer

Yes, TSP money can be rolled into a Gold IRA when the participant has an eligible withdrawal event, such as separation from federal service, reaching age 59½ for certain in-service withdrawals, or other qualifying circumstances. A direct rollover is generally the safest method because it avoids the 60-day deadline and the 20% withholding issue that can apply to distributions paid to the participant.

Past performance does not guarantee future results.

Not sure which Gold IRA provider fits the bracket? The 2-minute matching quiz on this site narrows the choice based on retirement timing, savings band, and priorities.

Who This Guide Is For

This guide is written for:

- FERS employees who rely heavily on the TSP as one of the main pillars of retirement income.

- CSRS employees who may have smaller TSP balances but still want rollover flexibility.

- Military service members using TSP under BRS or the legacy system, including those with deployment-related contribution issues.

- Recently retired or separated federal workers comparing the TSP against a self-directed precious metals IRA.

The practical question is not only whether a Thrift Savings Plan rollover can be done. The better question is whether moving some or all of the balance out of the TSP improves diversification enough to justify giving up the TSP's ultra-low costs and unique federal plan advantages.

TSP Basics — The 5 Core Funds

The TSP has five core funds plus Lifecycle funds. Those core funds are the G Fund, F Fund, C Fund, S Fund, and I Fund, and the Lifecycle funds simply combine those five in different target-date mixes.

- G Fund: government securities, designed to protect principal while paying a Treasury-based return.

- F Fund: broad U.S. bond market exposure, tied to the Bloomberg U.S. Aggregate Bond Index.

- C Fund: large-cap U.S. stocks, tracking the S&P 500.

- S Fund: U.S. small- and mid-cap exposure outside the S&P 500.

- I Fund: international stocks, with the benchmark updated in recent years to broaden non-U.S. exposure.

- Lifecycle funds: target-date portfolios that automatically shift toward lower risk over time.

One thing mainstream Gold IRA articles often miss is that TSP participants already have a clean, diversified, low-cost menu without needing to shop for mutual funds. The real limitation is that the TSP does not allow direct ownership of physical gold bullion inside the plan, which is why some participants consider a rollover into a self-directed IRA.

Traditional vs Roth TSP

Traditional TSP and Roth TSP balances can exist inside the same TSP account. When money leaves the plan in a rollover, traditional money generally belongs in a traditional IRA, while Roth TSP money generally belongs in a Roth IRA to avoid creating a taxable event.

That matters for any Thrift Savings Plan to Gold IRA strategy because the receiving account type needs to match the tax character of the money being moved. A participant with both traditional and Roth balances may need two receiving IRAs — one traditional self-directed IRA and one Roth self-directed IRA — if both sides of the account are being rolled over.

For military participants, things can get more complex when combat-zone tax-exempt contributions are involved. Some rollover planning around tax-exempt dollars is highly technical, so service members with mixed traditional, Roth, and combat-zone balances should get tax guidance before moving money.

When TSP Becomes Eligible

A TSP rollover is generally tied to a distributable event. Public guidance and rollover explainers consistently identify separation from federal service as the main trigger, while age 59½ can open an in-service withdrawal path for participants who are still working.

Common eligibility situations include:

- Separation from federal civilian or uniformed service.

- Age 59½ while still employed, using an eligible in-service withdrawal route.

- Death or disability, subject to plan and tax rules.

- Certain deployment or military-specific circumstances that can affect contribution and rollover planning.

Many commercial ranking pages oversimplify this and make it sound as if any active federal employee can move TSP money into gold at any time. That is not the practical rule set shown in the TSP-related sources reviewed here.

The Age-55 Rule

The TSP has an important federal employee advantage known as the age-55 rule. If a participant separates from service in the calendar year they turn 55 or later, distributions from the TSP can generally avoid the 10% early withdrawal penalty, even if the participant is younger than 59½.

This matters because some federal employees rush to move all TSP money into an IRA and accidentally give up easier access under TSP withdrawal rules. Once the money is in an IRA, the penalty rules usually become IRA rules, which are not always as flexible as keeping funds in the TSP after a qualifying separation.

