Affiliate disclosure: Some of the links in this article are from sponsors. The site owners may be compensated if customers request information from companies mentioned. Reviews may not be neutral or independent — readers should treat this site as a research starting point, not personalised financial advice. Read the full disclosure.

Under the SECURE Act, most non-spouse beneficiaries must fully distribute an inherited Gold IRA within 10 years of the owner's death — the "stretch IRA" over a lifetime is largely gone. A surviving spouse is the main exception and can generally treat the account as their own.

Source: IRS — Required Minimum Distributions for IRA Beneficiaries. Eligible designated beneficiaries follow different timing; confirm the category before acting.

Key takeaways

- The account passes to the named beneficiary on the account form — which overrides a will.

- The spouse vs non-spouse decision drives everything else: a spouse can roll it into their own IRA; most non-spouses face the 10-year rule.

- Eligible designated beneficiaries (minor child of the owner, disabled/chronically ill, or someone not more than 10 years younger) may still use a life-expectancy stretch.

- Inherited traditional IRA distributions are generally taxable as ordinary income; the underlying metal still follows IRA custody rules until distributed.

- A missed required distribution carries its own excise tax — beneficiaries should confirm the schedule with the custodian and a tax professional.

Quick Answer

When a Gold IRA owner dies, the account passes to the named beneficiary, not through the will, and becomes either a spousal rollover IRA, an inherited IRA, or a lump-sum payout, depending on who inherits and what election is made. For most non-spouse beneficiaries under the SECURE Act, all funds in an inherited Gold IRA must be distributed by the end of the 10th year after the original owner's death, with taxes based on whether the account was traditional or Roth.

Past performance does not guarantee future results.

Not sure which Gold IRA provider fits the bracket? The 2-minute matching quiz on this site narrows the choice based on retirement timing, savings band, and priorities.

The Three Possible Outcomes for an Inherited Gold IRA

In practice, almost every inherited Gold IRA ends in one of three outcomes.

- Spousal rollover (for surviving spouses): The surviving spouse moves the inherited assets into an IRA in their own name, effectively treating the Gold IRA as if it had always belonged to the spouse. Future RMDs, contribution rules, and tax treatment follow normal IRA rules for the spouse's age and account type, not inherited IRA rules.

- Inherited IRA (beneficiary IRA) treatment: The beneficiary keeps assets in a separate inherited IRA, subject to special timing rules for distributions. Most non-spouse beneficiaries must empty the account by the end of the 10th year after the owner's death; some eligible designated beneficiaries can stretch distributions over life expectancy.

- Lump-sum distribution: The beneficiary takes all assets out at once, either as cash after metals are sold inside the IRA, or as an in-kind distribution of physical coins/bars. The entire distribution is generally taxable in the year received for traditional IRAs; Roth tax treatment depends on holding periods.

What Changed with the SECURE Act

Before 2020, many non-spouse beneficiaries could use a "stretch IRA" strategy, taking required minimum distributions (RMDs) over their life expectancy and leaving the rest of the inherited IRA invested for decades. For inherited Gold IRAs, that meant heirs could hold physical bullion inside the IRA for a long time while taking relatively small annual withdrawals.

The SECURE Act of 2019 and SECURE Act 2.0 changed this for most non-spouse beneficiaries:

- Stretch IRA largely eliminated: Most non-spouse beneficiaries can no longer stretch RMDs over life expectancy. Instead, they must obey the 10-year distribution rule.

- 10-year rule: For deaths after 2019, a designated beneficiary usually must withdraw the entire balance by December 31 of the 10th year following the year of the original owner's death.

- Annual RMD vs "empty by year 10": IRS guidance has evolved. For beneficiaries who inherit from someone who had already started RMDs, recent interpretations suggest that both annual RMDs and the 10-year deadline can apply, adding complexity to planning.

- Exceptions for Eligible Designated Beneficiaries (EDBs): Certain categories of beneficiaries (spouses, minors, disabled, chronically ill, those close in age) may still use life-expectancy-based payouts.

For Gold IRAs, these law changes do not alter which metals are allowed or how depositories work, but they do change how long heirs can keep metals inside the tax-favored wrapper before distributions become mandatory.

