Educational only: This guide summarizes IRS and estate-planning material in general terms and is not financial, tax, or legal advice. Titling, probate, and tax rules are state-specific and change — an estate attorney and a tax advisor should confirm any plan. Customers should speak to a financial or tax advisor before making decisions. Goldco does not offer tax or legal advice. Past performance does not guarantee future results.

Quick Answer: Which Tangible Assets Make Sense for Heirs?

Tangible assets for heirs generally include real estate, vehicles, precious metals, jewelry, art and collectibles, and household or business equipment. These categories can provide heirs with value, but they also create practical issues around titling, appraisal, cost basis at death, and how easily the executor can raise cash for estate costs. Broadly, tangible assets are most helpful for heirs when:

- Ownership and beneficiary designations are clear — for example, properly titled real estate, well-documented vehicles, and accounts with transfer-on-death designations.

- The estate has enough liquidity — cash, marketable securities, or life insurance — to pay estate taxes, debts, and administration costs without forced sales of property.

- There is a plan for dividing high-value or sentimental items among multiple heirs, with documented instructions to reduce family conflict.

Physical precious metals — gold, silver, platinum, and palladium — fit into this picture as one category of tangible asset among several. For some estates, metals can help diversify holdings or store value, but they also raise issues around collectibles tax treatment, storage, and fair division among heirs. Past performance does not guarantee future results.