For that reason alone, a participant who expects to need retirement cash flow before 59½ should be careful about a full rollover. In many cases, a partial rollover is more sensible than moving the entire account out at once.

In-Service Withdrawals

An in-service withdrawal is the path for someone who is still employed but wants to move part of the TSP after reaching the allowed age threshold. Sources reviewed here show that participants age 59½ or older can take up to four in-service withdrawals per year from the account tied to active employment, subject to vesting and plan rules.

Older TSP paperwork references often mention TSP-90 for in-service withdrawal at age 59½. However, more recent TSP administration guidance indicates that several older forms were replaced by newer guided online processes and a newer TSP-99 withdrawal workflow for separated and beneficiary participants, so readers should confirm the live process on the current TSP platform before acting.

A financial hardship withdrawal is different from a rollover and can create tax friction. That is usually not the preferred path for anyone whose actual goal is a TSP rollover gold transaction into a self-directed IRA.

Why Federal Employees Consider Gold IRAs

Federal employees and service members usually look at Gold IRAs for three reasons:

- Diversification outside stock and bond index funds.

- Concern about inflation, currency risk, or broad market shocks.

- A desire to hold physical gold rather than only paper-based retirement assets.

That said, the case for gold needs to be presented honestly. Gold can diversify a retirement portfolio, but it does not generate income, it can be volatile over shorter periods, and a precious metals IRA adds storage, custodian, and dealer-spread costs that do not exist inside the TSP's standard structure.

Past performance does not guarantee future results. Federal employees should speak to a financial or tax advisor before making decisions.

The G Fund Question

The G Fund is one of the strongest reasons not to roll all TSP money out automatically. It is unique to the federal retirement system and is designed to protect principal while offering a government-securities-based return that many outside cash-like products cannot match in the same way.

A lot of rollover marketing pages ignore this entirely. Many advisors and TSP-focused commentators argue that federal employees should think twice before giving up the G Fund, especially if the account holder values principal stability and simple access within the federal system.

That does not mean a Gold IRA never makes sense. It means a federal employee may want to keep some money in TSP, especially in the G Fund, while rolling out only a portion intended for inflation-hedge or alternative-asset exposure.

TSP Fees vs Gold IRA Fees

This is one of the biggest trade-offs in the whole decision. TSP costs are exceptionally low by retirement-plan standards, while precious metals IRAs usually add flat annual fees plus storage costs and dealer spreads. For the specific numbers, see the sourced Gold IRA fees benchmark (all-in cost by account size) and the dealer markup data; a federal employee weighing physical metal against a simpler option may also want the Gold IRA vs gold ETF comparison.

Industry fee benchmarks for Gold IRAs commonly land around roughly $200 to $350 per year in setup, custodian, and storage costs combined, depending on the custodian and storage arrangement. By contrast, the TSP's fund expenses are a tiny fraction of assets each year, which is one reason it remains one of the strongest employer retirement plans in the country.

The trade-off works best when the account is large enough that a flat annual fee is not overwhelming and when the investor strongly values holding physical metal inside a retirement account. For smaller balances, the fee drag can be much harder to justify.

📊 Project a Gold IRA Portfolio — the Gold IRA Calculator on this site compares a gold-diversified portfolio against an all-stock baseline.

Partial Rollover Is Allowed

A partial rollover can be a smart middle path. Older TSP withdrawal material shows partial withdrawal flexibility after separation, and guidance for current TSP withdrawals indicates that participants can move part of the balance while leaving the rest in the TSP for later.

That is often the most practical answer for federal employees who want some gold exposure but do not want to surrender the G Fund or the low-cost structure of the whole plan. A common thought process is to keep the more defensive TSP allocation in place and move a limited slice of stock-heavy exposure into a self-directed IRA for metals.

This is especially relevant for FERS participants, whose retirement planning often depends on the interaction between the pension, Social Security, and TSP balance. A full rollover is not always necessary to achieve diversification.

