Educational only: This article summarizes BLS, SSA, TreasuryDirect, CMS, Investor.gov, and independent research in general terms. It is not financial, tax, or legal advice. The tables are mathematical illustrations, not forecasts. Customers should speak to a financial or tax advisor before making decisions. Goldco does not offer tax or legal advice. Past performance does not guarantee future results.

At a steady 3% inflation rate, an item costing $100 would cost about $134 after ten years and about $181 after twenty — the core reason a retirement plan needs to defend purchasing power, not just preserve a dollar balance.

Source: U.S. Bureau of Labor Statistics — Purchasing Power of the Consumer Dollar. Figures are compound arithmetic for illustration, not predictions.

Key takeaways

- The retirement risk is purchasing power, not the dollar balance — inflation quietly shrinks what a fixed income buys.

- Healthcare often rises faster than general prices, so a plan should test a separate, higher medical-cost assumption.

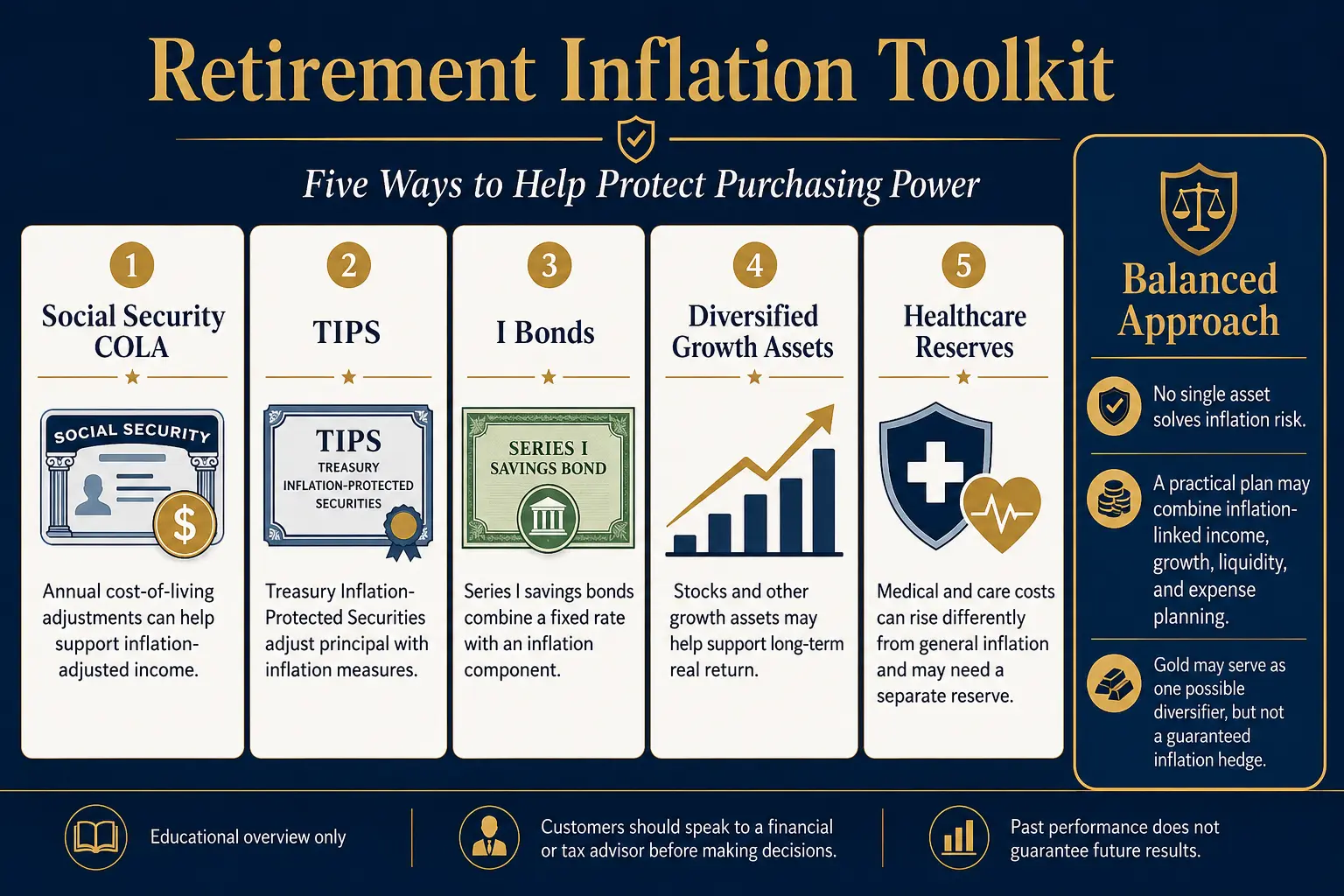

- Partial defenses exist: Social Security COLA (2.7% for 2026), TIPS whose principal adjusts with inflation, and diversified growth assets.