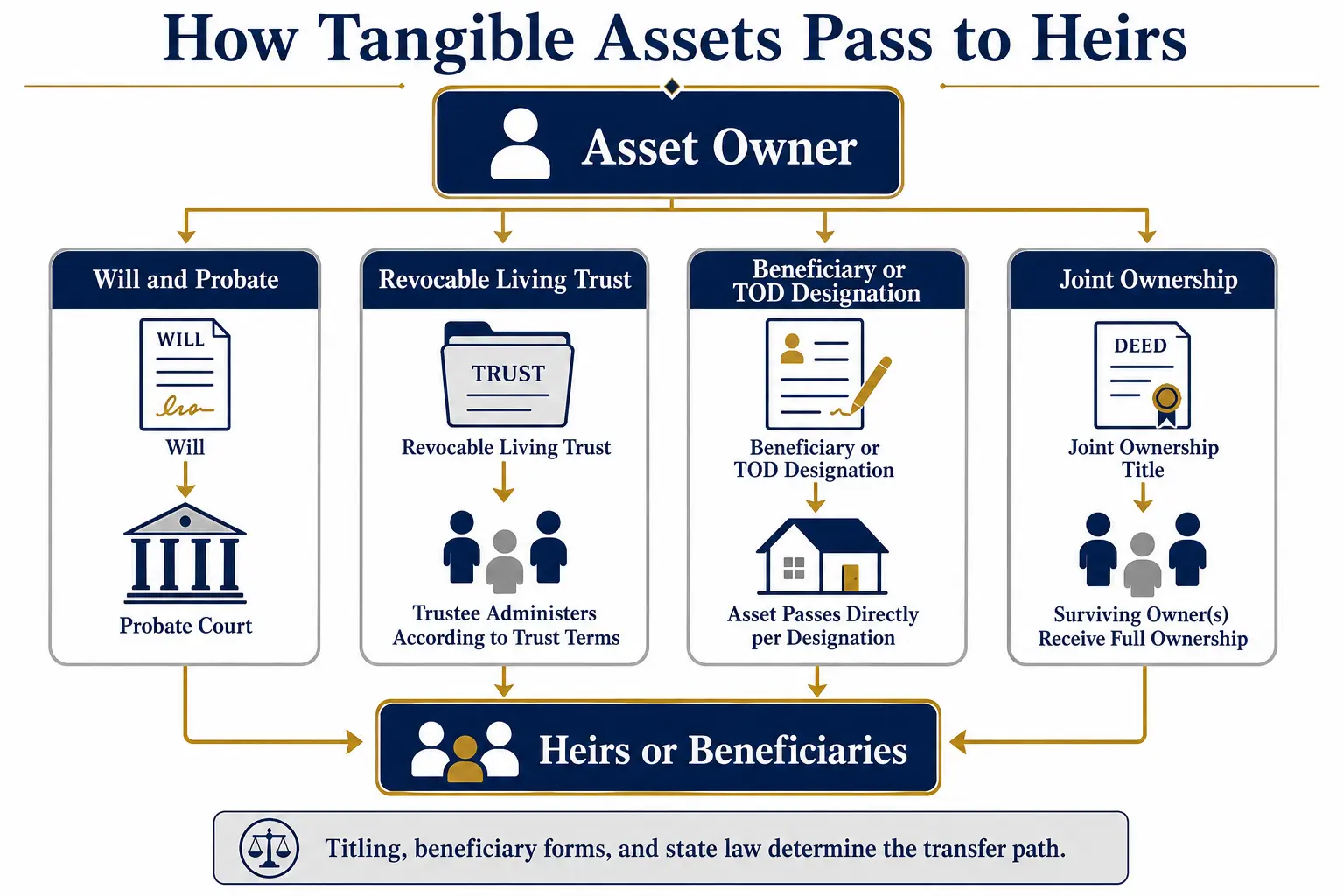

How Tangible Assets Pass to Heirs (Will, Trust, Beneficiary/TOD, Probate)

Most tangible assets pass to heirs through one of four main channels. Will and probate: a will directs how probate assets are distributed under oversight of the probate court, and real estate titled solely in the decedent's name, vehicles without special designations, and many personal possessions typically pass under the will and must go through probate unless retitled or planned otherwise. Revocable living trust: assets retitled into a properly drafted and funded revocable living trust generally avoid probate and are distributed according to trust terms — estate-planning attorneys often recommend a trust structure when an estate includes substantial tangible property, minor or special-needs beneficiaries, or blended-family situations. Beneficiary designations, POD and TOD: many financial accounts allow "pay on death" or "transfer on death" designations, which transfer assets directly to named beneficiaries outside probate and generally override conflicting language in a will or trust, so misaligned beneficiary forms can disrupt an otherwise careful plan (ACTEC). Joint ownership: joint tenancy with right of survivorship often passes the decedent's interest automatically to the surviving co-owner, which can simplify transfer but may complicate equitable division if only one heir is listed as joint owner.

Because titling and beneficiary setups are state-specific and can override will provisions, consultation with a qualified estate attorney is strongly recommended when designing an estate plan for tangible assets — state bar or estate-planning counsel, not gold or IRA dealers. Goldco does not offer tax or legal advice. Customers should speak to a financial or tax advisor before making decisions. In practice, estates often combine these mechanisms: real estate may be held in a revocable living trust to avoid probate, while vehicles and small accounts might use TOD designations; bank and brokerage accounts can use TOD or POD designations that pass directly to heirs without court involvement; and personal property such as furniture, jewelry, art, and collectibles is usually governed by the will and handled by the executor unless specifically assigned in a separate memorandum allowed under state law. Regular reviews of wills, trusts, and beneficiary designations are important, especially after life events like marriage, divorce, birth of a child, or death of a named beneficiary.

The Tax Picture: Step-Up in Basis at Death and How Collectibles/Metals Are Treated

For many types of property, U.S. tax law provides a step-up in basis at death, which can materially affect heirs' future tax when assets are sold. The IRS describes "basis" as the amount of investment in property for tax purposes — usually cost, adjusted for improvements and depreciation. When property is inherited, the basis is generally reset to its fair market value on the decedent's date of death (or an alternate valuation date if elected in an estate tax return), under Internal Revenue Code section 1014 (Tax Foundation). This step-up can apply to real estate, stocks, bonds, mutual funds, art, furnishings, and many other capital assets, meaning unrealized gains during the decedent's lifetime usually are not taxed to heirs when the asset is later sold. IRS Publication 551, Basis of Assets, explains how basis is determined, including special rules for inherited property and the need to document fair market value at the time of inheritance (IRS Publication 551). Because basis calculations and potential estate tax reporting are complex, especially for large estates, consultation with a tax advisor and estate attorney is advisable. Goldco does not offer tax or legal advice.

