Educational only: This article summarizes IRS rules and public law in general terms. It is not financial, tax, or legal advice. Tax treatment depends on the account, transaction, and individual circumstances. Customers should speak to a financial or tax advisor before making decisions involving taxes, RMDs, rollovers, Roth conversions, or estate planning. Goldco does not offer tax or legal advice. Past performance does not guarantee future results.

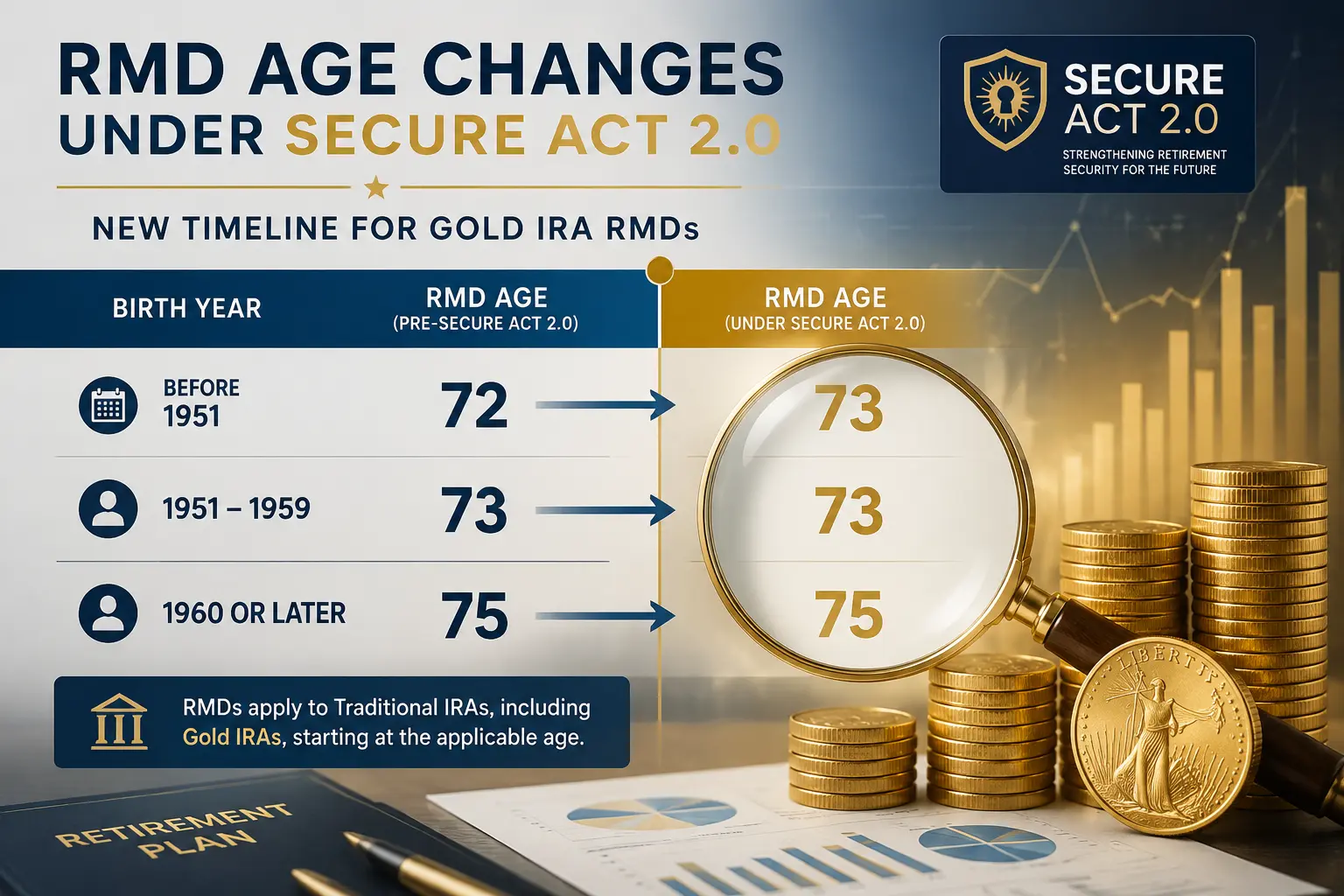

Under SECURE 2.0, traditional Gold IRA owners generally begin required minimum distributions at age 73 (rising to age 75 for those who reach 74 after 2032), and most non-spouse heirs must now empty an inherited IRA within 10 years.