Who Counts as an "Eligible Designated Beneficiary"

The SECURE Act carved out exceptions for Eligible Designated Beneficiaries (EDBs), who can still use a version of the stretch strategy.

The IRS and planning literature list these EDB categories:

- Surviving spouse: May treat the IRA as their own, roll over to their own IRA, or keep it as an inherited IRA with special timing options.

- Minor child of the IRA owner: Can use life-expectancy RMDs until reaching the age of majority (often age 21), after which the 10-year rule begins, creating a blend of stretch and 10-year treatment.

- Disabled individual: As defined under strict IRS criteria, can generally stretch distributions over life expectancy, subject to documentation and eligibility rules.

- Chronically ill individual: Similar to disabled category, with definitions based on the inability to perform activities of daily living or other long-lasting conditions.

- Individual not more than 10 years younger than the decedent: For example, a sibling or long-time partner close in age may qualify.

- Certain qualifying trusts (for disabled/chronically ill beneficiaries): Trusts can be treated as EDBs in narrow circumstances if they meet "see-through" requirements and are set up for disabled or chronically ill beneficiaries.

Most adult children and grandchildren do not fall into EDB categories and must follow the 10-year distribution rule.

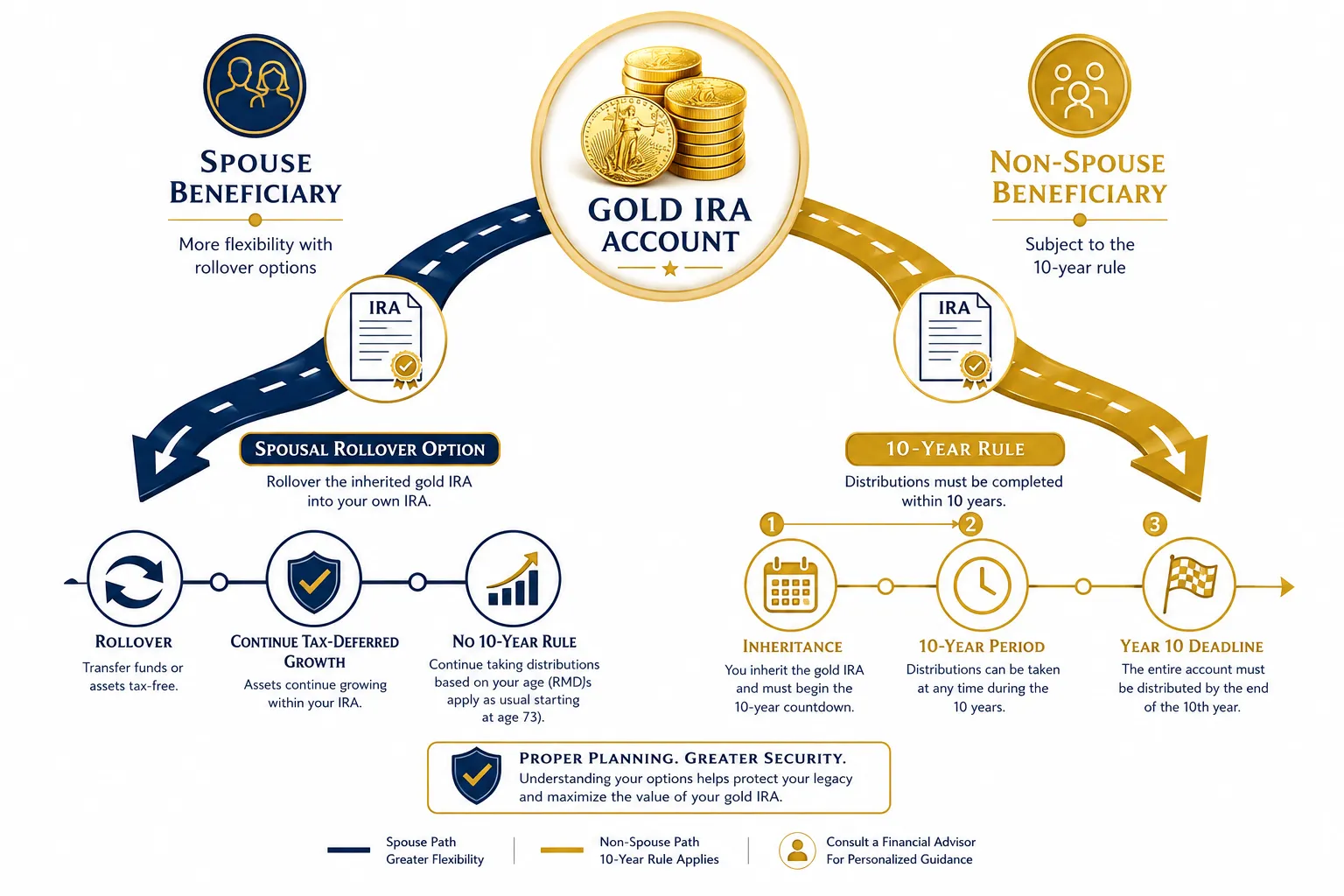

Spouse Beneficiary Rules

A surviving spouse inheriting a Gold IRA usually has the widest range of options.

Three main paths appear in IRS guidance and planning resources:

- Treat the IRA as their own (spousal rollover or re-designation): The spouse moves the inherited Gold IRA assets into an IRA in the spouse's own name, often by rollover. RMDs are then based on the spouse's own age and account type, and the SECURE Act 10-year inherited IRA rule no longer applies. For a younger spouse, this can delay RMDs and extend tax-deferred or tax-free growth (for Roth) inside the Gold IRA.

- Keep the account as an inherited IRA (spousal EDB): A spouse can elect to keep an inherited IRA in beneficiary status, using life-expectancy RMDs under EDB rules. This can be useful if the deceased owner was younger, or if the spouse is under age 59½ and wants access to distributions without early-withdrawal penalties that might apply to an IRA in their own name.

