Educational only: This article discusses retirement behavior and planning in general terms and is not financial, tax, or legal advice. Every household's situation differs. Customers should speak to a financial or tax advisor before making decisions. Goldco does not offer tax or legal advice. Past performance does not guarantee future results.

Research from the Center for Retirement Research at Boston College found that about half of surveyed retirees felt discomfort when imagining their portfolio balance falling — a reluctance to spend that persists even when a sound plan supports the spending.

Source: Center for Retirement Research at Boston College. Underspending is a real and common behavior, not a personal failing.

Key takeaways

- The guilt comes from an identity shift — decades of "saving is responsible" do not switch off just because a paycheck stops.

- The "retirement consumption puzzle" shows many retirees draw down savings far more slowly than plans assume, sometimes from fear rather than affordability.

- Loss aversion, longevity fear, and market fear all make spending principal feel unsafe even when a projection supports it.

- A structured withdrawal framework (a safe starting rate + guardrails) turns a frightening balance into a defined "paycheck" that feels permitted to spend.

- Underspending is itself a risk — sacrificing health, travel, or family time a plan could support is a genuine cost, not automatically the safer choice.

What Is Retirement Spending Guilt?

Retirement spending guilt is the discomfort or anxiety a person feels when spending the retirement savings they worked for decades to build — even when the money is there and a plan supports the spending. It is not the same as running short of money. It is a behavioral and emotional response: the balance that once felt like security now feels like something that should be protected rather than used. The Center for Retirement Research at Boston College found that about half of surveyed retirees felt discomfort when imagining their portfolio balance falling, a reluctance to draw down savings that can persist even when a projection shows the spending is sustainable (Center for Retirement Research at Boston College). Recognizing the guilt as a common, well-documented pattern — not a personal flaw — is the first step toward planning around it.

Why Do Lifelong Savers Struggle to Spend?