Source: IRS — Required Minimum Distributions FAQs. A Gold IRA has no separate rules; it follows the RMD, contribution, and inheritance rules of the underlying traditional or Roth IRA.

Key takeaways

- A Gold IRA follows the rules of its underlying traditional or Roth IRA — SECURE 2.0 does not create a separate metals regime.

- RMD age is 73 now, moving to 75 for individuals who reach age 74 after December 31, 2032.

- The inherited-IRA 10-year rule requires many non-spouse beneficiaries to fully distribute the account within 10 years of the owner's death.

- The missed-RMD excise tax is generally 25%, potentially reduced to 10% if corrected within the applicable window.

- Roth IRA owners take no lifetime RMDs; eligible designated beneficiaries may follow different timing than the 10-year rule.

A Gold IRA does not receive a separate set of SECURE 2.0 rules. For federal tax purposes, the term generally describes a traditional or Roth individual retirement account that holds qualifying precious metals. The tax rules follow the type of IRA, while separate Internal Revenue Code rules control which coins and bullion may be held. SECURE 2.0 may change when distributions must begin, how inherited accounts must be distributed, and how certain retirement contributions are treated. It does not create a new tax exemption for gold, remove IRA custody requirements, or allow account owners to take personal possession of IRA metals without distribution consequences.

Quick Answer: How SECURE 2.0 Touches a Gold IRA

SECURE 2.0 affects Gold IRAs mainly through the following changes:

- The current required minimum distribution age is generally 73.

- The applicable RMD age is scheduled to rise to 75 for individuals who reach age 74 after December 31, 2032.

- Roth IRAs remain exempt from lifetime RMDs for their original owners.

- Designated Roth accounts in workplace plans are no longer subject to lifetime RMDs beginning with 2024.

- Higher catch-up limits apply to workplace-plan participants who turn 60 through 63 during the year.

- A Roth catch-up rule applies in 2026 to certain higher-paid workplace-plan participants.

- The IRA catch-up contribution amount is $1,100 for 2026.

- Many non-spouse inherited-IRA beneficiaries remain subject to the 10-year distribution rule.

- The excise tax for a missed RMD is generally 25%, potentially reduced to 10% when corrected within the applicable correction period.

These rules apply according to the legal account type: a traditional self-directed IRA holding gold generally follows traditional IRA distribution rules, and a Roth self-directed IRA generally follows Roth IRA rules. Customers should speak to a financial or tax advisor before making decisions involving taxes, RMDs, rollovers, Roth conversions, or estate planning. Goldco does not offer tax or legal advice.

What SECURE 2.0 Means for a Gold IRA

The SECURE 2.0 Act was enacted as Division T of the Consolidated Appropriations Act, 2023 (Public Law 117-328). It amended numerous provisions of federal retirement law, including rules governing RMD ages, catch-up contributions, Roth accounts, and penalties. The law does not establish "Gold IRA" as a separate federal tax category. In practical terms, an account commonly called a Gold IRA is an IRA whose custodian permits qualifying precious metals; its contribution, rollover, distribution, beneficiary, and tax rules are based on whether the account is a traditional IRA, Roth IRA, SEP IRA, or SIMPLE IRA. So SECURE 2.0 changes the retirement-account framework around the metals — it does not change gold into a separate type of retirement plan.