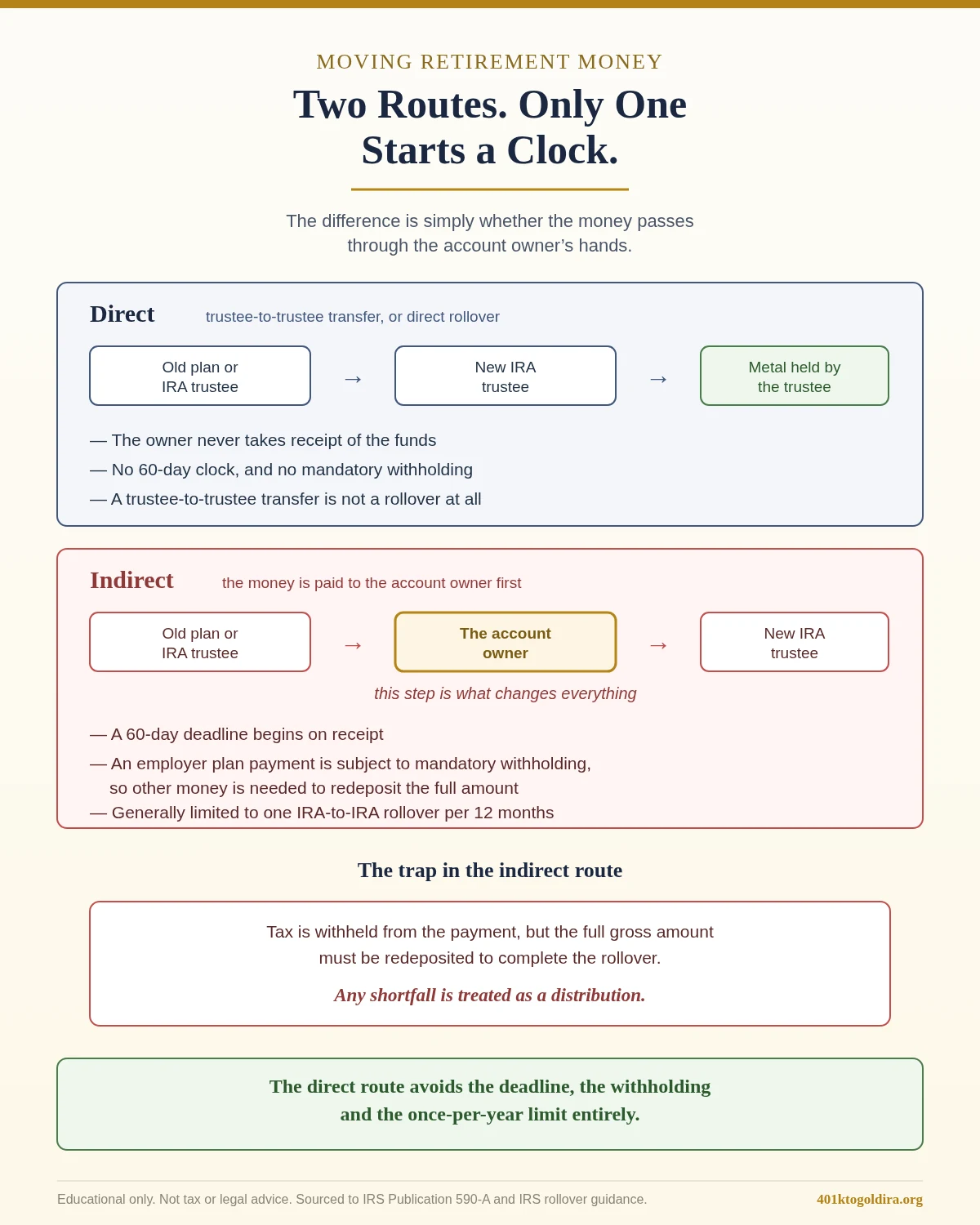

Direct vs Indirect Rollover

A direct rollover is usually the preferred method for a TSP transfer IRA strategy. In a direct rollover, money goes straight from the TSP to the receiving IRA custodian without first being paid to the participant.