- Lump-sum distribution: The spouse can take a full cash distribution, which is taxable as ordinary income for traditional IRAs but not subject to the 10% early-withdrawal penalty after death. In a Gold IRA context, this may happen via sale of bullion inside the IRA or via an in-kind distribution of coins/bars.

Research from major custodians stresses that the optimal choice depends on the spouse's age, income, and long-term retirement plan. Customers should speak to a financial or tax advisor before making decisions.

📊 Project a Gold IRA Portfolio — the Gold IRA Calculator on this site compares a gold-diversified portfolio against an all-stock baseline.

Non-Spouse Beneficiary Rules

For most non-spouse beneficiaries (adult children, siblings, friends), inherited Gold IRA rules follow the 10-year distribution framework.

Key points:

- Separate inherited IRA required: The beneficiary typically opens an inherited IRA (Gold IRA) titled in the deceased owner's name for the benefit of the beneficiary, rather than rolling assets into an IRA in the beneficiary's own name.

- 10-year window: For deaths after 2019, the beneficiary must fully distribute the account by the end of the 10th calendar year after the owner's death.

- Annual RMD uncertainty: Recent IRS guidance suggests that if the original owner had already reached RMD age (now 73), the beneficiary may be expected to take annual RMDs in years 1-9 and still empty the account by year 10, although regulations are evolving and complex.

- Taxation:

- Traditional Gold IRAs: Distributions from an inherited traditional IRA are taxed as ordinary income, regardless of whether the beneficiary receives cash or in-kind metal.

- Roth Gold IRAs: If the owner satisfied the 5-year holding rule, qualifying distributions can be tax-free, though RMD and 10-year rules still affect timing for non-spouse beneficiaries.

For a non-spouse inheritor of a Gold IRA, the tax code does not care whether the distribution is a sale of gold inside the IRA followed by a cash withdrawal or a direct distribution of American Eagle coins; in both cases, the IRA distribution amount (fair market value) is what appears as taxable income for traditional accounts.

Minor Child Beneficiary Rules

When the beneficiary is a minor child of the IRA owner, the SECURE Act offers a hybrid approach:

- While the child is under the age of majority (often treated as 21 for SECURE Act purposes), the inherited IRA can use life-expectancy-based RMDs, similar to the old stretch IRA.

- Once the child reaches age 21, the account switches into 10-year rule mode, and the remaining balance must be fully distributed by the end of the 10th year after that birthday.

