Educational only: This is a balanced, evidence-based examination, not a recommendation to buy silver. It summarizes reputable data and primary sources in general terms and is not financial, tax, or legal advice. Customers should speak to a financial or tax advisor before making decisions. Goldco does not offer tax or legal advice. Past performance does not guarantee future results.

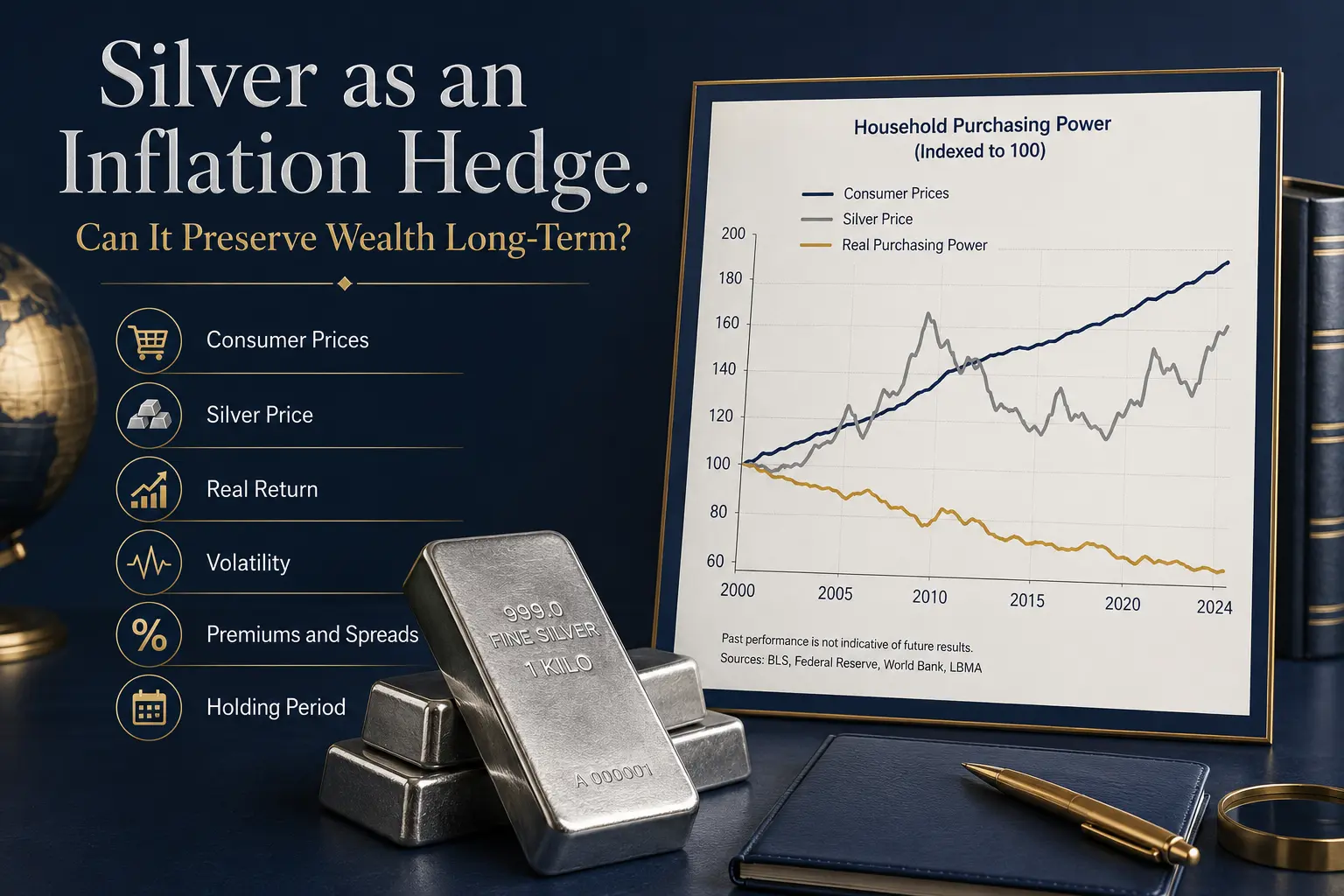

Silver's inflation link is weak and unstable. When silver set a new nominal record in 2025, its 1980 peak adjusted for inflation is estimated at over $200 per ounce — meaning a buyer at that peak lost purchasing power for ~45 years even as prices kept rising.

Source: Barchart — inflation-adjusted 1980 silver peak. Silver has no contractual link to inflation; its price is set by the market.