- A modest gold allocation is one optional diversifier — but its inflation link is weak and unstable per a 2024 CFA Institute analysis, so it is not a guaranteed hedge.

- Stress-test the plan at 2%, 3%, and 4% general inflation plus a separate healthcare rate rather than assuming a single number.

Social Security COLA can support part of household income; Treasury Inflation-Protected Securities (TIPS) and Series I savings bonds have direct links to inflation measures; diversified growth assets may support long-term real returns; and cash and short-term bonds support near-term spending. Tangible assets such as gold may play a limited role, but historical evidence does not show a stable inflation relationship in every period.

Quick Answer: Why Purchasing Power Matters More Than the Balance

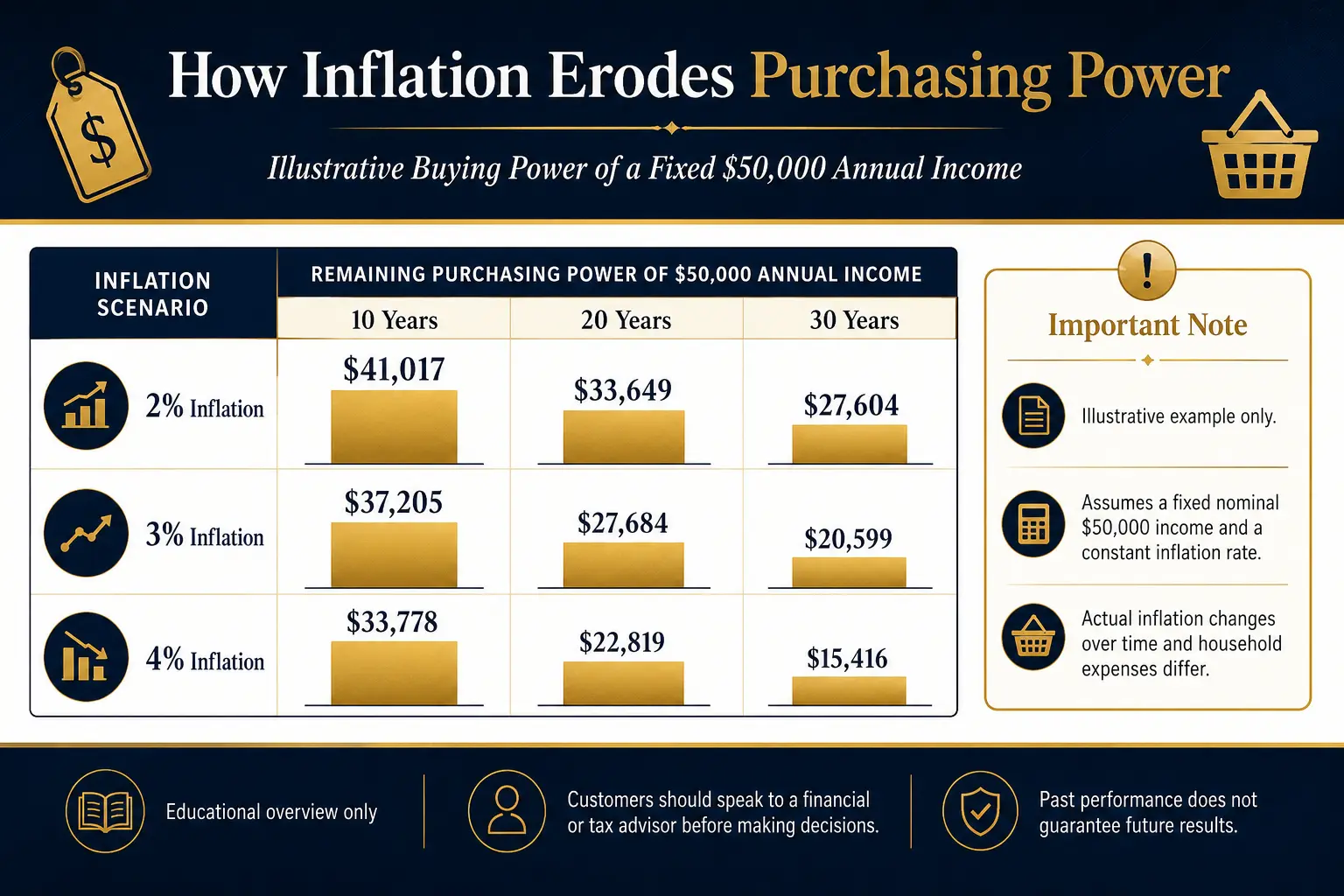

A retirement account can rise in nominal dollars while losing ground after inflation and taxes. Investor.gov defines real return as the return remaining after accounting for inflation and taxes. A fixed $50,000 annual income may still be $50,000 many years later, but its buying power can be much lower. The table below is a mathematical illustration, not an inflation forecast.

