Educational only: This guide summarizes IRS, SSA, and CFPB guidance in general terms and is not financial, tax, or legal advice. Contribution limits and figures should be confirmed against current IRS and SSA guidance for the specific year. Customers should speak to a financial or tax advisor before making decisions. Goldco does not offer tax or legal advice. Past performance does not guarantee future results.

Quick Answer: What to Do When Retirement Savings Are Behind

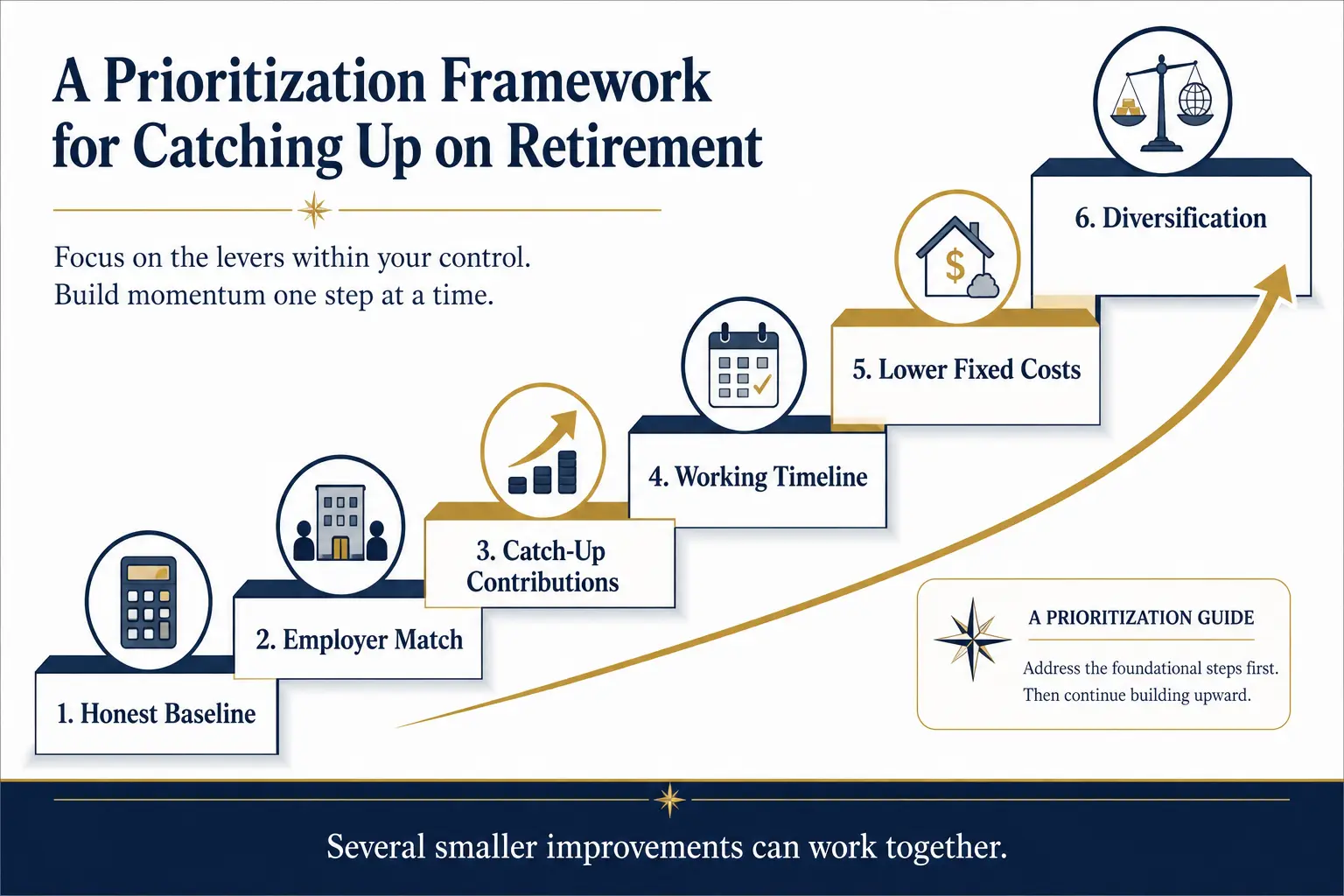

A late start retirement plan works better when the most powerful steps come first:

- Build an honest baseline. Add retirement accounts, taxable savings, pensions, and a current Social Security estimate, then estimate annual retirement spending and the income gap that savings must cover.

- Capture the full employer match. An available match is part of compensation and should usually be reviewed before lower-priority savings goals.

- Use retirement catch-up contributions. In 2026, most workers age 50 or older can contribute more to workplace plans, and workers ages 60 through 63 may qualify for the higher SECURE 2.0 catch-up limit. IRA savers age 50 or older also receive a higher limit (Internal Revenue Service).