Key takeaways

- Silver is not a reliable inflation hedge — its relationship with CPI is weak, unstable, and highly dependent on the entry price and holding period.

- Entry price dominates: silver bought near the 1980 peak had not recovered its real value ~45 years later, while silver bought at depressed prices far outpaced inflation.

- Silver's annualized volatility has been up to twice gold's over 20 years (BlackRock), because it is a smaller market driven by both investment and industrial demand.

- About 60% of silver consumption is industrial (electronics, solar, semiconductors), tying it to economic growth — which can help or hurt during inflation.

- TIPS have a contractual CPI link that silver lacks; silver may act as a diversifier with inflation sensitivity, not a stand-alone purchasing-power solution.

Is Silver a Reliable Inflation Hedge?

The honest answer is not consistently. A reliable inflation hedge should preserve purchasing power when the general price level rises. Silver has done that during some periods, but its relationship with inflation has been weak, unstable, and highly dependent on the starting price and holding period. A clear historical warning came from silver's 1980 peak: in October 2025, silver finally moved above its old nominal record after about 45 years, yet the inflation-adjusted 1980 high is estimated at over $200 per ounce — far above the new record (Barchart). That does not mean silver always fails; it means a purchase made at an extreme price can lose purchasing power for decades, even when inflation keeps raising the cost of everyday goods.

BlackRock's iShares research describes silver as a higher-volatility, more cyclical metal that has not consistently provided the same portfolio-stabilizing benefits as gold, noting that silver's price reflects both investment flows and industrial demand — which makes the result less like a direct inflation link and more like a changing commodity cycle (iShares). Silver may therefore work better as a diversifier with inflation sensitivity than as a stand-alone purchasing-power solution. The Protect Retirement Purchasing Power guide explains why inflation planning usually works better when several tools are combined.

What Does "Inflation Hedge" Actually Require of an Asset?

An inflation hedge should offset the loss of purchasing power caused by rising consumer prices. The Consumer Price Index measures changes in the prices paid by urban consumers for a broad basket of goods and services, and the Federal Reserve Bank of St. Louis notes that year-over-year changes in the CPI are commonly used to measure inflation (Federal Reserve Bank of St. Louis). A strong hedge would have a reasonably close link to that price index over the period that matters — and silver has no contract that ties its price to CPI. That distinction separates silver from Treasury Inflation-Protected Securities: TreasuryDirect states that TIPS principal rises with inflation and falls with deflation based on the CPI, and at maturity the investor receives the higher of the inflation-adjusted principal or the original principal (TreasuryDirect). Silver has no similar mechanism; its price is set by buyers and sellers in the global market.

A useful inflation test asks four questions: Direction — did the asset rise when inflation rose? Size — was the gain large enough to offset the loss of purchasing power? Timing — did the gain arrive while the higher costs were being paid? Reliability — did the relationship repeat across different inflation periods? Silver can pass parts of that test in selected windows and fail badly in others. An asset can still have a positive long-term return without being a reliable inflation hedge, and it can react strongly to an inflation scare while failing to track realized inflation over a full decade.

Does Silver's History Actually Track Inflation?

Silver's history does not show a smooth one-for-one relationship with consumer prices. The 1980-to-2025 comparison is one example: silver eventually passed its old nominal record but remained far below the old peak after adjusting for inflation (Barchart). That result matters because "store of value" claims can hide the importance of entry price — a metal bought before a major surge may preserve purchasing power, while the same metal bought near a speculative peak may not. Academic criticism also challenges the idea that a volatile market price can serve as a stable measure of purchasing power: in Bitcoin, Currencies, and Fragility, Nassim Nicholas Taleb argues that a true store of value should have low variation against a basket of goods, and notes that the late-1970s silver squeeze damaged silver's inflation-hedge role (arXiv). That paper focuses mainly on cryptocurrency, so its silver discussion should be treated as a conceptual critique rather than a final answer.

Shorter periods can tell a different story. Silver may rise when investors expect inflation, falling real interest rates, a weaker dollar, or supply shortages — but it may also fall during inflation because higher interest rates support the dollar or increase the opportunity cost of holding a metal with no cash flow. This is why inflation alone does not explain silver prices: the market also reacts to the expected policy response to inflation. Expected vs. unexpected inflation compounds this — markets can price in widely expected inflation before official data are published, so when the CPI number arrives silver may barely move because traders already acted; unexpected inflation may create a stronger response, but even that can be offset by interest-rate expectations, industrial weakness, forced selling, or a stronger dollar. No reliable primary source establishes a stable silver-to-CPI sensitivity that holds across all periods; any single correlation figure would depend on the dates, price series, inflation measure, currency, and return frequency used. The better conclusion is that the relationship changes over time.