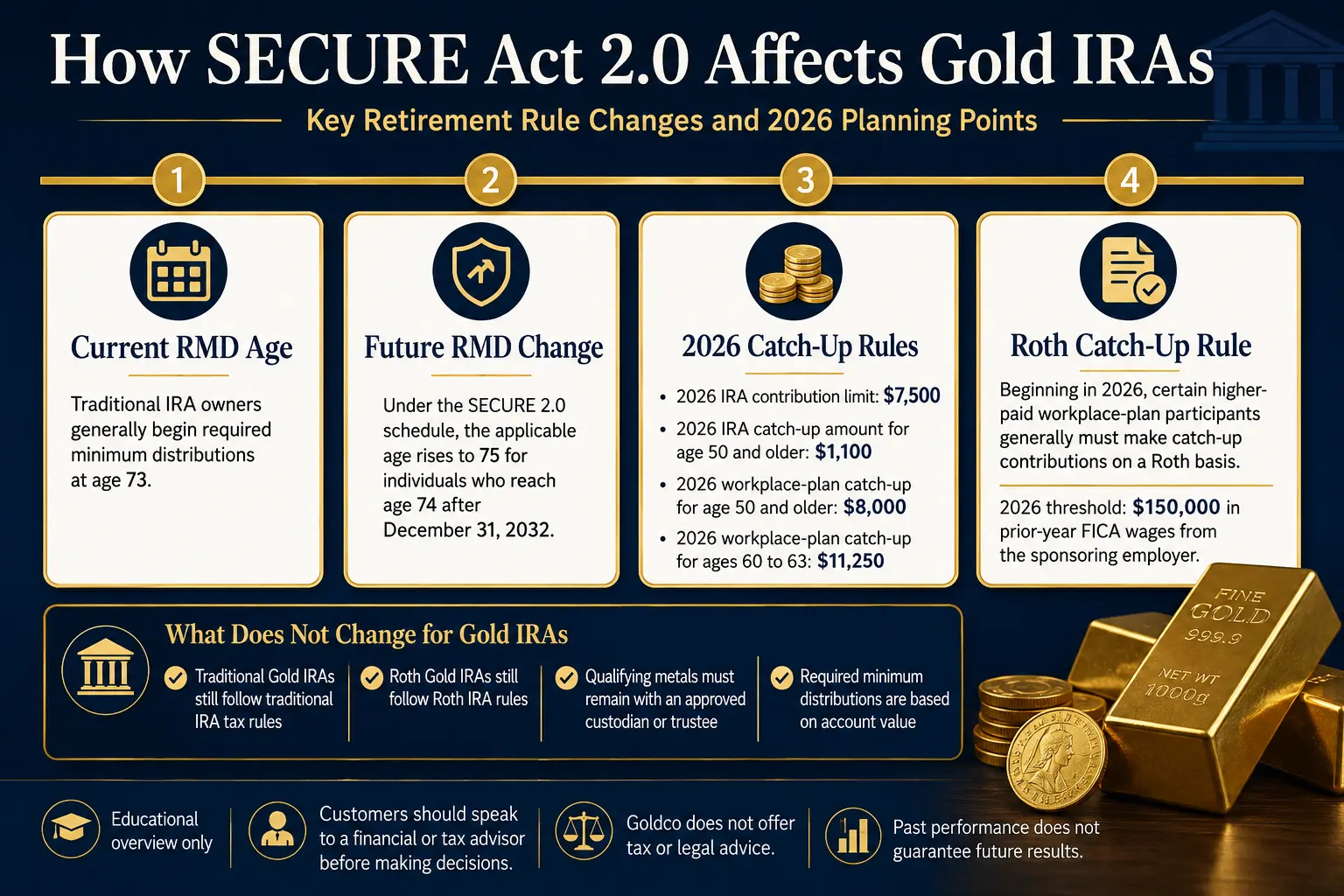

Current RMD Age Under SECURE 2.0

The IRS states that traditional IRA, SEP IRA, SIMPLE IRA, and retirement-plan owners generally begin RMDs at age 73 under the current rules. Roth IRA owners do not take lifetime RMDs from their own Roth IRAs. SECURE 2.0 created a birth-date schedule:

- Individuals who reached age 72 before January 1, 2023, remained under the earlier applicable-age rules.

- Individuals who reach age 72 after December 31, 2022, and reach age 73 before January 1, 2033, generally have an applicable RMD age of 73.

- Individuals who reach age 74 after December 31, 2032, generally have an applicable RMD age of 75.

Based on that statutory schedule, individuals born from 1951 through 1959 generally fall under age 73, while individuals born in 1960 or later generally fall under age 75. The increase to age 75 does not mean every retirement saver can wait until 75 — the applicable age depends on the statutory birth-date schedule.