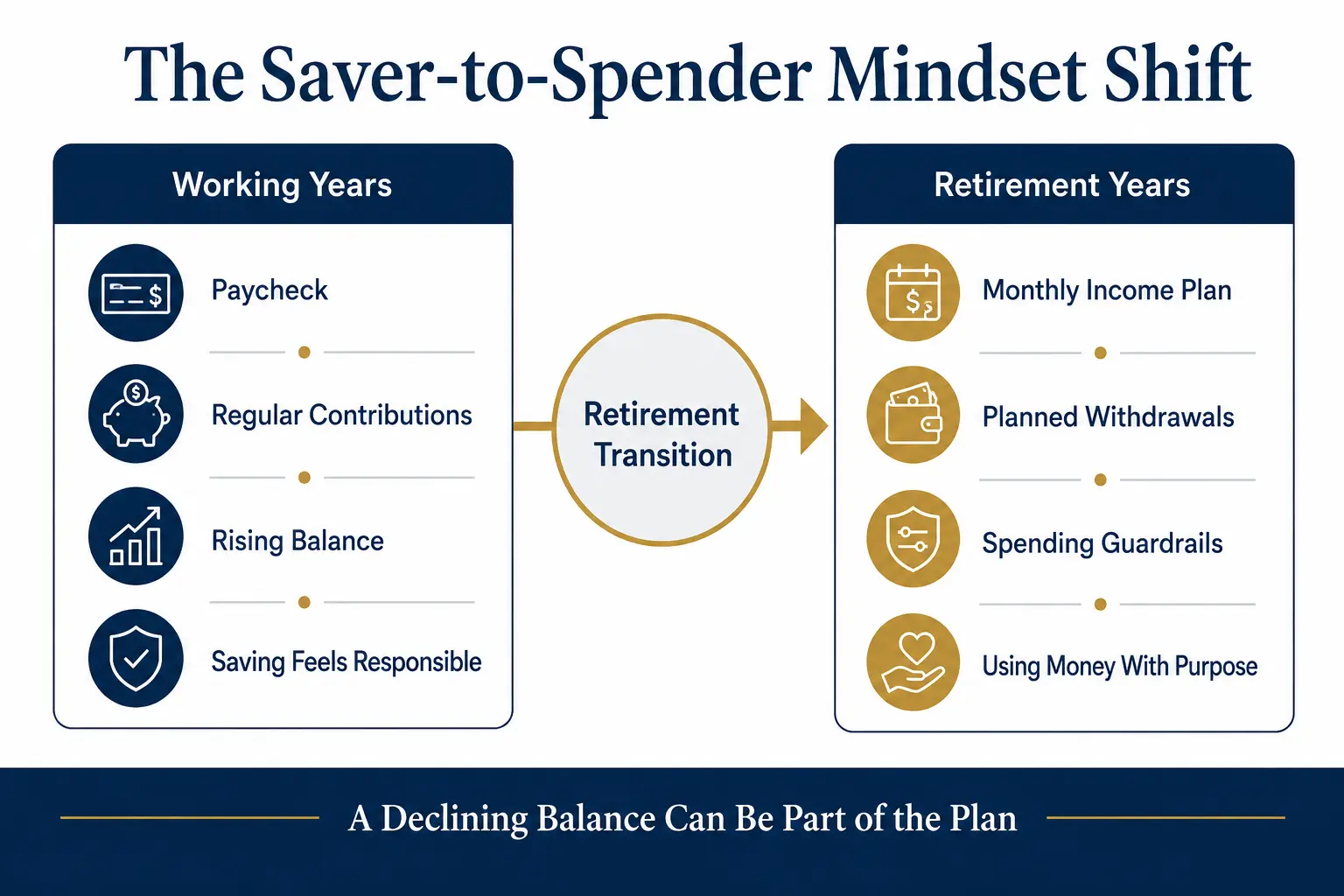

The core reason is that retirement reverses a habit built over a working lifetime. For thirty or forty years, the responsible act was to save: contribute to the plan, watch the balance rise, resist spending. Retirement asks for the opposite — to draw the balance down on purpose — and the mind does not switch that instinct off just because the paychecks stopped. The saver-to-spender transition is a genuine identity shift, and a large, hard-won balance can feel like an achievement to preserve rather than a resource to use. Several forces reinforce that reluctance, and they are worth naming individually, because a plan can address each one.

Do Retirees Really Underspend?

The evidence suggests many do. Economists describe a "retirement consumption puzzle" — the finding that spending often falls at retirement and that many retirees draw down their assets far more slowly than standard models predict. National Bureau of Economic Research working papers have examined this pattern, exploring how spending changes at and through retirement rather than following a smooth drawdown (National Bureau of Economic Research; National Bureau of Economic Research). The important distinction is why spending falls, because the causes are not all the same:

- Some spending falls because needs genuinely change — health, mobility, work costs, or household size shift over time.

- Some spending falls because a retiree chooses a simpler life and is content with it.

- Some spending falls because fear blocks purchases that a sound plan could comfortably support.

Only the third category is a problem to solve. A retiree who spends less because they prefer to is doing nothing wrong. A retiree who skips travel, delays a needed home repair, or hesitates over a small comfort — while a projection shows the money is there — is paying an invisible cost. Fidelity has described this "spending guilt" as a common obstacle in retirement, where a psychologically difficult shift keeps people from using money they can afford to use (Fidelity).

What Psychological Forces Drive Retirement Spending Guilt?

How does the saver-to-spender mindset shift create discomfort? The habit of saving becomes part of a person's identity. When the rule "spending is irresponsible" runs for decades, reversing it in retirement feels like breaking a personal value, not following a plan. How does loss aversion affect retirement spending? Behavioral research has long found that people feel the pain of a loss more sharply than the pleasure of an equal gain, so watching a balance decline — even by a planned amount — can feel worse than the enjoyment the spending buys. How do longevity fear and health uncertainty affect spending? Not knowing how long retirement will last, or what future medical and long-term-care costs may be, makes almost any withdrawal feel risky; the balance is a buffer against an unknown, and spending it feels like lowering a defense. Why does market fear make spending feel unsafe? A retiree who no longer earns a paycheck knows a market decline cannot be replaced by future contributions, so the fear of drawing down during a downturn — sequence-of-returns risk — adds another layer of caution. These forces are rational responses to real uncertainty; the goal is not to dismiss them but to build a plan that answers them.

How Can a Retirement Withdrawal Strategy Reduce the Guilt?

The single most effective antidote to spending guilt is a written withdrawal framework, because it converts a large, frightening balance into a defined amount that is designed to be spent. When a retiree knows a specific figure is the plan's paycheck, spending within it feels permitted rather than reckless. A common starting point is a safe withdrawal rate applied to the starting portfolio, adjusted over time — the 4% rule is the best-known version, though its critics and dynamic alternatives matter (the 4% Rule guide reviews how the rule is commonly discussed and its limits). More flexible approaches use spending guardrails: a spending floor for essentials, a planned level for normal years, and a flexible ceiling that can rise after strong markets or ease after weak ones, reviewed annually. Because the guardrails respond to how the portfolio actually performs, the retiree can spend confidently in good years and adjust in poor ones — without treating every market wobble as a reason to freeze. The broader mechanics of making a portfolio last are covered in the retirement portfolio longevity guide. Vanguard describes structured spending strategies as a way to turn savings into a sustainable, repeatable retirement income rather than an anxious guessing game (Vanguard). Customers should speak to a financial or tax advisor before making decisions about withdrawal rates or allocation. Goldco does not offer tax or legal advice.