If a minor inherits a Gold IRA, family members and advisors often must balance short-term RMD obligations with questions about when to liquidate or distribute bullion, and how to avoid large tax spikes in early working years.

Trust Beneficiary Rules

Many estate plans name a trust as the IRA beneficiary to control how heirs receive assets, but this adds another layer of rules.

Two broad categories appear in IRS and planning literature:

- See-through (look-through) trusts: If a trust meets detailed requirements and qualifies as a see-through trust, the IRS looks through to underlying individual beneficiaries to apply inherited IRA rules. Trusts often fall into:

- Conduit trusts, which require IRA distributions to be passed directly out to beneficiaries;

- Accumulation trusts, which let the trustee retain distributions inside the trust.

- Non-see-through trusts and estates: If the trust does not qualify as see-through, or if the IRA is left to the estate, more restrictive rules and shorter distribution windows can apply, often defaulting to 5-year or 10-year payouts depending on facts.

In Gold IRA contexts, trustees must decide whether to sell metals inside the IRA, take in-kind distributions into the trust, or transfer assets to beneficiaries, each with tax and control implications. Because the interaction between trust law, SECURE Act rules, and physical metals is complex, professional estate and tax counsel is especially important.

Special Considerations for Physical Gold

A Gold IRA is simply a self-directed IRA that holds coins and bars instead of mutual funds or ETFs, but the presence of physical bullion changes some practical decisions when the account is inherited.

In-kind metal distributions vs liquidation

Beneficiaries generally have two broad choices:

- Sell metals inside the IRA, then distribute cash: The custodian sells gold or silver held in the IRA and sends cash to the beneficiary as a taxable distribution (for traditional IRAs). Tax is based on the distribution amount, not on any separate capital gains schedule, because the distribution comes from a tax-deferred account.

- Take in-kind distributions of physical metals: The IRA transfers ownership of specific coins or bars directly to the beneficiary, who then holds metals in a taxable account or personally. The fair market value of the metals on the distribution date counts as the taxable distribution amount for traditional IRAs. Future gains or losses when the beneficiary later sells the coins are taxed under standard capital gains rules, using the distribution date value as the cost basis.

Both routes satisfy required distributions; the main differences are timing of tax, liquidity, and how much physical bullion the heir wants to keep.

No home storage inside the IRA

Inherited Gold IRAs still must obey standard IRA storage rules: IRS guidance and precious-metals IRA regulations state that IRA metals must be held by an approved trustee or custodian, not at home. Taking personal possession of IRA metals before a proper distribution is treated as a distribution and can trigger income tax (and penalties in some cases).

Inherited Traditional vs Inherited Roth Gold IRA

Inherited Gold IRA rules differ significantly between traditional and Roth Gold IRAs, mostly in taxation, not in distribution timing.

Inherited traditional Gold IRA

- Contributions were pre-tax, so distributions to beneficiaries are generally taxed as ordinary income.

- RMD rules depend on beneficiary status and SECURE Act categorizations; the 10-year rule applies to most non-spouse beneficiaries.

- Whether the heir receives cash or metal, the taxable amount is the fair market value of the distribution at the time it leaves the IRA.

Inherited Roth Gold IRA

- If the original Roth IRA satisfied the 5-year holding requirement, qualified distributions to heirs can be tax-free, even though RMD rules still govern timing for non-spouse beneficiaries.

- The SECURE Act still imposes the 10-year distribution rule on many non-spouse beneficiaries of Roth IRAs.

- For a Roth Gold IRA, an inheritor may have greater flexibility to delay distributions until later in the 10-year window without income-tax concerns, though market risk for metals remains.

In both cases, gold and other precious metals can rise or fall in value, and tax law can change; planning needs to account for both.

Required Minimum Distributions on Inherited IRAs

RMD rules for inherited IRAs differ from those for owners and are influenced by the SECURE Act.

High-level patterns:

- Traditional IRAs: For many non-spouse beneficiaries, the focus is on emptying the account by year 10, though annual RMDs may also apply if the decedent had reached RMD age. EDBs can use annual life-expectancy RMDs, potentially preserving the inherited Gold IRA longer.

