Affiliate disclosure: Some of the links in this article are from sponsors. The site owners may be compensated if customers request information from companies mentioned. Reviews may not be neutral or independent — readers should treat this site as a research starting point, not personalised financial advice. Read the full disclosure.

Who This Guide Is For

This guide is written for:

- Public school teachers and K-12 staff in 403(b) plans sponsored by school districts.

- University and college faculty in 403(b) or 403(b)/401(a) combinations (often with TIAA-CREF).

- Nonprofit employees at hospitals, charities, foundations, and churches covered by 403(b) plans.

- Ministers and employees of certain religious organizations that use 403(b) tax-sheltered annuities.

The focus is practical: how an educator with a 403(b) can legally move funds into a Gold IRA without triggering taxes or penalties, and what traps to avoid.

Past performance does not guarantee future results.

Not sure which Gold IRA provider fits the bracket? The 2-minute matching quiz on this site narrows the choice based on retirement timing, savings band, and priorities.

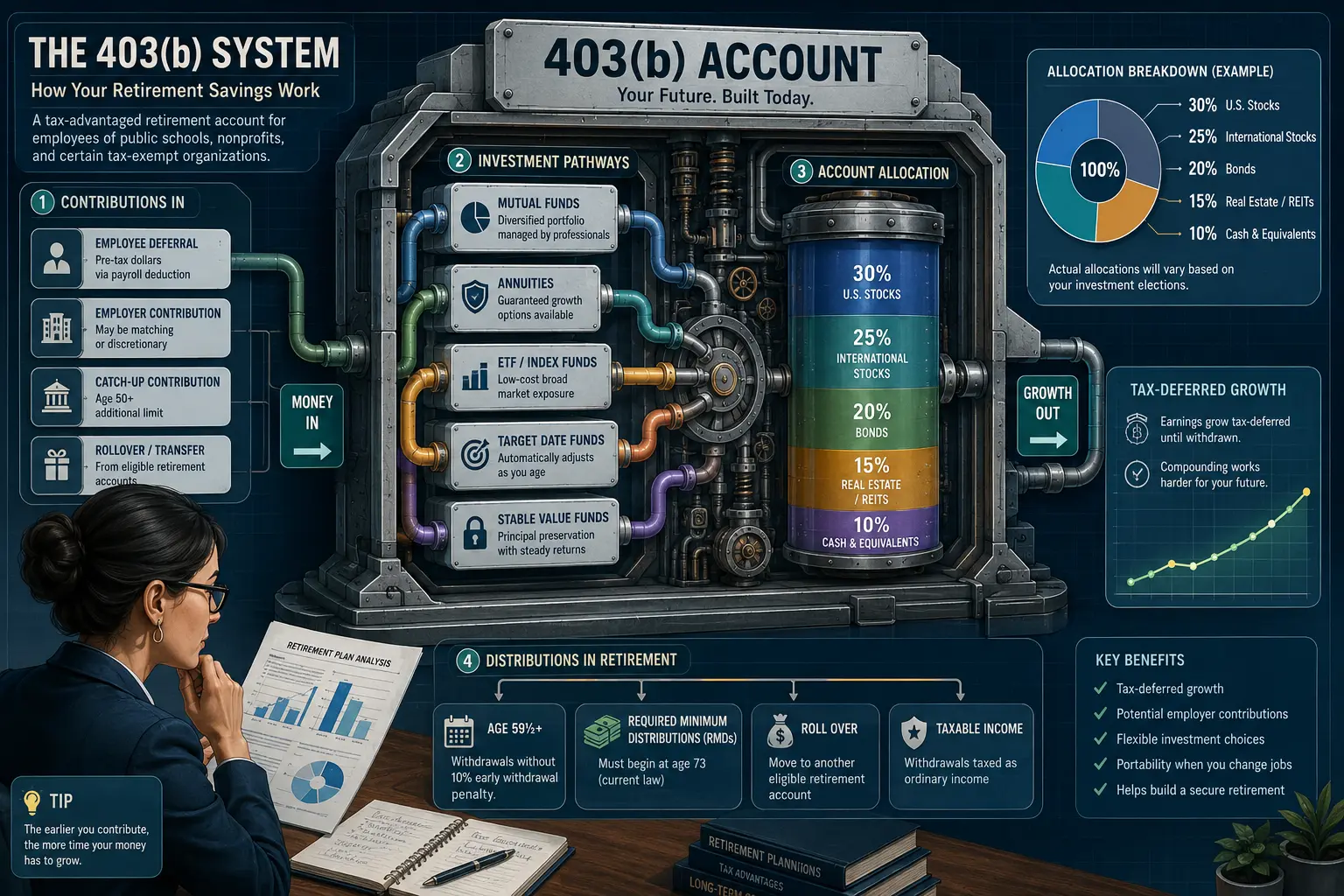

403(b) Basics — What Educators Actually Have

A 403(b) plan is a tax-advantaged retirement plan for employees of public schools, 501(c)(3) nonprofits, and certain churches. Two main structures exist, and the structure affects rollover mechanics:

- 403(b)(7) custodial accounts

- Assets are held in mutual funds or similar investments inside custodial accounts.

- Many private-nonprofit 403(b)(7) plans are covered by ERISA; public-school 403(b)s generally are not.

- 403(b)(1) tax-sheltered annuities (TSAs)

- Historically issued as fixed or variable annuity contracts from insurers such as TIAA-CREF, Voya, AXA/Equitable.

- Contracts may include surrender charges and illiquidity periods, which become important when considering a rollover.

Educators often have multiple 403(b) contracts across vendors accumulated over a long career, making it important to map exactly which contracts are eligible for rollover and what charges apply.

403(b) vs 401(k) — Key Differences That Matter for Rollovers

While 403(b) and 401(k) plans both provide tax-deferred retirement savings, there are important differences for rollover planning:

- Employer coverage: 403(b) — public schools, 501(c)(3) nonprofits, some ministers. 401(k) — private-sector employers and some public employers.

- Investment structure: 401(k)s typically use mutual funds and collective trusts. 403(b)s may be annuity-heavy, especially legacy TIAA, Voya, AXA contracts, with associated surrender fees.

- ERISA coverage: Many 401(k)s are ERISA-governed, with strong fiduciary standards and creditor protection. Public-school 403(b)s are usually non-ERISA; nonprofit 403(b)s can be ERISA or non-ERISA depending on design.

- Rollover quirks: Some 403(b) annuity contracts restrict how and when funds can be moved, requiring TPA (Third-Party Administrator) forms, surrender charge calculations, or special distribution codes before a rollover is allowed.

These quirks mean that a teacher rolling from a TIAA 403(b) into a Gold IRA faces different paperwork and timing risk than a private-sector employee rolling from a standard 401(k).

When Educators Are Eligible to Roll Over a 403(b)

A 403(b) account can only be rolled to a Gold IRA after a "distributable event" under IRS and plan rules.

Common distributable events:

- Separation from service: Leaving the employer sponsoring the 403(b) (retirement, job change, layoff) usually triggers full rollover eligibility.

- Reaching age 59½: Many plans allow in-service distributions or rollovers at age 59½, even if the participant continues working.

- Plan termination: If the employer terminates the 403(b) plan, participants can generally roll balances into IRAs or other plans.

- Death or disability: Death — plan assets move to beneficiaries, who may roll into inherited IRAs subject to inherited-IRA rules (covered in Inherited Gold IRA Rules). Disability — some plans permit distributions and rollovers when a participant meets disability criteria.

The specific Summary Plan Description (SPD) and vendor paperwork determine when a particular educator's contracts become rollable.

The Age-55 Separation From Service Rule

Educators often hear about the "age-55 rule" and wonder how it affects rollovers.

The rule works as follows:

- For 403(b) and 401(k) plans, distributions taken after separation from service in the year the participant turns 55 or later are exempt from the 10% early-withdrawal penalty (though ordinary income tax still applies).

- This rule affects penalty-free withdrawals, not the basic ability to roll funds to a Gold IRA. A separation from service already counts as a distributable event for rollover purposes, even if it occurs before 55.

Practically, some educators choose to leave part of a 403(b) in the plan for age-55 penalty-free access, while rolling the rest into an IRA or Gold IRA. That trade-off is highly personal and should be discussed with a financial or tax advisor.

In-Service Rollovers — When Plans Allow Them

Many educators continue in the same district or university well past age 59½. Some 403(b) plans allow in-service rollovers, which let participants move money to an IRA while staying employed.

Key points:

- Common thresholds: Some 403(b) plans allow in-service rollovers starting at age 59½, and a minority allow them at age 50 or 55.

- Plan-specific rules: Each plan can set stricter rules than the IRS minimum; some plans do not allow any in-service rollovers until separation.