The first RMD deadline can create two distributions in one year

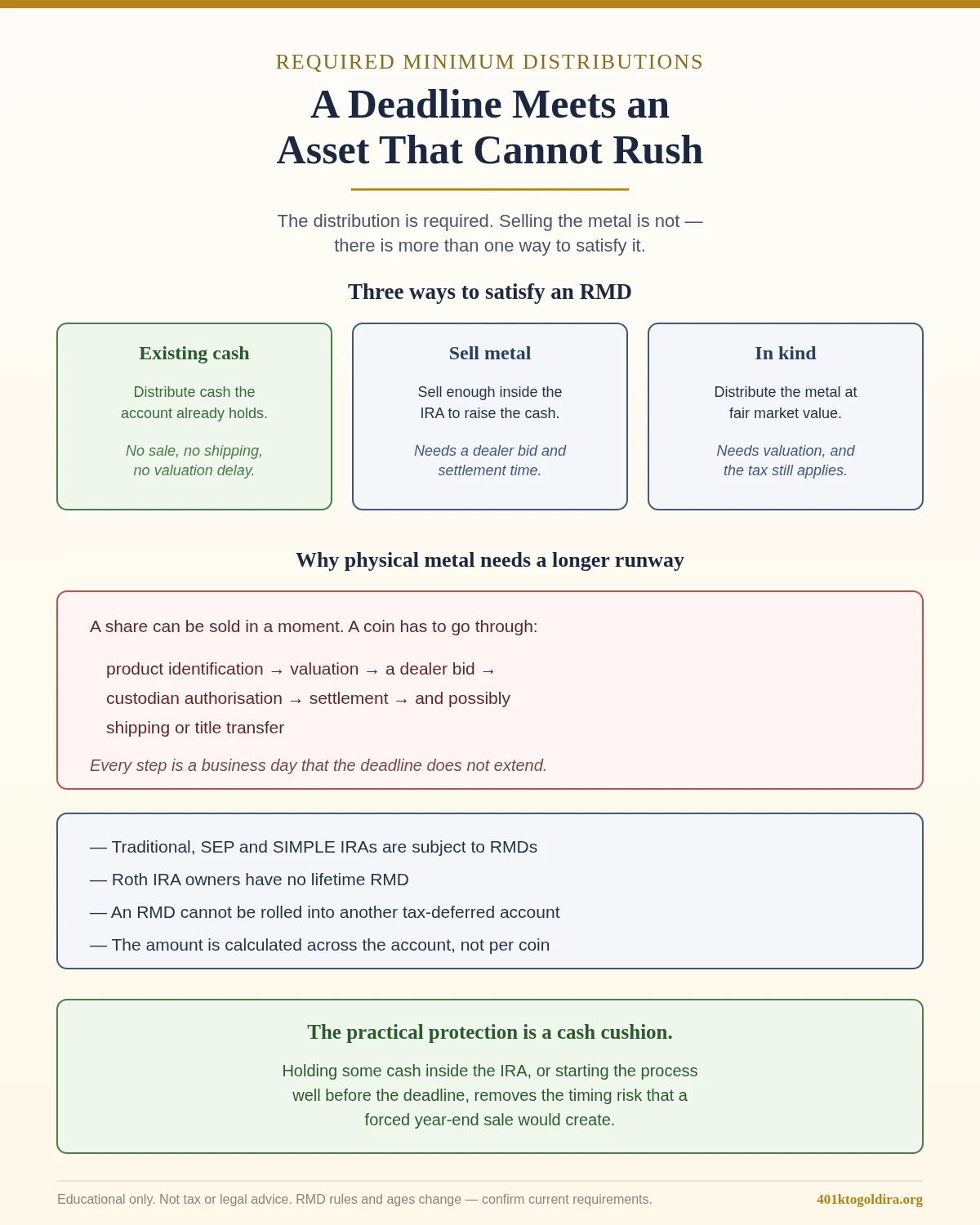

For a traditional IRA owner subject to age 73, the first RMD is generally due by April 1 of the year after the year in which age 73 is reached. Later RMDs are generally due by December 31 each year. Delaying the first RMD until the following April does not postpone the second RMD — it remains due by December 31 of that same calendar year, which can place two taxable IRA distributions in one year. A customer with a traditional Gold IRA may therefore need a distribution plan before reaching the applicable age, which may involve retaining sufficient cash inside the account, selling part of the metals, taking an in-kind distribution where the custodian permits it, or satisfying aggregated traditional IRA RMDs from another traditional IRA. The Gold IRA RMD calculator can illustrate the math. Customers should speak to a financial or tax advisor before making decisions involving RMD timing or taxable distributions. Goldco does not offer tax or legal advice.