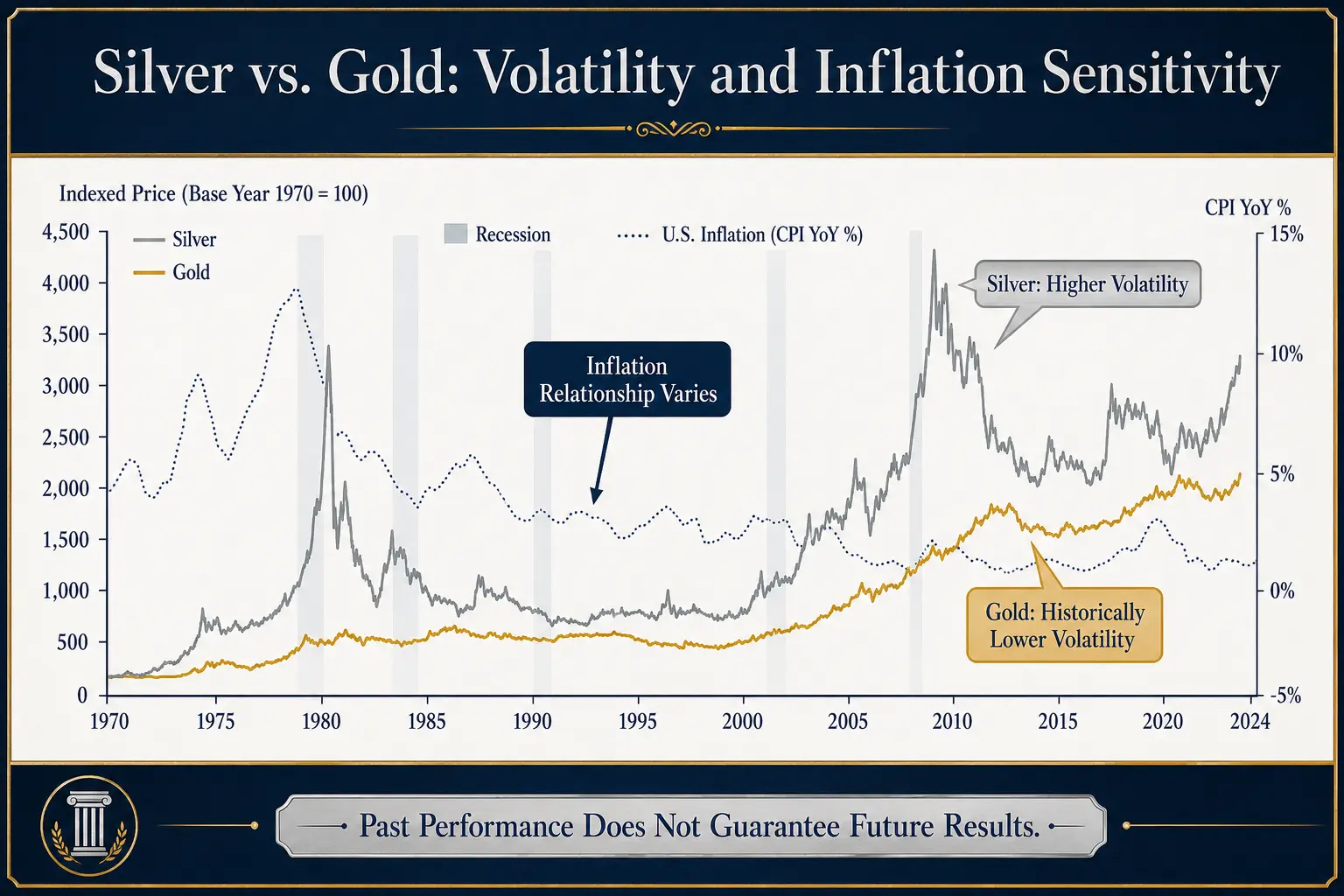

Why Is Silver More Volatile Than Gold?