How Does Lifetime Income Change the Feeling of Spending?

Guilt eases most when a retiree knows their essential costs are covered no matter what. Lifetime-income sources — Social Security and pensions, and for some households an annuity — pay a stream that does not depend on drawing down a portfolio, which makes the rest of the plan feel safer to spend. When housing, food, health care, and insurance are funded by predictable income, the remaining savings can be treated as flexible money for travel, family, and comfort, rather than as an emergency buffer that must never shrink. Annuities are one option some retirees use to create that income floor, but they carry their own considerations — FINRA notes that annuities differ widely in costs, features, surrender terms, and tax treatment, and that the insurer's obligations depend on its financial strength and claims-paying ability (FINRA). The point is not that any one product is right, but that matching guaranteed income to essential expenses is one of the most reliable ways to make spending feel permitted. Broader inflation and cash-flow planning is covered in the protect retirement purchasing power guide, and liquidity questions in the need cash from retirement assets guide.

Can Underspending Itself Be a Mistake?

It can. The instinct to protect the balance treats spending as the only risk, but underspending has real costs of its own. A retiree who skips the trip while still healthy, delays a home modification that would improve safety, or forgoes time with family to preserve a number may reach later years with a large unspent balance and a smaller life than the money could have funded. Health, energy, and relationships are not evenly available across a long retirement — some experiences are only possible earlier. Required minimum distributions also eventually force some drawdown from traditional retirement accounts: the IRS requires distributions to begin at the applicable age (73 for those born 1951–1959, 75 for those born 1960 or later), so a portion of the balance must be withdrawn on a schedule whether or not it is spent (Internal Revenue Service). None of this argues for careless overspending — a plan still has to last. It argues that the goal is a balanced drawdown that funds a good life without running short, and that "spend as little as possible" is not automatically the responsible choice. The allocation guide and the suitability quiz can help organize the broader plan.