How RMDs Apply to Physical Gold Held in an IRA

SECURE 2.0 did not create a metals-specific RMD formula. An RMD is generally calculated by dividing the prior December 31 account balance by the applicable IRS life-expectancy factor, so a custodian must have an account value for the metals. Form 5498 reports the fair market value of an IRA, and IRS reporting rules also address assets that do not have readily available market values. An IRA owner with several traditional IRAs must calculate the RMD separately for each IRA; the calculated amounts may then be totaled and withdrawn from one or more of those traditional IRAs. This aggregation rule can matter when one traditional IRA holds physical metals and another holds cash or publicly traded assets — the total obligation may be taken from another traditional IRA, provided each account's RMD is first calculated correctly. The rule does not generally permit a 401(k) RMD to be satisfied from an IRA. Required minimum distributions are also not eligible for rollover treatment: a distribution cannot first be treated as an RMD and then placed back into another IRA as a normal rollover.

Higher Catch-Up Contribution Limits in 2026

SECURE 2.0 added a higher workplace-plan catch-up limit for participants who turn 60, 61, 62, or 63 during the calendar year. The provision first applied in 2025 and remains relevant in 2026. For 2026:

- The regular employee deferral limit for most 401(k), 403(b), governmental 457 plans, and the federal Thrift Savings Plan is $24,500.

- The general age-50 catch-up limit for those plans is $8,000.

- The higher catch-up limit for participants turning 60 through 63 is $11,250.

A qualifying participant using the higher limit could therefore defer as much as $35,750, subject to plan terms, compensation, and other applicable limits. These amounts were confirmed by the IRS in Notice 2025-67 and the IRS 2026 contribution-limit announcement.

Does the higher workplace catch-up limit apply directly to a Gold IRA?

No. The $11,250 limit applies to eligible catch-up contributions made through specified workplace retirement plans. It is not a separate Gold IRA contribution allowance. The connection to a Gold IRA is indirect: additional money accumulated in an employer plan could later become eligible for rollover after a qualifying event, subject to the distributing plan's rules. A rollover is not treated as a regular annual IRA contribution, but it must satisfy the federal rollover rules. The rollover guide covers those mechanics. Customers should speak to a financial or tax advisor before making decisions involving contributions or rollovers. Goldco does not offer tax or legal advice.

The 2026 IRA contribution and catch-up limits

SECURE 2.0 indexed the IRA catch-up contribution amount for inflation. For 2026, the regular combined traditional-and-Roth IRA contribution limit is $7,500. The catch-up amount for individuals age 50 or older is $1,100, producing a possible combined limit of $8,600, subject to taxable compensation, income restrictions, deduction rules, and other eligibility requirements. Opening a self-directed IRA that holds metals does not provide an additional contribution limit beyond the federal IRA limit. Rollovers are governed separately from regular annual contributions and may exceed the annual limit because they represent retirement assets moved from another eligible account rather than a new annual contribution.

The Roth Catch-Up Rule Beginning in 2026

Beginning in 2026, certain participants making catch-up contributions to workplace plans with Roth features must make those catch-up contributions on a Roth basis when prior-year FICA wages from the employer sponsoring the plan exceeded $150,000 (the inflation-adjusted threshold applicable for 2026). The original statutory threshold was $145,000, subject to cost-of-living adjustments. IRS guidance provided an administrative transition period for 2024 and 2025, which delayed enforcement of the mandatory Roth treatment until 2026. The Treasury Department and IRS issued final regulations in September 2025; provisions relating to the Roth catch-up requirement generally have a formal applicability date for taxable years beginning after December 31, 2026, but the statutory requirement and transition guidance make 2026 the first operational year for the rule as described by the IRS.

How the Roth catch-up rule can affect a later Gold IRA rollover

The rule applies to the workplace-plan contribution, not directly to an existing Gold IRA. Its later effect can appear when workplace-plan assets are rolled over. An eligible distribution from a designated Roth account may generally be rolled into another designated Roth account or a Roth IRA — it may not be rolled into a traditional IRA. Pretax workplace-plan amounts may generally be directed to a traditional IRA, while eligible designated Roth amounts may be directed to a Roth IRA. A self-directed Roth IRA may hold qualifying precious metals if the account, custodian, metals, and storage arrangement satisfy the applicable IRA rules. Roth tax character must remain separate from traditional pretax IRA assets unless a taxable Roth conversion is completed under the conversion rules.