Physical precious metals are treated differently from many other capital assets. Under federal law, many forms of bullion and coins are classified as "collectibles." IRS guidance on capital gains and losses notes that net capital gains from selling collectibles, such as coins or art, are taxed at a maximum 28% rate rather than the typical long-term capital gain rates of 0%, 15%, or 20% (IRS Topic 409). Internal Revenue Code section 408(m) specifically includes metals like gold and silver, with some exceptions, in the collectibles category (The Tax Adviser, AICPA). Short-term gains, held one year or less, are taxed as ordinary income at the taxpayer's regular rate, while long-term gains may be subject to the higher collectibles cap. This means heirs inheriting physical precious metals need to consider both the stepped-up basis (fair market value at death) and the fact that later long-term gains may be taxed at the collectibles rate. For non-metal collectibles such as art, rare coins, or memorabilia, similar tax rules apply, but authentication, provenance, and valuation can be more complex. Past performance does not guarantee future results. Customers should speak to a financial or tax advisor before making decisions. Goldco does not offer tax or legal advice.

Estate Liquidity: Why Heirs May Need Cash, and How Illiquid Assets Create Pressure

Estate liquidity refers to how much cash or readily marketable assets are available to pay taxes, debts, and administrative expenses shortly after death. Key obligations that often must be paid in cash include funeral and final medical expenses; court costs, executor fees, attorney fees, and appraisal costs; secured and unsecured debts including mortgages, credit cards, and business loans; and federal or state estate or inheritance taxes where applicable. When an estate is rich in tangible assets (real estate, metals, collectibles, vehicles) but poor in cash or liquid investments, the executor may be forced to sell property quickly to raise funds. This can lead to unfavorable sale terms, conflict among heirs who prefer to keep certain assets, or uneven distributions if some assets are sold and others retained.

Illiquid assets include property that is slow to sell or difficult to divide: real estate that needs repairs, is encumbered by liens, or sits in a less liquid market; closely held business interests, machinery, and specialized equipment; and large collections — art, rare coins, memorabilia, or bullion stored in non-transparent locations — that require specialized appraisal. Without deliberate planning, illiquid estates can increase stress on heirs and executors, especially if taxes or debts must be paid within fixed deadlines. A mix of liquid assets, such as savings accounts, money market funds, or life insurance designed to provide immediate cash, can relieve this pressure. Customers should speak to a financial or tax advisor before making decisions on estate liquidity and asset mix. Goldco does not offer tax or legal advice.

Practical Problems With Physical Valuables

Physical valuables often require professional appraisal and, in some cases, authentication to determine fair market value at death and for eventual sale or division among heirs. Typical steps include a licensed appraiser assessing real-estate fair market value as of the date of death for estate tax and basis purposes; establishing vehicle value using market guides, dealer quotes, or appraisals; and qualified appraisers or dealers providing written valuations for collectibles and metals, with third-party grading and authentication for rare coins or high-end collectibles. Accurate appraisals support equitable division among heirs and help establish cost basis at death for later tax reporting. IRS guidance emphasizes that if basis cannot be substantiated, the IRS can treat basis as zero, which can increase taxable gain on a sale (IRS Publication 551).

Physical valuables also create ongoing storage and security considerations: real estate must be insured and maintained until transfer or sale, with property taxes and utilities paid to protect value; vehicles should be stored safely, insured, and retitled promptly to avoid liability issues; and precious metals and high-value collectibles are often stored in safe-deposit boxes, professional vaults, or well-secured home safes, with appropriate insurance coverage. Failure to manage storage and insurance can expose heirs and the estate to theft, damage, or liability claims, eroding the value of tangible assets for heirs.