- Vendor differences: For example, certain TIAA RA/GRA contracts restrict access until separation, even if the plan as a whole allows in-service transactions.

An educator considering a 403(b) to Gold IRA rollover while still employed should request written confirmation of in-service rollover provisions from the plan administrator or vendor.

Why Educators Consider Gold IRAs

Educators typically spend decades accumulating equity and bond exposure through mutual funds and annuities. A Gold IRA introduces physical precious metals into that retirement mix.

Common motivations cited in independent research:

- Diversification: Adding gold and silver can reduce reliance on stocks and bonds alone, creating a more diversified portfolio of uncorrelated assets.

- Inflation and currency risk: Gold can serve as a potential hedge against inflation and currency debasement, though results vary by time period.

- Tangible asset preference: Some educators prefer having part of their retirement in tangible bullion stored in depositories rather than purely paper claims.

Important caveats: Gold can be volatile and may underperform stocks and bonds over long stretches. Gold IRAs carry custodian and storage fees and often involve dealer spreads on bullion. Past performance does not guarantee future results.

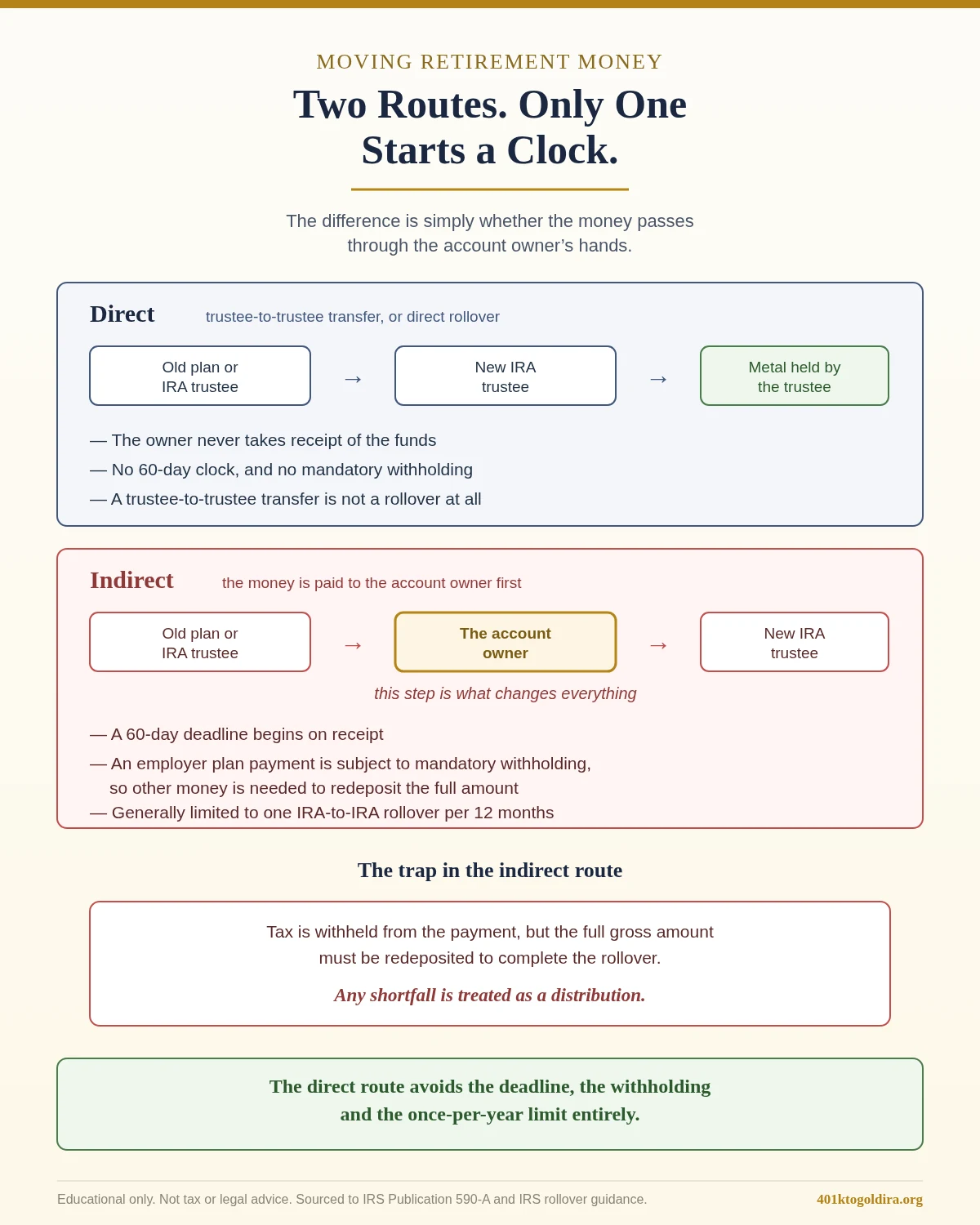

Direct vs Indirect Rollover — The 60-Day Trap

When moving money from a 403(b) into a Gold IRA, there are two technical paths:

Direct rollover (trustee-to-trustee transfer)

- Funds move directly from the 403(b) provider to the IRA custodian, without the participant taking possession.

- No mandatory withholding, no 60-day redeposit deadline, and the "once-per-year IRA rollover rule" does not apply.

- This is often the cleaner method for 403(b) to Gold IRA rollovers.

Indirect rollover

- The 403(b) cuts a check payable to the participant, who then has 60 days to deposit the funds into an IRA.

- The plan must withhold 20% for federal income tax, and any withheld amount not re-deposited within 60 days is treated as a taxable distribution (and possibly subject to a 10% penalty if under 59½).

Because of the 20% withholding and strict 60-day window, indirect rollovers are usually riskier and more complex. For educators, a direct trustee-to-trustee rollover is typically the safer path.

📊 Project a Gold IRA Portfolio — the Gold IRA Calculator on this site compares a gold-diversified portfolio against an all-stock baseline.

The 6-Step 403(b) → Gold IRA Rollover Process

The practical process for educators usually breaks down into six steps.

Step 1: Confirm a distributable event

The participant confirms with the 403(b) administrator that a qualifying event has occurred: separation from service, age 59½ in a plan that permits in-service rollovers, plan termination, or another eligible distribution trigger.

Step 2: Check annuity surrender charges (TIAA, Voya, AXA, etc.)

If the 403(b) is held inside annuity contracts rather than mutual-fund custodial accounts, the vendor should provide: current account values by contract, any surrender charge schedule, and whether certain funds are in illiquid "RA" or legacy contracts at TIAA or similar vendors.

Large surrender charges may justify a partial rollover or a slower, staged approach.

Step 3: Choose a Gold IRA provider

The educator selects a self-directed IRA custodian and metals dealer, either directly or via a bundled provider (such as Goldco, Augusta Precious Metals, Noble Gold, or others profiled on this site).

Key selection points:

- Minimum account size (e.g., $20k Noble, $25k Goldco, $50k Augusta).

- Fee structure (custodian fees, storage fees, dealer spreads).

- Educational support and customer-service reputation.

The Best Gold IRA Companies 2026 comparison and provider reviews on this site can help narrow options.

Step 4: Open the self-directed Gold IRA

The chosen custodian opens a self-directed IRA (Traditional or Roth, matching the pre-tax or Roth status of the 403(b) funds). Paperwork includes an IRA application, beneficiary designations, and depository selection. No money moves yet; the account is simply opened and ready to receive the rollover.

Step 5: Initiate a trustee-to-trustee transfer

The educator works with both institutions to arrange a direct rollover:

- The Gold IRA custodian typically provides a transfer/rollover request form.

- The 403(b) administrator or vendor may require its own distribution election form, often with a box labelled "direct rollover to IRA".

- Funds are then sent directly to the IRA custodian, by check or wire, without passing through the participant's personal account.

Step 6: Select metals and complete the purchase

Once funds arrive in the Gold IRA cash balance, the participant works with the metals desk to choose IRS-approved coins and bars. The custodian pays the dealer from the IRA, and metals are shipped to an IRS-approved depository. Statements then show metal holdings instead of mutual funds.

Throughout this process, the money never leaves a tax-advantaged account, so a properly structured 403(b) to Gold IRA rollover is generally not a taxable event.

TIAA-CREF Specific Considerations

TIAA-CREF (now TIAA) is a dominant vendor for higher-education and some K-12 403(b) plans and has unique contract structures.

Common wrinkles:

- Contract types: TIAA uses RA, GRA, GSRA, and IRA annuity contracts, each with different liquidity rules and surrender charges.

- Traditional annuity restrictions: The "TIAA Traditional" annuity often includes 10-year or multi-year payout provisions if balances are withdrawn or transferred, meaning a rollover may need to be staged over time.