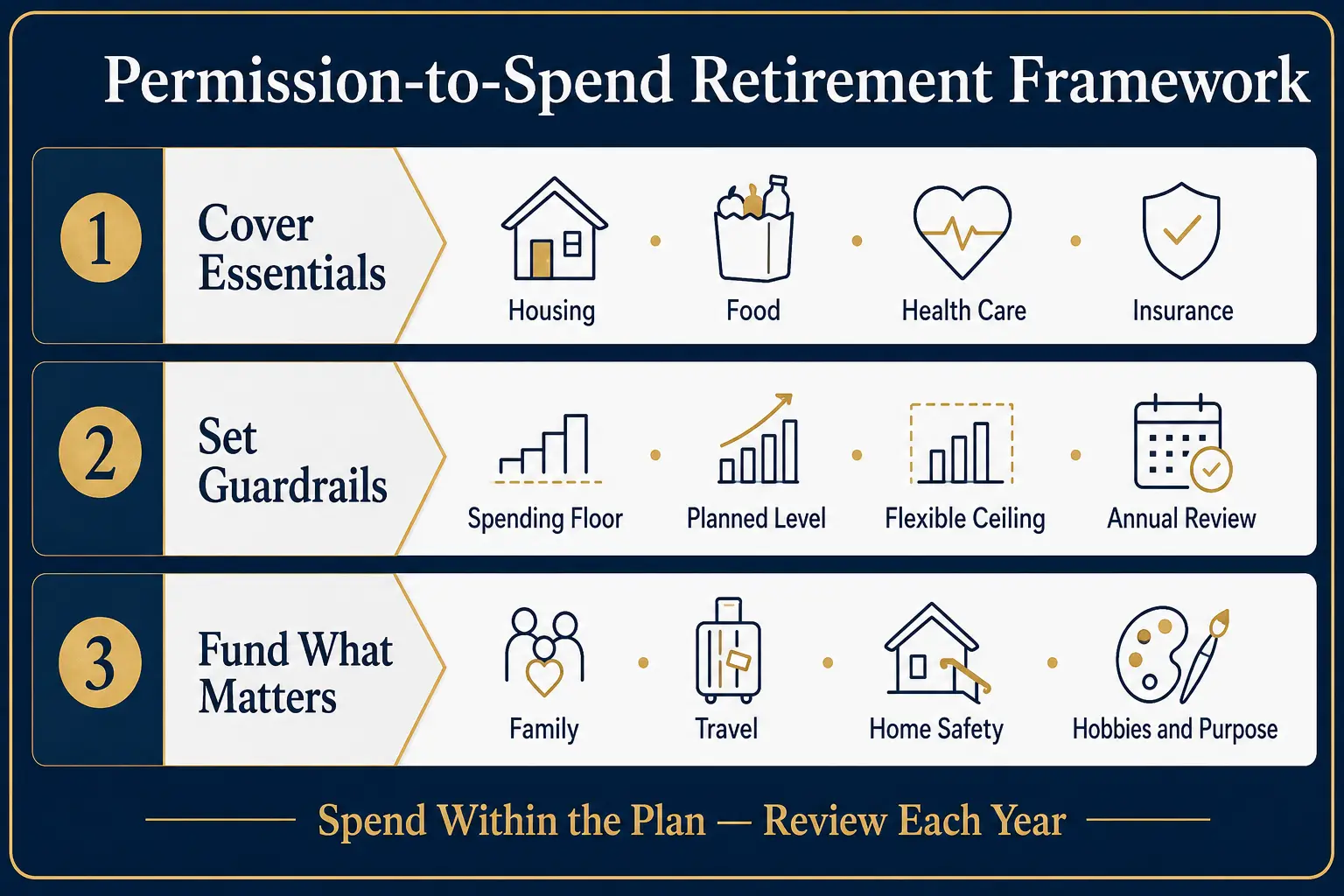

A Practical Permission-to-Spend Plan

Turning the psychology into action follows a simple sequence. First, cover essentials with reliable income. Map housing, food, health care, and insurance to Social Security, pensions, and any lifetime-income source, so core needs do not depend on market swings. Second, set guardrails on the flexible money. Define a spending floor, a planned level, and a flexible ceiling from the remaining portfolio, and agree in advance how each adjusts after strong or weak years. Third, fund what matters. With essentials covered and guardrails in place, spending on family, travel, home safety, and purpose is not a guilty indulgence — it is the plan working as intended. Then review each year. An annual check-in on the balance, the withdrawal rate, health, and goals lets the plan flex without a permanent commitment. The most useful mindset shift is to stop treating a declining balance as failure. A balance that draws down on a plan, funding a good retirement while lasting the horizon, is exactly what the saving was for. Customers should speak to a financial or tax advisor before making decisions about spending, withdrawals, or allocation. Goldco does not offer tax or legal advice.

Frequently Asked Questions

What is retirement spending guilt?

Retirement spending guilt is the discomfort or anxiety many lifelong savers feel when spending the money they worked decades to accumulate, even when a sound plan shows the spending is affordable. It often leads to underspending and a lower quality of life than the money allows.

Do retirees really underspend?

Research on the "retirement consumption puzzle" finds that many retirees draw down savings far more slowly than plans assume, and surveys show a large share feel discomfort watching their balance fall. Some reduced spending reflects genuine changes, but some reflects fear rather than affordability.

How can a withdrawal strategy reduce spending guilt?

A structured withdrawal framework — such as a safe starting rate with dynamic guardrails — converts a large, frightening balance into a defined "paycheck." Spending within the plan feels permitted rather than reckless, which reduces the anxiety of drawing down principal.

Does guaranteed lifetime income help with spending guilt?

Lifetime-income sources that cover essential costs — Social Security, pensions, and some annuity products — can make spending feel safer, because core expenses are covered no matter how markets or longevity play out. FINRA notes annuities carry their own costs, features, and issuer-strength considerations to weigh.

Can underspending itself be a mistake?

Yes. Sacrificing travel, family time, health, or comfort a plan could support is a real cost. Underspending can leave a retiree with a lower quality of life and a large unspent balance, which is not automatically a better outcome than a planned, sustainable drawdown.

Conclusion

Retirement spending guilt is a common, well-documented response to a genuine identity shift — the move from a lifetime of saving to the unfamiliar task of drawing savings down. It is driven by loss aversion, longevity fear, and market fear, and it can quietly cost a retiree the very experiences their savings were meant to fund. The answer is not willpower but structure: cover essentials with reliable income, set spending guardrails on the flexible money, fund what matters, and review each year. A declining balance, drawn down on a plan, is not a failure — it is the plan working.

Sources

- Center for Retirement Research at Boston College. Half of Retirees Afraid to Use Their Savings.

- National Bureau of Economic Research. Working paper on retirement consumption.

- National Bureau of Economic Research. Working paper on the retirement-consumption puzzle.

- Fidelity. Overcoming retirement spending guilt.

- Vanguard. Spending strategies in retirement.

- FINRA. Annuities.

- Internal Revenue Service. Retirement Topics — Required Minimum Distributions.

Article reviewed and edited by Daniel M. — editor, 401kToGoldIRA.org. A behavioral-finance overview sourced to the Center for Retirement Research at Boston College, the National Bureau of Economic Research, Fidelity, Vanguard, FINRA, and the IRS; educational only, not financial, tax, or legal advice.