An indirect rollover is riskier because the money is distributed to the participant first, and then the participant has only 60 days to redeposit it into an IRA. Some distributions also trigger 20% federal withholding, which can create a funding shortfall unless the participant replaces the withheld amount from other cash.

For most federal employees, that 20% withholding trap is reason enough to avoid the indirect route. A direct rollover is cleaner, easier to document, and less likely to create an accidental taxable event.

Paperwork and Forms

TSP paperwork has changed over time, which creates confusion because many articles still cite older form numbers as if nothing changed. Older references include TSP-77 for partial withdrawals after separation and TSP-90 for age-based in-service withdrawals, but later guidance says several legacy forms were replaced with updated guided online processes and the newer TSP-99 workflow for separated participants.

- TSP-77 is still widely recognized in older materials as a request for partial withdrawal when separated.

- TSP-90 is commonly referenced in older content as the in-service withdrawal form at age 59½, but newer administration updates indicate that older paper forms were replaced in the platform transition.

- TSP-99 is now widely referenced as the withdrawal request workflow for separated and beneficiary participants.

The safest practice is simple: use current TSP account tools and current TSP instructions instead of relying only on archived PDFs or third-party blog screenshots. Federal paperwork details can change, and the right form path depends on whether the participant is separated, still employed, or requesting only a partial move.

The 6-Step Process

1. Confirm rollover eligibility

The participant should first confirm there is a valid distributable event or an allowed in-service withdrawal route. Separation from service is the most common trigger, while age 59½ can create in-service access for active participants.

2. Decide whether the rollover should be full or partial

This is where the G Fund question matters. Many federal employees may be better served by keeping some TSP assets in place and rolling out only a portion.

3. Match the tax buckets correctly

Traditional TSP money generally belongs in a traditional IRA, and Roth TSP money generally belongs in a Roth IRA. Mixed accounts may require more than one receiving IRA.

4. Open the self-directed IRA first

The receiving self-directed IRA should be open before the TSP withdrawal or rollover request is submitted. That allows the participant to use the correct custodian name, account number, and mailing instructions for a direct rollover.

5. Request a direct rollover from TSP

The participant should choose the option that sends the rollover directly to the institution. A direct transfer is the path most sources describe as tax-neutral when the account types are matched correctly.

6. Purchase only IRS-approved metals through the IRA

Once the money lands in the new IRA, the custodian facilitates the purchase of eligible bullion and arranges approved third-party storage. The metals cannot be personally stored at home if they are meant to remain inside the IRA structure.

Military Considerations

Military TSP participants have extra wrinkles that civilian-only articles often miss. Under the Blended Retirement System, matching contributions and service-related timing issues can affect how much remains in TSP and when a rollover decision makes sense.

Combat-zone and tax-exempt contribution rules can also complicate rollover planning. Military OneSource notes that combat pay is tax-exempt and that special contribution limits can apply when combat pay is used, while tax treatment of mixed balances may require careful coordination when rolling money into traditional and Roth IRAs.

For that reason, a Gold IRA for military readers should never be treated as a basic one-line rollover. A service member with combat-zone balances, Roth money, and traditional money should get tax guidance before moving funds.

Tax Treatment

The standard tax rule is straightforward. Traditional TSP money rolls to a traditional IRA without current tax, and Roth TSP money rolls to a Roth IRA without current tax when handled properly.

The problems usually begin when participants:

- Take a distribution instead of a direct rollover.

- Miss the 60-day window on an indirect rollover.

- Mix up Roth and traditional destinations.

- Ignore special military tax-exempt contribution issues.

Customers should speak to a financial or tax advisor before making decisions. Goldco does not offer tax or legal advice.

Common Mistakes

Federal employees often make the same rollover errors:

- Rolling out the entire TSP without thinking about the G Fund advantage.

- Using an indirect rollover and triggering withholding headaches.

- Treating a hardship withdrawal as if it were the same as a rollover.