Roth RMD Changes

Roth IRA owners were already exempt from lifetime RMDs before SECURE 2.0. Beneficiaries of Roth IRAs remain subject to post-death distribution rules. SECURE 2.0 extended similar lifetime-RMD treatment to designated Roth accounts in 401(k) and 403(b) plans for taxable years beginning after December 31, 2023, removing the former need to roll designated Roth plan money into a Roth IRA solely to avoid lifetime workplace-plan RMDs. This provision does not make traditional Gold IRA assets Roth assets — a traditional self-directed IRA holding metals remains subject to traditional IRA RMD rules, and changing traditional IRA assets to Roth status generally requires a Roth conversion, which may create taxable income. Customers should speak to a financial or tax advisor before making decisions involving Roth conversions or RMDs. Goldco does not offer tax or legal advice.

The Inherited-IRA 10-Year Rule and Gold IRAs

The original SECURE Act of 2019 established the 10-year rule for many designated beneficiaries. SECURE 2.0 did not repeal that framework, although it made related retirement-distribution changes and directed further regulatory implementation. Under the 10-year rule, a covered beneficiary generally must empty the inherited IRA by December 31 of the year containing the tenth anniversary of the original owner's death (for example, when an owner dies during 2025, the deadline is generally December 31, 2035). Full detail on inheritance mechanics is in the inherited Gold IRA rules and beneficiary rules guides.

When the owner died before the required beginning date

When the original IRA owner died before the required beginning date and the 10-year rule applies, no distribution is generally required during years one through nine. The remaining account must still be distributed by the end of the tenth year.

When the owner died on or after the required beginning date

When the original owner died on or after the required beginning date, a non-eligible designated beneficiary subject to the 10-year rule generally must continue annual beneficiary RMDs and fully distribute the account by the end of year ten. Final Treasury regulations apply the annual distribution framework in addition to the year-ten deadline in these circumstances. The IRS provided penalty relief for certain missed inherited-account RMDs through 2024; that transitional relief did not eliminate the underlying 10-year rule and should not be treated as continuing automatically into 2025 or 2026.

Eligible designated beneficiaries

Eligible designated beneficiaries can receive different treatment. The category generally includes a surviving spouse, a minor child of the account owner, a disabled individual, a chronically ill individual, and an individual not more than 10 years younger than the account owner. Depending on the circumstances, an eligible designated beneficiary may qualify for life-expectancy distributions or other special rules.

Gold-specific inherited-account planning issues

An inherited Gold IRA follows the inherited-IRA rules — physical metals do not remove the year-ten deadline or any annual RMD obligation. Because the account holds physical assets, the beneficiary and custodian may need to address valuation, available cash, metal sales, distribution processing, and any permitted in-kind distribution. Leaving the entire distribution obligation until the final year could concentrate taxable income and require a large sale or distribution of metals. Customers should speak to a financial or tax advisor before making decisions involving inherited IRAs, beneficiary designations, estate planning, or distributions. Goldco does not offer tax or legal advice.

Reduced Penalties for Missed RMDs

SECURE 2.0 reduced the excise tax associated with an RMD shortfall. The tax is generally 25% of the amount not distributed as required, and it may be reduced to 10% when the shortfall is corrected within the statutory correction window and the applicable filing requirements are met. The IRS may also waive the excise tax when the shortfall resulted from reasonable error and reasonable steps are being taken to correct it; Form 5329 and an explanatory statement may be required. A lower penalty does not make an RMD optional — a traditional Gold IRA owner or inherited-IRA beneficiary must still arrange the required distribution by the applicable deadline.

Rules SECURE 2.0 Did NOT Change for Gold IRAs

- Qualifying-metal requirements remain. Most metals and coins are treated as collectibles for IRA purposes unless an exception applies; the exception covers specified coins and qualifying gold, silver, platinum, or palladium bullion that meets the legal requirements.

- Custodian or trustee possession remains required. Qualifying bullion must be held in the physical possession of a bank or approved nonbank trustee, and qualifying IRA coins must remain in the possession of the IRA custodian or trustee. Personal possession by the owner or beneficiary can cause the metals to be treated as distributed.

- Prohibited-transaction rules remain. When an IRA owner or beneficiary engages in a prohibited transaction, the account can stop being treated as an IRA as of the first day of that tax year and can be treated as distributing its assets at fair market value.

- No separate annual contribution limit. The regular IRA contribution limit applies across traditional and Roth IRA contributions; a self-directed custodian or physical-metal asset does not create an additional annual allowance.

- RMDs remain based on account value, not metal weight. The formula uses the prior year-end value and the applicable factor — the number of coins or ounces does not replace the federal dollar-value calculation.