- Review the retirement date. Working one to three more years can create more contribution years, more time for savings to grow, fewer years of withdrawals, and a higher Social Security benefit when claiming is delayed past full retirement age (Fidelity; Social Security Administration).

- Lower fixed costs. Housing, vehicles, insurance, debt payments, subscriptions, and recurring support obligations can have more impact than small spending cuts.

- Use an HSA when eligible. HSA contributions and qualified medical withdrawals receive federal tax advantages, and unused balances can carry forward (Internal Revenue Service).

- Diversify rather than search for one rescue asset. Stocks, bonds, cash reserves, and other assets each have different roles. Precious metals may be one limited diversification tool, but they are not a complete retirement plan.

Customers should speak to a financial or tax advisor before making decisions involving contribution limits, IRA eligibility, tax deductions, Roth treatment, rollovers, or asset allocation. Goldco does not offer tax or legal advice.

Not Enough Saved for Retirement: Start With an Honest Number

The first goal is not to compare a balance with a frightening headline. The goal is to measure the retirement gap. A practical inventory includes workplace plans, traditional and Roth IRAs, taxable investments, cash reserves, pensions, expected Social Security, home equity, debt balances, and any part-time income expected in retirement. A personal Social Security account can provide benefit estimates at different claiming ages (Social Security Administration).

Next, the plan needs a spending estimate. Current take-home spending is a better starting point than salary because payroll taxes, retirement contributions, commuting, and some work costs may change after retirement. Housing, health care, food, transportation, insurance, taxes, travel, family support, and home repairs should be separated into essential and flexible categories. The annual retirement gap is simple: expected annual spending, minus recurring pension and Social Security income, equals the annual amount that savings must support. For example, planned spending of $60,000 and recurring pension and Social Security income of $32,000 create a $28,000 annual gap. If fixed-cost changes reduce spending by $6,000, the gap falls to $22,000 — a 21.4% reduction in the amount savings must support. That arithmetic does not depend on market returns.

Use Savings-by-Age Benchmarks as Reference Points, Not Grades

Fidelity publishes guideposts of 1 times salary by age 30, 3 times by 40, 6 times by 50, 8 times by 60, and 10 times by 67. Fidelity describes the milestones as aspirational and bases them on assumptions that include saving 15% of income from age 25, maintaining substantial stock exposure, and retiring at 67 (Fidelity). Those figures can help with retirement savings by age comparisons, but they do not fit every household. A saver with a pension may need less personal savings than a saver without one. A household with a paid-off home and low spending may need less than a household with a large mortgage. A retirement that starts at 70 also has a different funding period from one that starts at 62.

The useful question is not whether a benchmark was missed. It is how much the current plan can improve through higher savings, lower spending, a later retirement date, and more efficient use of tax-advantaged accounts. The site's Gold IRA Calculator can support scenario testing, but any calculator output depends on assumptions about returns, inflation, fees, taxes, and retirement length.

Maximize Catch-Up Contributions Under the 2026 Rules

Retirement catch-up contributions are one of the clearest legal tools for saving for retirement in the 50s and early 60s. For 2026, the employee contribution limit for most 401(k), 403(b), governmental 457, and Thrift Savings Plan accounts is $24,500. The standard catch-up limit for participants age 50 or older is $8,000, allowing total employee contributions of up to $32,500 in most covered plans (Internal Revenue Service).

SECURE 2.0 provides a higher catch-up for workers who are ages 60, 61, 62, or 63 by the end of the year. For 2026, that higher catch-up remains $11,250. Combined with the $24,500 regular limit, the total can reach $35,750 in an eligible plan. For IRAs, the 2026 contribution limit is $7,500. The age-50 catch-up is $1,100, producing a combined limit of $8,600. Traditional IRA deductibility and Roth IRA eligibility can depend on income, filing status, and workplace-plan coverage (Internal Revenue Service; Internal Revenue Service).

A Sensible Contribution Order

A common priority order is: (1) contribute enough to receive the full workplace match; (2) build or preserve an emergency reserve so a repair or medical bill does not force retirement-account withdrawals; (3) increase workplace contributions toward the age-based limit; (4) use an IRA when eligible and appropriate; (5) use an HSA when eligible and health-plan terms fit the household; (6) add taxable savings after tax-advantaged options are reviewed. The correct order can differ when high-interest debt, unstable income, near-term expenses, or limited cash reserves are present — a catch-up strategy that creates new credit-card debt can weaken the overall plan. Automatic increases can make the process easier: a saver might raise the contribution rate by 1 percentage point now, direct part of each raise or bonus to retirement, and repeat the increase every six months until cash flow becomes tight.