| Constant income | Inflation assumption | Buying power after 10 yr | after 20 yr | after 30 yr |

|---|---|---|---|---|

| $50,000 | 2% | ~$41,017 | ~$33,649 | ~$27,604 |

| $50,000 | 3% | ~$37,205 | ~$27,684 | ~$20,599 |

| $50,000 | 4% | ~$33,778 | ~$22,819 | ~$15,416 |

Assumes a fixed nominal income and constant inflation rate solely to show compounding. Actual inflation changes year to year and household spending differs. Reflects the BLS principle that purchasing power can be measured by comparing price levels over time.

A practical plan asks three questions: which income sources rise with inflation, which expenses may rise faster than the household's general cost of living, and which assets can support long-term real return without too much short-term risk. No single product answers all three. Customers should speak to a financial or tax advisor before making decisions involving retirement income, asset allocation, withdrawals, or taxes. Goldco does not offer tax or legal advice.

How Inflation Compounds Against a Fixed Income

Inflation is not only a one-year problem — each new price level becomes the starting point for the next year. At a steady 3% rate, an item costing $100 would cost about $134 after ten years and about $181 after twenty (illustrations based on compound arithmetic, not predictions). Purchasing-power erosion can affect retirement in several ways: a fixed pension buys less over time; cash reserves can lose real value when interest does not keep pace; fixed-rate bond payments remain unchanged even as living costs rise; withdrawals may need to increase; and taxes can reduce the real return available for spending. Investor.gov identifies inflation as a risk for fixed-rate investments and cash equivalents.

Personal inflation can differ from headline CPI

The CPI measures the average experience of a broad population — it does not measure the exact rate faced by every retiree. BLS states that its main indexes do not produce official estimates for specific groups such as Americans age 62 and older; it publishes a research index for older Americans, but with important limitations, and it is not an official index. A household that spends more than average on medical care, housing, insurance, or travel can experience a different rate of erosion than the national CPI suggests — one reason retirement planning benefits from category-level budgeting rather than one inflation assumption for every expense.

Social Security COLA and Inflation-Adjusted Income

Social Security includes an automatic cost-of-living adjustment. The SSA states that the COLA's purpose is to prevent Social Security and Supplemental Security Income benefits from being eroded by inflation, using the CPI for Urban Wage Earners and Clerical Workers (CPI-W) under a statutory third-quarter formula. The Social Security COLA for 2026 is 2.8% (that figure applies to 2026 benefits and should be updated in a later review). COLA is an important form of inflation-adjusted income, but it does not mean every retiree's full budget rises at the same rate — Social Security may cover only part of household spending, while pensions, annuities, rent, dividends, bond interest, and portfolio withdrawals follow different rules. A useful income map labels each source as fully linked to an inflation measure, partly adjustable, fixed in nominal dollars, market-dependent, or discretionary. This prevents a COLA on one income source from being mistaken for full retirement inflation protection.

TIPS and I Bonds: Direct Inflation-Linked Options

TIPS and Series I savings bonds are the most direct federal tools for linking principal or interest to inflation measures. TIPS are issued with 5, 10, and 30-year maturities; principal rises with inflation and falls with deflation, interest is paid every six months at a fixed rate applied to the adjusted principal, and at maturity the holder receives the inflation-adjusted principal or the original principal, whichever is greater. They can support purchasing power when maturities are matched to future spending years, but market values can rise or fall before maturity, selling early can produce a gain or loss, they protect against the referenced CPI rather than every personal expense, and federal tax can be due each year on interest and principal adjustments in a taxable account (TIPS are exempt from state and local income tax). I Bonds combine a fixed rate with an inflation rate that resets every six months, earn interest up to 30 years, can be redeemed after 12 months (with a three-month interest penalty before five years), and carry a $10,000 annual electronic purchase limit per taxpayer identifier — useful for gradual accumulation but often too limited to cover a large portfolio alone.