Sentimental and high-value tangible assets are frequent sources of family conflict, so estate-planning practitioners recommend clear instructions and communication to reduce disputes. A written statement or memorandum, where permitted by state law, can list specific items and identify which heir should receive each; certain items can be sold and the cash divided when an item cannot be fairly shared but has strong sentimental or financial value; and for collections or many similar items, some executors use a structured selection order or "lottery" so heirs can choose items in turn under agreed rules. Open discussion of expectations with heirs during life can also reduce misunderstandings and resentment. Goldco does not offer tax or legal advice.

Where Physical Precious Metals and a Precious-Metals IRA Fit

Physical gold, silver, platinum, and palladium can be part of an estate's tangible asset mix, often held as bars, coins, or rounds. In a general taxable account or in physical form outside retirement accounts, metals are treated as collectibles for tax purposes when sold. For heirs, inheriting physical metals means metals receive a stepped-up basis to fair market value at death, similar to other capital assets; later sales may trigger collectibles-level capital gains rates, up to a 28% maximum for long-term gains; and storage, security, insurance, and logistical access can be more complex than for cash or publicly traded securities. As with other tangible assets, metals should be treated as one component of an overall estate strategy, not a default or promoted solution. Past performance does not guarantee future results. Customers should speak to a financial or tax advisor before making decisions. Goldco does not offer tax or legal advice.

A "gold IRA" or broader precious-metals IRA is a type of self-directed individual retirement arrangement that holds IRS-approved metals inside a tax-advantaged account rather than directly in the owner's name, and inheritance rules for IRAs differ significantly from inheriting metal outright. Inherited traditional IRAs are subject to required minimum distribution rules based on whether the beneficiary is a surviving spouse, an eligible designated beneficiary, or another individual (IRS Publication 590-B). For many non-spouse designated beneficiaries, the SECURE Act and subsequent IRS guidance require that the entire inherited IRA be paid out by the end of the tenth year following the year of death (the "10-year rule"), with eligible designated beneficiaries allowed different timing (Vanguard). Distributions from inherited traditional IRAs are generally taxable as ordinary income, whereas sales of inherited metals outside an IRA generate capital gains or losses based on stepped-up basis and collectibles treatment. These differences mean that leaving metals inside an IRA for heirs involves retirement-account distribution rules and tax treatment distinct from simply passing down physical bullion. For more detail, see Gold IRA Beneficiary Rules, Inherited Gold IRA Rules, Estate Planning With a Gold IRA, and How the SECURE Act Affects a Gold IRA. Because IRA rules are technical and subject to change, IRS publications and direct professional advice are essential. Goldco does not offer tax or legal advice. Further context on allocation and retirement planning with metals appears in How Much Gold Should Be Held in Retirement and the Gold IRA Suitability Quiz, as part of a broader retirement framework rather than a single solution.

Making the Transfer Smooth: Documentation, an Inventory, and Communicating the Plan

A practical estate plan for tangible assets for heirs starts with a clear inventory and documentation of ownership. Helpful steps include creating a list of real estate, vehicles, metals, collectibles, business equipment, and significant household items — with location, approximate value, and how each asset is titled; keeping copies of deeds, titles, purchase records, appraisals, and authentication certificates with estate-planning documents; and linking each significant asset to will provisions, trust terms, or beneficiary designations so the executor can quickly match property to instructions. Well-organized records reduce the risk of assets being overlooked, misvalued, or misdistributed during estate administration.

An owner can align titling and beneficiary designations with the estate plan so tangible assets pass in predictable ways: moving appropriate assets into a revocable living trust where trust administration offers more control than TOD alone; using TOD or POD designations for certain accounts where simple, direct transfer is desired, and keeping designation forms in sync with the will and trust; and avoiding ad hoc joint ownership arrangements that conflict with the intended distribution among multiple heirs. Because trust law, probate rules, and TOD deeds vary by state, collaboration with an estate attorney is important when choosing which assets belong in a trust, which should use beneficiary designations, and which remain probate assets under the will. Finally, many estate practitioners emphasize communication: discussing the overall plan — including why certain heirs may receive specific assets or differing shares — can lower the chance of surprise and resentment; explaining choices around illiquid assets such as a family home or closely held business helps heirs understand whether a sale, co-ownership, or buyout is anticipated; and identifying the executor and trustee and clarifying their role in dividing or selling tangible property sets expectations in advance. This calm, practical approach helps ensure that what is left behind remains a benefit rather than a burden. Customers should speak to a financial or tax advisor before making decisions related to tax, liquidity, or IRA planning, and should engage an estate attorney for titling, will, and trust questions. Goldco does not offer tax or legal advice.