- Moving money before confirming whether the age-55 TSP rule could matter for near-term income access.

- Choosing a metals provider based only on ads, gifts, or urgency language rather than written fee and spread disclosures.

The quality of the Gold IRA provider matters, but the decision starts with the TSP side of the equation. If the federal employee gets the plan rules wrong, even a reputable custodian cannot fix a bad tax move after the fact.

Provider Fit

Not every federal employee needs the same kind of Gold IRA company. Account size, service expectations, and comfort with education-heavy versus sales-heavy onboarding all matter when comparing providers.

| Investor profile | Possible fit |

|---|---|

| Broad rollover shoppers who want the site's highest-ranked option | Goldco Review |

| Federal employees with larger balances who want an education-first process | Augusta Precious Metals Review |

| Mid-range accounts looking for a more accessible entry point | Noble Gold Review |

A federal employee comparing options should also review the broader Best Gold IRA Companies 2026 comparison, use the Gold IRA Calculator, and keep the Gold IRA Rollover Survival Guide close during the paperwork stage.

Bottom Line

A TSP to Gold IRA rollover can work, but it is not a default move and it is rarely an all-or-nothing decision. The best candidates are federal employees or service members who have a valid rollover event, understand the tax buckets, prefer a direct rollover, and have a clear reason for adding physical precious metals to retirement holdings.

For many TSP participants, the smarter path is a partial rollover rather than a full exit. That approach can preserve the G Fund and the TSP's low-cost structure while still allowing a measured allocation to physical gold through a self-directed IRA.

FAQ

Can a federal employee roll TSP to a Gold IRA?

Yes, after an eligible distributable event or through an allowed in-service withdrawal path. The usual method is a direct rollover into a self-directed IRA that permits precious metals.

Can physical gold be purchased inside TSP?

No reviewed source indicates that the core TSP structure allows direct ownership of physical bullion. That is why participants use a rollover if they want actual IRA-held metals.

What is the best way to do a Thrift Savings Plan rollover?

A direct rollover is usually best because it sends funds straight to the receiving IRA and avoids the 60-day deadline and withholding issues that come with indirect rollovers.

Is a partial rollover allowed from TSP?

Yes, older and current withdrawal guidance indicates that separated participants can move part of the balance and leave the rest in TSP, though live procedures should be confirmed in the account system.

What happens to Roth TSP money in a rollover?

Roth TSP money generally rolls into a Roth IRA. Traditional TSP money generally rolls into a traditional IRA.

What is the federal age-55 rule for TSP?

If a participant separates from service in the year they turn 55 or later, TSP withdrawals can generally avoid the 10% early withdrawal penalty. That rule can be lost in practical terms if funds are moved into an IRA too soon.

Can an active employee move TSP to a Gold IRA before retirement?

Sometimes, but usually only through an allowed in-service withdrawal path after age 59½. Active employees generally cannot move TSP funds freely at any age just because they want gold exposure.

Should a federal employee roll out of the G Fund?

Not automatically. The G Fund is unique to the TSP and is one of the strongest reasons many federal employees keep at least part of the account in place.

Are Gold IRA fees higher than TSP fees?

Yes, in most cases. TSP fees are extremely low, while Gold IRAs commonly add flat annual custodian and storage fees plus dealer spreads.

Do military TSP participants have extra tax issues?

Yes, especially when combat-zone tax-exempt contributions are involved. Mixed traditional, Roth, and tax-exempt balances may require more careful rollover planning.

What forms are used for a TSP rollover?

Older materials reference TSP-77 for partial post-separation withdrawals and TSP-90 for certain in-service withdrawals, while newer guidance says the TSP moved many withdrawal processes to updated online workflows and newer TSP-99 usage for separated participants.

Is there a related guide for other employer plans?

Yes. Readers comparing federal-plan rules with other account types can also review the 403(b) to Gold IRA Rollover for educators and nonprofit employees, and Inherited Gold IRA Rules for related rollover issues after a death in the family.

Article reviewed and edited by Daniel — independent precious-metals retirement researcher.