| Feature | TIPS | I Bonds |

|---|---|---|

| Marketability | Can be sold before maturity | Cannot be sold on a market |

| Inflation link | Principal adjusts with CPI | Composite rate includes an inflation component |

| Maturities | 5, 10, or 30 years | Earn interest up to 30 years |

| Early access | Sellable, but market price varies | Locked 12 months; interest penalty before 5 years |

| Purchase scale | Large auction/market capacity | $10,000 annual electronic limit per taxpayer ID |

| Tax timing | Annual federal tax on adjustments in taxable accounts | Federal tax generally deferrable to redemption/maturity |

Neither instrument removes every retirement risk — TIPS carry interest-rate and market-price risk before maturity, I Bonds have purchase and liquidity limits, and both are tied to broad inflation measures rather than a household's exact basket. Tax treatment and account placement can affect results. Customers should speak to a financial or tax advisor before using TIPS or I Bonds in a taxable account, IRA, or withdrawal plan. Goldco does not offer tax or legal advice.

Growth Assets and Diversification

Retirement inflation protection often requires some exposure to assets with long-term growth potential. Investor.gov explains that asset allocation divides a portfolio among categories such as stocks, bonds, and cash, with the appropriate mix depending on time horizon and risk tolerance, and notes that precious metals, real estate, and other assets can be included — each with its own risks. Stocks may support real growth because companies can raise prices and grow earnings, but prices can also fall sharply, including near the start of retirement. Bonds provide income and stability but face inflation risk. Cash supports spending but too much low-yield cash can lose purchasing power. Diversification does not ensure a profit or remove loss risk; its purpose is to avoid relying on one source of return. A balanced plan can use separate layers: near-term spending (cash, money-market, T-bills, short-term high-quality bonds), inflation-linked spending (COLA, TIPS, I Bonds), long-term growth (diversified stock exposure), and optional diversifiers (real estate, commodities, or tangible assets in a limited supporting role). Customers should speak to a financial or tax advisor before making allocation or retirement-income decisions. Goldco does not offer tax or legal advice.

Healthcare Inflation as a Distinct Retirement Pressure

Medical spending deserves a separate line in a retirement inflation plan. BLS divides the medical care CPI into medical care services (professional services, hospital and related services, health insurance) and medical care commodities — the index measures consumer prices and does not represent every dollar of national health spending. CMS projects that national health expenditures will grow by an average of 5.4% per year from 2025 through 2034, faster than projected GDP growth of 4.1%, with Medicare spending projected to grow 7.7% per year on average (spending-growth projections, not pure price-inflation forecasts, reflecting enrollment, use of care, and service mix). CMS also reports that per-person personal healthcare spending for people age 65 and older was $22,356 in 2020, more than twice the amount for working-age adults (a historical figure, not a current individual estimate). A practical plan separates Medicare premiums, supplemental coverage, prescription drugs, dental/vision/hearing, out-of-pocket cost sharing, long-term care, and a reserve. The retirement healthcare cost calculator can help organize assumptions as an educational planning tool.

Where Tangible Assets Like Gold May Fit

Gold is often described as a retirement inflation hedge. The historical evidence is mixed. A 2024 CFA Institute analysis found that monthly changes in gold prices were not meaningfully related to changes in inflation on average from 1979 through 2024, and that the relationship changed over time — some periods showing positive inflation sensitivity, others weak or negative. An academic study in Energy Economics found that gold's response depended on the inflation regime: in its U.S. data, gold responded more clearly when monthly inflation was unusually high, and less so during moderate or low inflation, which the authors cited as one reason the research literature reaches mixed conclusions. World Gold Council research argues that gold has offered stronger purchasing-power protection over long periods while acknowledging weaker short-term performance — but the World Gold Council represents the gold industry, so its conclusions should be considered alongside independent and academic evidence.

The combined evidence supports a cautious conclusion: gold may respond well during some inflation regimes, can fail to track inflation over shorter or moderate-inflation periods, is also affected by interest rates, the dollar, investor demand, and market conditions, produces no contractual income, and carries dealer spreads, custody, storage, and account fees that can reduce results. Gold may serve as one possible diversifier rather than the main purchasing-power strategy. The gold allocation backtest can help compare historical portfolio scenarios, while how much gold to own in retirement discusses allocation without presenting one percentage as suitable for everyone. Customers should speak to a financial or tax advisor before adding gold, changing an allocation, or using a Gold IRA. Goldco does not offer tax or legal advice.

A Practical Plan to Protect Retirement Purchasing Power

A purchasing-power plan can be built in nine steps:

- Measure spending in today's dollars. List essential and flexible expenses using current prices, keeping medical care, housing, food, transportation, insurance, taxes, and travel in separate categories.

- Classify income by inflation protection. Identify whether each source is CPI-linked, partly adjustable, fixed, or market-dependent — Social Security has a statutory COLA, but a private pension may have no adjustment or a capped one.