- Roth IRAs: Original Roth owners face no lifetime RMDs, but beneficiaries do; the 10-year rule and/or life-expectancy RMDs can apply depending on beneficiary type.

- Gold IRA nuance: RMD amounts are calculated based on fair market value of metals inside the IRA, usually using year-end valuations and standard IRS life-expectancy tables. The custodian can satisfy RMDs by selling metals for cash or by distributing coins/bars worth at least the RMD amount in kind.

Because RMD calculations can be tricky when metal prices move, many beneficiaries rely on the IRA custodian's valuation tools and double-check figures with tax professionals.

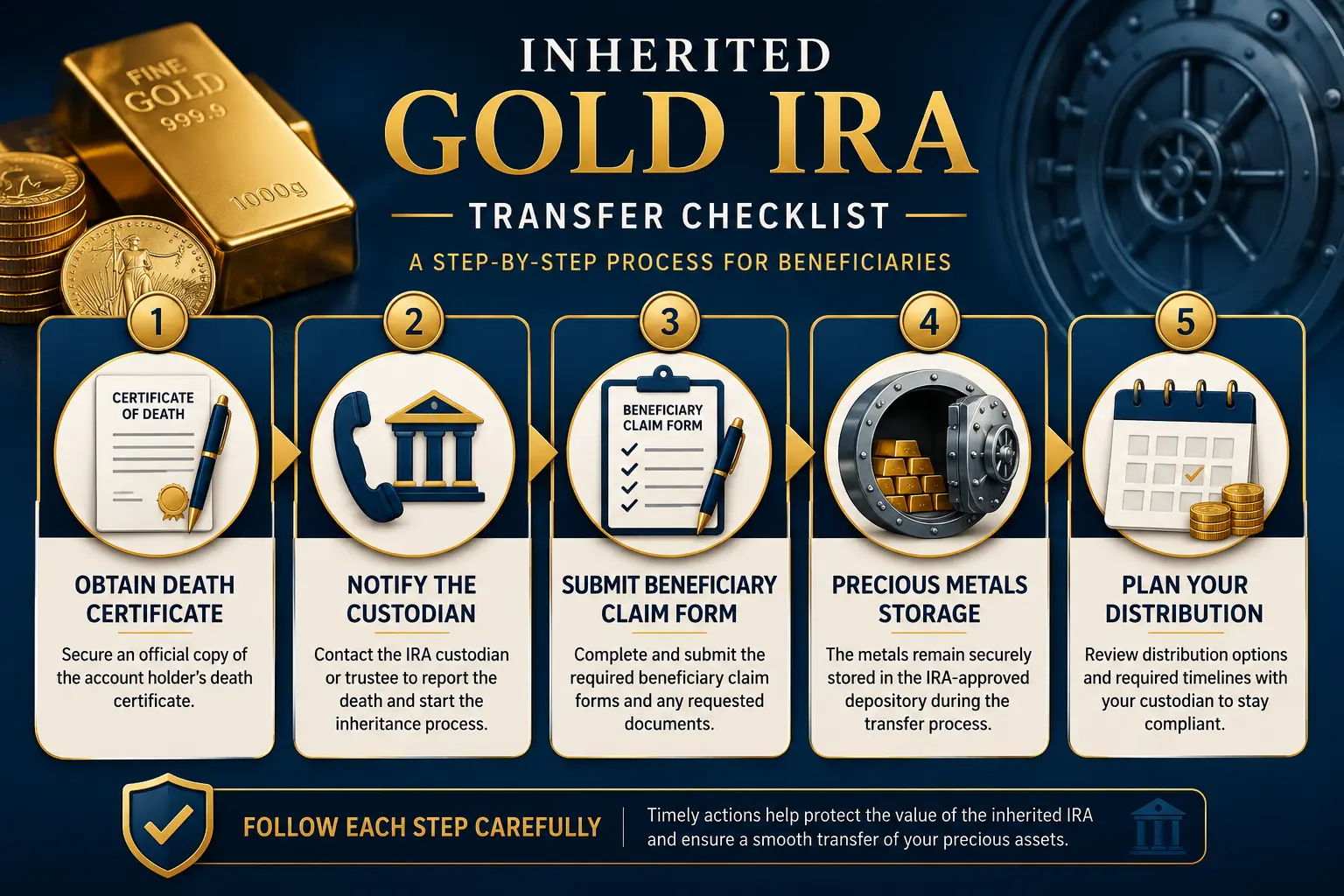

What to Do Immediately After Inheriting a Gold IRA

The weeks after inheriting a Gold IRA can be overwhelming. A calm, stepwise approach helps.