Silver combines two different identities: it is a precious metal with a long monetary history, but also an industrial input used in electronics, solar panels, vehicles, grid equipment, and other technologies. Gold demand is more heavily tied to investment, reserves, jewelry, and wealth storage. BlackRock's iShares analysis states that silver's annualized volatility has been as much as twice gold's over the past 20 years, linking that difference to silver's smaller, less liquid market and its combination of investment and industrial demand (iShares). Higher volatility matters for an inflation hedge because purchasing-power protection is most useful when it is available at the right time — a retiree facing rising food, housing, or medical costs may not benefit from a metal that falls sharply during the year cash is needed, even if the price later recovers.

Silver volatility can come from changes in manufacturing demand, solar and electronics demand, mine and recycling supply, investor buying and selling, exchange-traded product flows, interest rates and real yields, the U.S. dollar, futures-market positioning, market liquidity, and price momentum and speculation. The same forces can create strong upside — but that upside potential does not make the inflation relationship stable. The Silver IRA Pros and Cons guide provides a wider review of volatility, storage costs, dealer spreads, and self-directed IRA mechanics.

How Does Industrial Demand Change Silver's Inflation Behavior?

Industrial demand can support silver prices, but it also makes the metal sensitive to economic growth. The Silver Institute reported that industrial silver demand rose 4% in 2024 to a record 680.5 million ounces, linking the increase to grid infrastructure, vehicle electrification, photovoltaic applications, electronics, and artificial-intelligence-related demand (Silver Institute). The Silver Institute is an industry organization and the report was sponsored by companies in the silver market — its figures were researched by Metals Focus, but the source should still be read as industry research. BlackRock estimated that about 60% of annual silver consumption is tied to electronics, solar panels, and semiconductors, giving silver a growth-sensitive component that gold does not have to the same degree (iShares).

This creates several possible outcomes. Inflation with strong industrial growth: silver may benefit when prices are rising, manufacturing is expanding, and investment demand is strong. Inflation with economic weakness: silver can face mixed pressure when inflation stays high but factories, construction, or consumer demand slow — monetary demand may rise while industrial demand weakens. Disinflation with falling interest rates: silver may rise even as inflation falls if lower real rates, a weaker dollar, or improved industrial expectations support the market. Strong growth without high inflation: industrial demand can support silver even when consumer inflation is moderate. These scenarios explain why silver is not a pure CPI trade — its dual monetary and industrial demand can help in some cycles and disrupt inflation protection in others. The Silver vs. Gold IRA Cost guide covers practical differences between the two metals beyond price behavior.

Is Silver a Store of Value Over Decades or a Short-Term Inflation Hedge?

Silver has a stronger historical claim as a monetary metal than as a precise short-term CPI hedge. A store of value does not need to rise every month with inflation; it needs to preserve useful purchasing power over a long horizon after costs. That test still depends heavily on the starting date. The 1980 peak shows that silver can fail the long-term test for a buyer entering at an extreme valuation — the metal did not set a new nominal record until 2025, and the inflation-adjusted hurdle remained far higher (Barchart). Different starting points produced better results: silver purchased at depressed prices before major bull markets gained far more than inflation. That range of outcomes suggests silver behaves more like a volatile commodity and monetary asset than a stable purchasing-power index.

A clean distinction is: a short-term hedge tends to rise when an inflation surprise occurs; a long-term store of value tends to preserve purchasing power across decades; a diversifier behaves differently enough from other assets to improve portfolio balance; and a speculative asset can move sharply on expectations, positioning, and sentiment. Silver may serve the store-of-value and diversifier roles in selected periods — and can also behave like the speculative one. It should not be described as a dependable substitute for an inflation-linked security. The Gold vs. Cash guide offers a related comparison between a non-yielding metal and a liquid monetary asset.

How Do Physical Costs Affect Silver's Real Return?

The silver spot price is not the same as the return received from physical bullion. A physical purchase may include a dealer premium over spot, shipping and insurance, secure storage, account or vault fees, a resale discount or dealer spread, authentication or assay costs for some products, and taxes based on the holding structure. Those costs raise the inflation hurdle: if consumer prices rise 3% while the silver price rises 4%, the real result is not automatically positive, because purchase and sale spreads can absorb the difference. Silver's lower value per ounce also means a fixed dollar allocation usually requires more weight and storage space than the same dollar amount in gold, increasing physical handling and storage friction.

Physical silver held in a self-directed IRA adds custodian, depository, and transaction costs. The IRS states that most metals are treated as collectibles in retirement accounts, with limited exceptions for specified coins and qualifying bullion, and that qualifying bullion must remain in the physical possession of a bank or approved nonbank trustee (Internal Revenue Service). Customers should speak to a financial or tax advisor before making decisions involving allocation, taxes, an IRA, a rollover, or physical silver. Goldco does not offer tax or legal advice.