Common Misconceptions

"SECURE 2.0 moved every RMD age to 75"

Incorrect. Age 73 remains the applicable age for many current retirees. Age 75 applies under the later statutory schedule to individuals who reach age 74 after December 31, 2032.

"The $11,250 catch-up can be contributed directly to a Gold IRA"

Incorrect. The $11,250 figure is the 2026 catch-up limit for qualifying participants turning 60 through 63 in specified workplace retirement plans. The 2026 IRA catch-up amount is $1,100.

"Roth catch-up contributions can later be rolled into a traditional Gold IRA"

Designated Roth distributions generally may be rolled to another designated Roth account or a Roth IRA, not to a traditional IRA. A self-directed Roth IRA holding qualifying metals may be an available destination when all rollover, custody, and asset rules are satisfied.

"Physical gold removes inherited-IRA distribution deadlines"

Physical metals do not override the beneficiary rules. A covered inherited Gold IRA remains subject to the applicable annual RMD and year-ten distribution requirements.

Frequently Asked Questions

Does SECURE 2.0 change the RMD age for a traditional Gold IRA?

Yes. A traditional Gold IRA follows the federal RMD age applicable to traditional IRAs. The current general age is 73, with age 75 applying later under the statutory birth-date schedule.

Are Roth Gold IRAs subject to lifetime RMDs?

An original Roth IRA owner is not required to take lifetime RMDs. Beneficiaries remain subject to post-death distribution rules.

What is the 2026 IRA catch-up contribution?

The 2026 IRA catch-up contribution is $1,100 for individuals age 50 or older. Combined with the $7,500 regular limit, the potential total is $8,600, subject to the applicable eligibility rules.

Does the mandatory Roth catch-up rule apply to Gold IRA contributions?

The mandatory Roth catch-up rule applies to certain catch-up contributions in workplace plans. It does not convert ordinary annual Gold IRA contributions into workplace-plan catch-up contributions.

Can an inherited Gold IRA remain open beyond ten years?

A beneficiary subject to the 10-year rule must fully distribute the inherited IRA by the end of the tenth year. Different rules may apply to eligible designated beneficiaries and certain non-individual beneficiaries.

Can a Gold IRA RMD be rolled into another IRA?

No. An amount treated as a required minimum distribution is not eligible for rollover treatment.

Update Log

- 2026: Initial publication. Figures reflect IRS 2026 announcements (Notice 2025-67, the IRS 2026 contribution-limit release) and the SECURE 2.0 statute (Public Law 117-328). Confirm current figures with the IRS or a tax professional before acting.

Sources

- Internal Revenue Service. Required Minimum Distributions FAQs.

- Internal Revenue Service. Retirement Topics — RMDs.

- Internal Revenue Service. Publication 590-B (Distributions from IRAs).

- Internal Revenue Service. Publication 590-A (Contributions to IRAs).

- U.S. Government Publishing Office. SECURE 2.0 Act — Public Law 117-328.

- Internal Revenue Service. N 23 54.

- Internal Revenue Service. Retirement Topics — Catch-Up Contributions.

- Internal Revenue Service. N 25 67.

- Internal Revenue Service. 401k limit increases to 24500 for 2026 ira limit increases to 7500.

- Internal Revenue Service. N 23 62.

- Internal Revenue Service. 2025 40 IRB.

- Internal Revenue Service. Treasury irs issue final regulations on new roth catch up rule other s.

- Internal Revenue Service. 2024 33 IRB.

- Internal Revenue Service. N 24 35.

- Internal Revenue Service. Retirement Topics — Beneficiary.

- Internal Revenue Service. Investments in Collectibles in IRA Accounts.

- Internal Revenue Service. Rollovers of Retirement Plan and IRA Distributions.

- Internal Revenue Service. Rollover chart.

- Internal Revenue Service. Rollovers of after tax contributions in retirement plans.

- Internal Revenue Service. Retirement topics designated roth account.

- Internal Revenue Service. Rmd comparison chart iras vs defined contribution plans.

- Internal Revenue Service. Form 5498 asset information reporting codes and common errors.

- Internal Revenue Service. I1099r.

Article reviewed and edited by Daniel M. — editor, 401kToGoldIRA.org. Sourced to IRS.gov and the SECURE 2.0 statute; educational only, not tax or legal advice.