A practical 5-step checklist from IRA and estate-planning resources:

- Confirm the type of account and custodian: Identify whether the account is traditional or Roth, the IRA custodian, and the depository holding the metals.

- Obtain and review beneficiary forms: Confirm that the beneficiary designation is valid and up to date; this usually overrides will instructions for the IRA.

- Clarify beneficiary status under SECURE Act rules: Determine whether the beneficiary is a spouse, EDB, non-spouse adult, minor child, or trust, since this drives the choice of strategy and timelines.

- Set up the inherited IRA or spousal rollover with the custodian: Work with the existing custodian (or a new one, if transferring) to create the appropriate inherited account structure and ensure titles reflect inherited status correctly.

- Build a distribution plan with professionals: Consult a tax advisor and, where appropriate, an estate attorney to map out how and when to take distributions (cash or metal), manage RMDs, and handle any state inheritance or estate-tax exposure.

Customers should speak to a financial or tax advisor before making decisions.

Common Mistakes Heirs Make

Common patterns in IRS guidance and advisor case studies include:

- Cashing out everything immediately without understanding tax impact: A full lump-sum distribution from a traditional Gold IRA can push the beneficiary into a much higher tax bracket in that year, especially if metal prices are elevated.

- Missing key deadlines: Failing to establish the inherited IRA correctly, mis-titling accounts, or missing the 10-year deadline can lead to penalties or forced distributions under less favorable rules.

- Assuming old stretch rules still apply: Some heirs still think they can stretch RMDs over life expectancy when the SECURE Act now enforces the 10-year window for most non-spouse beneficiaries.

- Treating physical gold as tax-free because it is "just coins": Distributions of bullion from a traditional Gold IRA are generally taxable as ordinary income based on fair market value, even if the beneficiary keeps the coins and does not sell them.

- Ignoring state estate or inheritance taxes: In higher-tax states with estate or inheritance taxes, heirs may face state-level obligations separate from federal income tax on distributions.

The Gold IRA Rollover Survival Guide on this site includes a section on avoiding common IRA inheritance traps. The companion article on Gold IRA Creditor Protection by State covers what happens to inherited Gold IRAs in bankruptcy.

Estate Planning Steps for Current Gold IRA Owners

Gold IRA owners planning ahead can make the inheritance process easier for heirs by taking several steps:

- Keep beneficiary designations up to date: Regularly review and update primary and contingent beneficiaries with the custodian, especially after major life events.

- Coordinate IRA beneficiaries with the will and any trusts: Ensure that IRA beneficiary forms, wills, and trust documents work together and do not conflict, especially when trusts are involved.

- Clarify intentions for metals vs cash: Communicate whether heirs are expected to keep metals, sell them, or split between heirs, and document these preferences where possible.

- Consider whether a trust is appropriate: In some cases, using conduit or accumulation trusts as IRA beneficiaries can help manage distributions for minors, spendthrift heirs, or disabled beneficiaries, though SECURE Act rules still apply.

- Document storage and account details: Provide heirs with information on custodians, depositories, and account numbers, so they can act promptly when needed.

Estate planners often recommend revisiting beneficiary designations whenever a new provider is chosen, for example after switching to a Gold IRA company like Goldco, Augusta, or Noble Gold; the Best Gold IRA Companies 2026 comparison and individual provider reviews on this site provide background for those choices.

State Estate Tax and Gold IRAs

While federal estate tax currently affects only the largest estates, state-level estate and inheritance taxes can impact a wider range of families.

Key points from estate-planning sources:

- State estate tax: A small number of states impose their own estate tax with lower thresholds than federal law, and Gold IRAs are generally counted as part of the taxable estate.

- State inheritance tax: Some states tax beneficiaries directly on inherited assets, with rates varying by relationship and amount.