- TPA and employer authorization: Many TIAA 403(b)s require third-party administrator (TPA) or employer sign-off before a rollover proceeds, especially while the participant is still employed.

Educators should request: a detailed breakdown of contract types and balances, the liquidity schedule and any surrender charges, and a copy of vendor-specific rollover instructions.

Voya / AXA and Other Annuity Considerations

Many K-12 403(b) plans still include legacy variable annuities from insurers like Voya and AXA/Equitable. Considerations include:

- Surrender periods: Contracts often have 7-10-year surrender schedules, where early withdrawals incur percentage penalties.

- High internal costs: Some older annuities carry high mortality and expense (M&E) charges and subaccount fees, which may motivate a rollover despite surrender fees.

- Vendor-specific paperwork: Each insurer has its own distribution and rollover forms, which must be filled out correctly to classify the movement as a direct rollover rather than a taxable distribution.

For educators, the trade-off is between paying surrender charges now to gain lower ongoing costs and new investment options, versus waiting for surrender periods to expire before doing a rollover.

Tax Treatment of a 403(b) Rollover to Gold IRA

From a tax perspective, the key is to match pre-tax or Roth status and use a direct rollover.

- Pre-tax 403(b) → Traditional Gold IRA: A direct rollover from a pre-tax 403(b) to a Traditional Gold IRA is generally not taxed at the time of rollover. Future distributions from the Gold IRA are taxed as ordinary income, with RMDs starting at age 73 under SECURE Act 2.0.

- Roth 403(b) → Roth Gold IRA: A direct rollover from a Roth 403(b) to a Roth Gold IRA preserves the Roth character; qualified distributions later can be tax-free if holding-period rules are met.

- Once-per-year rule: The "once-per-year IRA rollover rule" applies only to 60-day rollovers between IRAs, not to direct 403(b) → IRA trustee-to-trustee transfers.

Indirect rollovers and mis-directed checks can trigger tax bills and penalties. Because the stakes are high, customers should speak to a financial or tax advisor before making decisions.

Common Mistakes Educators Make

Patterns seen in advisor case studies and rollover guides include:

- Requesting a distribution instead of a rollover: Checking the wrong box can result in a taxable distribution plus 20% withholding and possible 10% penalty, instead of a clean rollover.

- Using an indirect rollover and missing the 60-day deadline: Delays, mail errors, or confusion can cause funds not to be re-deposited on time, turning the rollover into a permanent distribution.

- Ignoring surrender charges and contract restrictions: Rolling out of TIAA or insurer annuities without understanding surrender schedules can cost thousands in avoidable penalties.

- Rolling everything out of a plan that allows age-55 penalty-free withdrawals: Some educators later regret not leaving a portion in the 403(b) to preserve age-55 penalty-free access, especially before age 59½.

- Choosing a Gold IRA provider without understanding fees and spreads: Focusing only on promotions or bonus-metal offers rather than total cost and metals pricing can erode long-term value.

The Gold IRA Rollover Survival Guide on this site includes checklists designed specifically for educators and other 403(b) participants.

What If Only Part of the 403(b) Should Roll Over?

A common strategy is to roll only a portion of a 403(b) into a Gold IRA while leaving the rest in mutual funds or annuities.

- Partial rollovers usually allowed: Most 403(b) plans allow participants to designate specific dollar amounts or percentages for rollover, subject to any contractual surrender or minimum-balance rules.

- Multiple vendors: Teachers with several 403(b) vendors can often roll out one contract while leaving others untouched.

- Blend with other IRAs: Some educators pair a Gold IRA with a separate low-cost index-fund IRA, creating a diversified structure over time.

Partial rollover options should always be confirmed with the plan administrator and annuity vendors before proceeding.

What "Approved" Gold IRA Metals Look Like

A Gold IRA can only hold IRS-approved metals; not every coin or bar qualifies.

General IRS rules:

- Gold fineness: Gold must be 99.5% pure or higher, except for the American Gold Eagle, which is specifically allowed despite slightly lower fineness.

- Silver: At least 99.9% pure.

- Platinum & palladium: At least 99.95% pure.

Commonly accepted Gold IRA products include American Gold Eagles, American Silver Eagles, Canadian Maple Leafs (gold and silver), and certain bars from approved refiners and mints that meet purity standards.

Collectible coins, rare coins, and certain proof sets do not qualify, and buying them inside an IRA can trigger prohibited-transaction issues.