- Use more than one inflation assumption. Test general inflation at 2%, 3%, and 4%, plus a separate healthcare assumption (planning scenarios, not forecasts).

- Match near-term spending with liquid assets so money needed in the next several years does not depend on selling volatile assets in an unfavorable market.

- Consider an inflation-linked income layer — TIPS maturities or I Bond redemptions aligned with future spending, subject to liquidity, purchase, tax, and market limits.

- Keep a diversified growth layer. A retirement that may last decades can still require growth, balanced against short-term loss risk.

- Build a healthcare reserve, modeled separately from the general CPI assumption.

- Limit any tangible-asset role. Gold or other tangible assets can be tested as a minority diversifier, including dealer premium, spread, storage, fees, liquidity, and opportunity cost. The Gold IRA calculator and quiz can help organize assumptions and questions.

- Review the plan regularly. A yearly review can compare actual spending with the original assumptions and rebalance.

Frequently Asked Questions

What does retirement purchasing power mean?

Retirement purchasing power is the amount of goods and services that retirement income and savings can buy after considering inflation. As prices rise, a fixed dollar amount buys less.

Does Social Security keep up with inflation?

Social Security uses an annual COLA based on the CPI-W under a statutory formula. The adjustment helps preserve benefit purchasing power, but it may not match every retiree's personal spending pattern.

Are TIPS suitable for retirement inflation protection?

TIPS directly adjust principal for CPI changes and return at least the original principal at maturity. They can still fluctuate in market value before maturity and can create annual federal tax on principal adjustments in taxable accounts.

How do I Bonds address inflation?

I Bonds combine a fixed rate with an inflation rate that resets every six months. They have a one-year holding requirement, an early-redemption interest penalty before five years, and a $10,000 annual electronic purchase limit per taxpayer identifier.

Is gold a reliable inflation hedge?

Historical evidence is mixed. Some studies find stronger results during high-inflation periods or over long horizons, while other analyses find an unstable or weak average relationship. Gold should not be treated as a dependable one-asset solution.

How often should a retirement inflation plan be reviewed?

A yearly review is a practical general schedule, with additional reviews after major changes in income, spending, health, tax law, or retirement date. No universal review schedule fits every household.

Update Log

- 2026: Initial publication. Sourced to BLS (CPI, medical-care CPI, R-CPI-E), SSA (COLA, 2026 COLA 2.8%), TreasuryDirect (TIPS, I Bonds), CMS (National Health Expenditure), Investor.gov, and independent research on gold and inflation (CFA Institute, Energy Economics, World Gold Council). Figures such as the COLA change annually — reverify before relying on any figure.

Sources

- U.S. Bureau of Labor Statistics. Cpi.

- U.S. Bureau of Labor Statistics. Purchasing Power and Constant Dollars.

- U.S. Bureau of Labor Statistics. Questions and answers.

- U.S. Bureau of Labor Statistics. R cpi e home.

- U.S. Bureau of Labor Statistics. Medical care.

- Social Security Administration. Cola.

- Social Security Administration. LatestCOLA.

- U.S. TreasuryDirect. Tips.

- U.S. TreasuryDirect. I bonds.

- U.S. TreasuryDirect. Comparing tips to i.

- Investor.gov (SEC). Purchasing power.

- Investor.gov (SEC). What Is Risk?.

- Investor.gov (SEC). Asset Allocation Basics.

- Investor.gov (SEC). Beginner's Guide to Asset Allocation.

- Centers for Medicare & Medicaid Services. Nhe fact sheet.

- CFA Institute. Gold and inflation an unstable relationship.

- World Gold Council. Beyond cpi gold as a strategic inflation hedge.

Article reviewed and edited by Daniel M. — editor, 401kToGoldIRA.org. Sourced to BLS, SSA, TreasuryDirect, CMS, Investor.gov, and independent research; educational only, not tax or legal advice.

Further Reading

Gold Allocation BacktestHow 0-25% gold historically affected a 60/40 portfolio — sourced.

Gold Allocation BacktestHow 0-25% gold historically affected a 60/40 portfolio — sourced. How Much Gold Should Investors Own in Retirement?A framework for matching allocation to goals, liquidity, and risk.Inflation & Purchasing-Power CalculatorTest how a fixed dollar amount and a fixed income lose real value at an assumed inflation rate.

How Much Gold Should Investors Own in Retirement?A framework for matching allocation to goals, liquidity, and risk.Inflation & Purchasing-Power CalculatorTest how a fixed dollar amount and a fixed income lose real value at an assumed inflation rate.