Frequently Asked Questions

What is a step-up in basis at death?

A step-up in basis at death is a tax rule under Internal Revenue Code section 1014 that generally resets the tax basis of inherited property to its fair market value at the date of death (or an alternate valuation date if elected), rather than the original purchase price. This can significantly reduce taxable capital gains when heirs later sell inherited assets such as real estate or securities.

How are physical precious metals and collectibles taxed for heirs?

Physical metals like gold and silver held outside an IRA are treated as collectibles, so long-term capital gains from their sale are subject to a maximum 28% federal tax rate, higher than the standard long-term capital gain rate in many cases. Short-term gains are taxed at ordinary income rates, and all gains must be reported on the appropriate IRS forms such as Form 8949 and Schedule D.

How do transfer-on-death (TOD) and beneficiary designations affect probate?

Accounts and certain assets with valid beneficiary, POD, or TOD designations generally pass directly to the named beneficiaries outside of probate and typically override conflicting instructions in a will. This can simplify transfer for those specific assets but may complicate overall estate planning if designations are not coordinated with the will or trust.

How can an executor fairly divide tangible property among multiple heirs?

Executors and estate planners often use a combination of specific bequests, written memoranda detailing who receives which items, optional sale-and-split instructions for high-value assets, and structured selection processes such as rotation or lottery systems. Clear documentation and communication with heirs before and after death help reduce disputes over sentimental and valuable items.

How do inherited IRAs differ from inheriting metals outright?

Inherited traditional IRAs must follow IRS distribution rules: many non-spouse designated beneficiaries must empty the account by the end of the tenth year after the owner's death, with required minimum distributions in some circumstances, and distributions usually taxed as ordinary income. Inheriting metals outright instead involves stepped-up basis and later capital gains tax under collectibles rules when the metals are sold.

Conclusion

The tangible assets that make the most sense for heirs are the ones that transfer cleanly, value reliably, and sit inside an estate with enough liquidity to cover taxes and debts without forced sales. Step-up in basis softens the tax on most inherited property, collectibles and metals carry their own 28% ceiling, and IRA-held metal follows entirely separate distribution rules. Clear titling, an accurate inventory, and open communication with heirs turn a collection of possessions into a plan. Precious metals belong in that plan as one option among several, never as the whole answer.

Sources

- Internal Revenue Service. Publication 551, Basis of Assets.

- Internal Revenue Service. Topic No. 409, Capital Gains and Losses.

- Internal Revenue Service. Publication 590-B (Distributions from IRAs).

- Internal Revenue Service. Gifts & Inheritances FAQ.

- Tax Foundation. Step-Up in Basis (glossary).

- The Tax Adviser (AICPA). Taxation of Collectibles.

- American College of Trust and Estate Counsel (ACTEC). Pitfalls of Pay-on-Death Accounts.

- Fidelity. What Is a Step-Up in Basis?.

- Vanguard. RMD Rules for Inherited IRAs.

- University of Nebraska Extension. Estate Planning and Stepped-Up Tax Basis.

Article reviewed and edited by Daniel M. — editor, 401kToGoldIRA.org. A neutral estate/legacy guide sourced to the IRS, the Tax Foundation, the AICPA's Tax Adviser, ACTEC, Fidelity, Vanguard, and university extension programs; educational only, not financial, tax, or legal advice. An estate attorney should confirm titling, will, and trust decisions.