Where Might a Modest Silver Allocation Fit?

Silver may fit as one small part of a diversified plan when the purpose is clear. Investor.gov explains that diversification spreads money among investments so one loss has less effect on the full portfolio, while also stating that diversification cannot prevent losses during a broad market decline (Investor.gov). The World Gold Council argues that precious metals can improve diversification because gold has historically shown different performance drivers from stocks and bonds — that research is produced by a gold-industry organization and focuses on gold rather than silver (World Gold Council). BlackRock's iShares research offers the more silver-specific caution: silver can add differentiated exposure over full market cycles, but it is more volatile and has not consistently matched gold's stabilizing role.

A proportionate review can ask: What job is silver expected to perform? Is the goal inflation sensitivity, diversification, or price appreciation? How much volatility can the full plan absorb? Are physical premiums, spreads, and storage included? Is enough cash available for near-term retirement spending? Does the portfolio already have commodity or mining exposure? Would TIPS or another inflation-linked asset address the goal more directly? And how will the position be rebalanced after a large price move? No evidence-based universal silver percentage was verified. The How Much Gold Should Be Held in Retirement guide can help frame allocation questions across precious metals without setting a personal target, and the Gold IRA Suitability Quiz can organize broader research. Customers should speak to a financial or tax advisor before making decisions about retirement allocation, silver, gold, or an IRA. Goldco does not offer tax or legal advice.

Frequently Asked Questions

Is silver a good inflation hedge?

Silver has sometimes gained during inflationary periods, but the historical relationship is not consistent. Industrial demand, interest rates, the dollar, investment flows, and speculation can outweigh the current inflation rate.

Does silver beat inflation over the long term?

The result depends heavily on the purchase date. Silver bought near the 1980 peak did not regain that purchasing power by the time it set a new nominal record in 2025 — the inflation-adjusted 1980 high is estimated at over $200 per ounce.

Why is silver more volatile than gold?

Silver trades in a smaller market and depends more heavily on industrial demand. BlackRock reports that silver's annualized volatility has been as much as twice gold's over the past 20 years.

Can industrial demand make silver a better inflation hedge?

Industrial demand can support silver prices, but it also links the metal to manufacturing and economic growth. That can weaken performance during inflationary slowdowns.

Are TIPS a more direct inflation hedge than silver?

TIPS have a contractual link to CPI because their principal adjusts with inflation. Silver has no contractual CPI adjustment and is priced through market supply and demand.

Does physical silver have costs that reduce inflation protection?

Yes. Dealer premiums, bid-ask spreads, shipping, insurance, storage, and possible account fees can reduce the real return received from physical silver.

Can silver be held in an IRA?

Certain coins and qualifying bullion can be held under limited IRS exceptions. Qualifying bullion must remain in the physical possession of a bank or approved nonbank trustee.

Conclusion

Silver can respond to inflation, currency concerns, falling real rates, and investor demand — and it can also fall during inflation when interest rates rise, the dollar strengthens, industrial activity weakens, or speculative positions unwind. That record does not support calling silver a reliable inflation hedge. A more accurate description is that silver is a volatile monetary and industrial metal that may add inflation sensitivity and diversification in selected periods; it should be tested against costs, liquidity needs, and other inflation tools rather than treated as a stand-alone answer.

Sources

- Federal Reserve Bank of St. Louis. Consumer Price Index (CPIAUCSL).

- Barchart. How High Can Silver Prices Rise? (inflation-adjusted 1980 peak).

- iShares (BlackRock). Gold and Silver: Investing in Precious Metals.

- TreasuryDirect. Treasury Inflation-Protected Securities (TIPS).

- arXiv. N. N. Taleb, Bitcoin, Currencies, and Fragility.

- The Silver Institute. Industrial Demand Reached a Record 680.5 Moz in 2024 (industry body).

- Investor.gov (U.S. SEC). Diversify Your Investments.

- World Gold Council. The Relevance of Gold as a Strategic Asset (industry body).

- Internal Revenue Service. Investments in Collectibles in Individually Directed Qualified Plan Accounts.

Article reviewed and edited by Daniel M. — editor, 401kToGoldIRA.org. A balanced, evidence-based examination sourced to the Federal Reserve (FRED), Barchart, iShares/BlackRock, TreasuryDirect, arXiv, the Silver Institute, Investor.gov, and the World Gold Council (industry sources flagged); educational only, not financial, tax, or legal advice.