- Valuation of Gold IRAs: For estate-tax purposes, Gold IRAs are valued based on the fair market value of metals in the account at the date of death (or alternate valuation date), similar to other assets.

Because state rules differ widely and can change, families often need local tax counsel to map out the combined federal and state impact of inheriting a Gold IRA.

Bottom Line

Inherited Gold IRA rules blend general IRS inherited IRA regulations with the practical realities of physical precious metals held in depositories. For spouses, the key decision is often between treating the account as their own or using inherited IRA status; for non-spouse beneficiaries, the main challenge is navigating the SECURE Act 10-year rule, RMD requirements, and tax implications while deciding whether to keep metals, sell them, or take in-kind distributions over time.

A thoughtful plan usually includes clear beneficiary designations, coordination with wills and trusts, a distribution schedule that fits the beneficiary's tax bracket, and a realistic view of gold's role in the overall portfolio rather than relying on metals alone. Past performance does not guarantee future results, and precious metals can be volatile; tax and estate rules may also change, so ongoing professional guidance is important.

FAQ

What happens to a Gold IRA when the owner dies?

The Gold IRA passes to the named beneficiary, who can treat it as a spousal rollover (if a spouse), maintain it as an inherited IRA, or take a lump-sum distribution; probate usually does not control the account.

Do inherited Gold IRAs follow different rules than regular inherited IRAs?

No. The federal inheritance rules are the same for Gold IRAs and other IRAs; the difference is that the account holds physical metals, creating extra decisions about in-kind distributions versus liquidation.

How does the SECURE Act affect inherited Gold IRAs?

The SECURE Act largely eliminated the stretch IRA for most non-spouse beneficiaries, replacing it with a requirement to empty the inherited IRA by the end of the 10th year after the owner's death, with limited exceptions for EDBs.

Who qualifies as an Eligible Designated Beneficiary (EDB)?

EDBs include surviving spouses, minor children of the IRA owner, disabled individuals, chronically ill individuals, and certain beneficiaries not more than 10 years younger than the decedent, plus some qualifying trusts.

Can a spouse just roll an inherited Gold IRA into their own IRA?

Yes. A surviving spouse can generally treat the IRA as their own via rollover or re-designation, after which normal IRA rules apply based on the spouse's age and account type.

How are inherited traditional Gold IRA distributions taxed?

Distributions from an inherited traditional Gold IRA — whether in cash or in-kind bullion — are usually taxed as ordinary income based on the fair market value of the distribution at the time it leaves the IRA.

Are inherited Roth Gold IRA distributions tax-free?

If the original Roth IRA met the 5-year holding requirement, many beneficiary distributions can be tax-free, but the SECURE Act's 10-year distribution rule or life-expectancy rules still govern timing for non-spouse beneficiaries.

Can a beneficiary take physical gold out of an inherited Gold IRA?

Yes. Beneficiaries can receive in-kind distributions of gold coins or bars, but the fair market value of the metals counts as the distribution amount for RMD and tax purposes in traditional IRAs.

What happens if the IRA is left to a trust?

If a trust is named as beneficiary, see-through and conduit vs accumulation trust rules determine how SECURE Act and RMD rules apply, and distributions may flow to or remain inside the trust at the trustee's discretion.

Does a Gold IRA go through probate?

Generally, no. Properly titled IRAs with valid beneficiary designations bypass probate and go directly to the named beneficiary, though the overall estate value can still matter for estate-tax purposes.

Can gold inside an inherited IRA be moved to another Gold IRA provider?

In many cases, an inherited IRA can be transferred trustee-to-trustee to a different custodian that supports Gold IRAs, while preserving its inherited status and tax deferral; the specific rules depend on the new provider and IRS guidance.

Where can readers learn more about providers for Gold IRAs and rollovers?

This site's Best Gold IRA Companies 2026 comparison, Goldco Review, Augusta Precious Metals Review, Noble Gold Review, and Goldco Lawsuit and Legal Record provide detailed provider research, while the Gold IRA Rollover Survival Guide offers step-by-step rollover and inheritance context.

Article reviewed and edited by Daniel — independent precious-metals retirement researcher.