Provider Options for Educators

This site's research highlights several providers that often fit educators at different balance levels:

- Goldco (minimum ~$25,000): Positioned as "Our Top Pick" for combined service quality, buyback program, and reputation. Often suits educators rolling mid-five-figure or larger 403(b) balances into Gold IRAs. Goldco does not offer tax or legal advice; customers should consult independent professionals on rollover consequences. See Goldco Review.

- Augusta Precious Metals (minimum ~$50,000): Education-first model with a mandatory web conference, very strong BBB/BCA records, and flat-fee schedule. Often attractive for professors or administrators with larger accounts who want a slower, high-touch onboarding process. See Augusta Precious Metals Review.

- Noble Gold (minimum ~$20,000): Often discussed for starter portfolios, with relatively low minimums and simple fees. May fit teachers rolling a partial 403(b) balance into metals for the first time. See Noble Gold Review.

- American Hartford Gold (~$10,000 minimum): Often considered for smaller rollovers or more promotion-driven offerings, with strong reputation but heavier use of free-silver marketing. See American Hartford Gold Fees.

The Best Gold IRA Companies 2026 comparison and the Birch Gold vs American Hartford Gold head-to-head provide deeper analysis for educators comparing providers side by side.

Bottom Line

A 403(b) to Gold IRA rollover is entirely feasible for many educators, but the decision sits at the intersection of plan rules, annuity contracts, tax rules, and personal risk tolerance. The safest implementations use direct trustee-to-trustee rollovers, careful review of surrender charges, and providers that clearly explain fees and approved metals.

Because precious metals can be volatile and carry their own risk profile, a Gold IRA is usually best viewed as a diversifying component, not a replacement for all mutual-fund or annuity holdings. Past performance does not guarantee future results, and gold prices can move sharply in both directions. Customers should speak to a financial or tax advisor before making decisions, especially when coordinating 403(b) rollover timing, Social Security, pensions, and other retirement income sources.

FAQ

Can a 403(b) be rolled into a Gold IRA?

Yes. A 403(b) balance can generally be rolled into a self-directed Gold IRA after a distributable event such as separation from service, reaching age 59½ (if the plan permits in-service rollovers), or plan termination.

Who is eligible to have a 403(b) plan?

Eligible workers include public school teachers and staff, university faculty, 501(c)(3) nonprofit employees, certain hospital employees, and some ministers.

Does the age-55 separation rule affect a Gold IRA rollover?

The age-55 rule mainly affects penalty-free withdrawals from a 403(b) after separation at 55 or later; it does not prevent a rollover. Some educators leave part of a 403(b) in-plan for age-55 access and roll the rest to an IRA.

What is the safest rollover method from 403(b) to Gold IRA?

Most experts favor a direct trustee-to-trustee rollover, which avoids the 60-day deadline and 20% mandatory withholding that apply to indirect rollovers where the participant receives the funds first.

How do TIAA and annuity vendors affect rollovers?

TIAA and insurers such as Voya and AXA may use annuity contracts with surrender schedules and payout windows, which can restrict when and how balances can be moved. Detailed contract information is needed before planning a rollover.

Is a 403(b) to Gold IRA rollover a taxable event?

A properly structured direct rollover from a pre-tax 403(b) to a Traditional Gold IRA, or from a Roth 403(b) to a Roth Gold IRA, is generally not taxable at the time of rollover, though future distributions from the IRA will be taxed according to account type.

Can only part of a 403(b) be rolled into a Gold IRA?

Yes. Most plans allow partial rollovers, enabling participants to move a chosen percentage or dollar amount into a Gold IRA while leaving the rest in mutual funds or annuities.

Are Gold IRAs appropriate for all educators?

Not necessarily. Gold IRAs can provide diversification and tangible-asset exposure, but they also involve volatility, fees, and liquidity considerations. Suitability depends on overall retirement income, risk tolerance, and time horizon.

How are RMDs handled after a 403(b) rollover to a Gold IRA?

After a rollover, the Gold IRA becomes subject to IRA RMD rules, with distributions generally required starting at age 73 under current SECURE Act 2.0 provisions. RMDs can be taken in cash (by selling metals) or in-kind (by distributing coins/bars).

What if a 403(b) has both pre-tax and Roth contributions?

Pre-tax 403(b) balances typically roll into a Traditional Gold IRA, while Roth 403(b) balances roll into a Roth Gold IRA, preserving tax treatment for each source.

Article reviewed and edited by Daniel — independent precious-metals retirement researcher.