Customers should speak to a financial or tax advisor before making decisions involving retirement catch-up contributions, IRA deductions, Roth contributions, rollovers, or the SECURE 2.0 catch-up rules. Goldco does not offer tax or legal advice.

Rethink the Timeline: Working Longer, Phased Retirement, and Delaying Social Security

Working longer retirement plans are not available to every person — health, caregiving duties, layoffs, and physically demanding work can limit the choice. When continued work is realistic, even a modest extension can affect several parts of the plan at once. Fidelity notes that delaying retirement gives savings more time to grow, reduces the number of retirement years that savings must fund, and can raise Social Security income; its planning examples show that later retirement can reduce the savings multiple needed under the firm's assumptions (Fidelity). A phased retirement can mean reduced hours, project work, consulting, seasonal work, or a lower-stress role — availability depends on the employer and occupation. Even when earnings are lower than full-time pay, they may cover current expenses and allow retirement accounts to remain invested longer.

Delaying Social Security. Social Security retirement benefits rise for each month claiming is delayed beyond full retirement age. For people born in 1943 or later, delayed retirement credits equal 8% per year, or two-thirds of 1% per month, and the increase stops at age 70 (Social Security Administration). The decision is personal — health, life expectancy, marital status, survivor needs, current cash flow, taxes, and the ability to keep working all matter, and delaying is not automatically the right choice for every household. Someone who claims before full retirement age and continues working may be affected by the earnings test: for 2026, the general earnings limit is $24,480 for someone under full retirement age all year, while a separate $65,160 limit applies in the year full retirement age is reached before the birthday month. Earnings no longer reduce benefits beginning with the month full retirement age is reached (Social Security Administration). Medicare timing must be reviewed separately, because late enrollment at age 65 can delay coverage or increase costs in some situations (Social Security Administration).

Cut Fixed Costs and Consider Downsizing

Large recurring expenses usually matter more than small one-time cuts. A fixed-cost review can cover mortgage or rent, property taxes, home insurance, utilities, vehicle payments, auto insurance, debt payments, subscriptions, storage units, and recurring family support. The goal is not to remove every enjoyable expense — it is to find changes that improve monthly cash flow for years. The Consumer Financial Protection Bureau notes that balancing debt, retirement income, and assets becomes more important with age, and its retirement resources highlight home equity, mortgage obligations, and housing choices as part of retirement planning (Consumer Financial Protection Bureau).

Downsizing may release home equity and reduce maintenance, utilities, insurance, and property taxes, but it can also create moving costs, transaction costs, repairs, higher homeowners-association fees, or a less convenient location — a useful comparison looks at the five- or ten-year cost of staying versus moving rather than focusing only on the sale price. Other practical changes can include paying off a vehicle and keeping it longer, refinancing or restructuring debt only when the total cost improves, moving closer to health care or family support, or renting part of a home where local rules and household needs permit. Every permanent $500 monthly reduction lowers annual spending by $6,000; if that amount is redirected to savings before retirement, it works twice: current contributions rise and the future spending target falls.

Use Every Suitable Tax-Advantaged Account, Including an HSA

A Health Savings Account can serve as both a current medical account and a long-term health-cost reserve when the saver is eligible. IRS Publication 969 states that eligible HSA contributions can be deductible, employer contributions can be excluded from income, and distributions used for qualified medical expenses are not taxed; unused balances generally carry over, and earnings are not included in income while held in the account (Internal Revenue Service). An HSA is not available to every household — eligibility generally requires qualifying high-deductible health-plan coverage and no disqualifying coverage, and HSA contributions stop once Medicare enrollment begins, including periods of retroactive Medicare coverage.

For nonmedical distributions, the IRS generally applies income tax and an additional 20% tax. The additional 20% tax no longer applies after age 65, disability, or death, although a nonmedical distribution can still be taxable income; qualified medical distributions remain tax-free when the rules are met (Internal Revenue Service). That structure can make HSA retirement savings useful for a late starter who is eligible and can pay some current medical costs from other cash. The choice still depends on plan deductibles, expected health needs, emergency reserves, and the investment options and fees inside the HSA. Customers should speak to a financial or tax advisor before making decisions involving HSA eligibility, Medicare enrollment, tax deductions, reimbursements, or retirement-account coordination. Goldco does not offer tax or legal advice.

Diversification for a Shorter Runway

A shorter savings runway does not make concentration safer. It usually makes large mistakes harder to recover from. A late starter may need growth, but that does not mean placing the entire account in the most aggressive asset available — a diversified mix can include stock funds for growth, bonds for income and stability, cash for near-term needs, and other assets with different return patterns. The exact mix depends on the retirement date, spending needs, pension income, risk capacity, and ability to continue working.

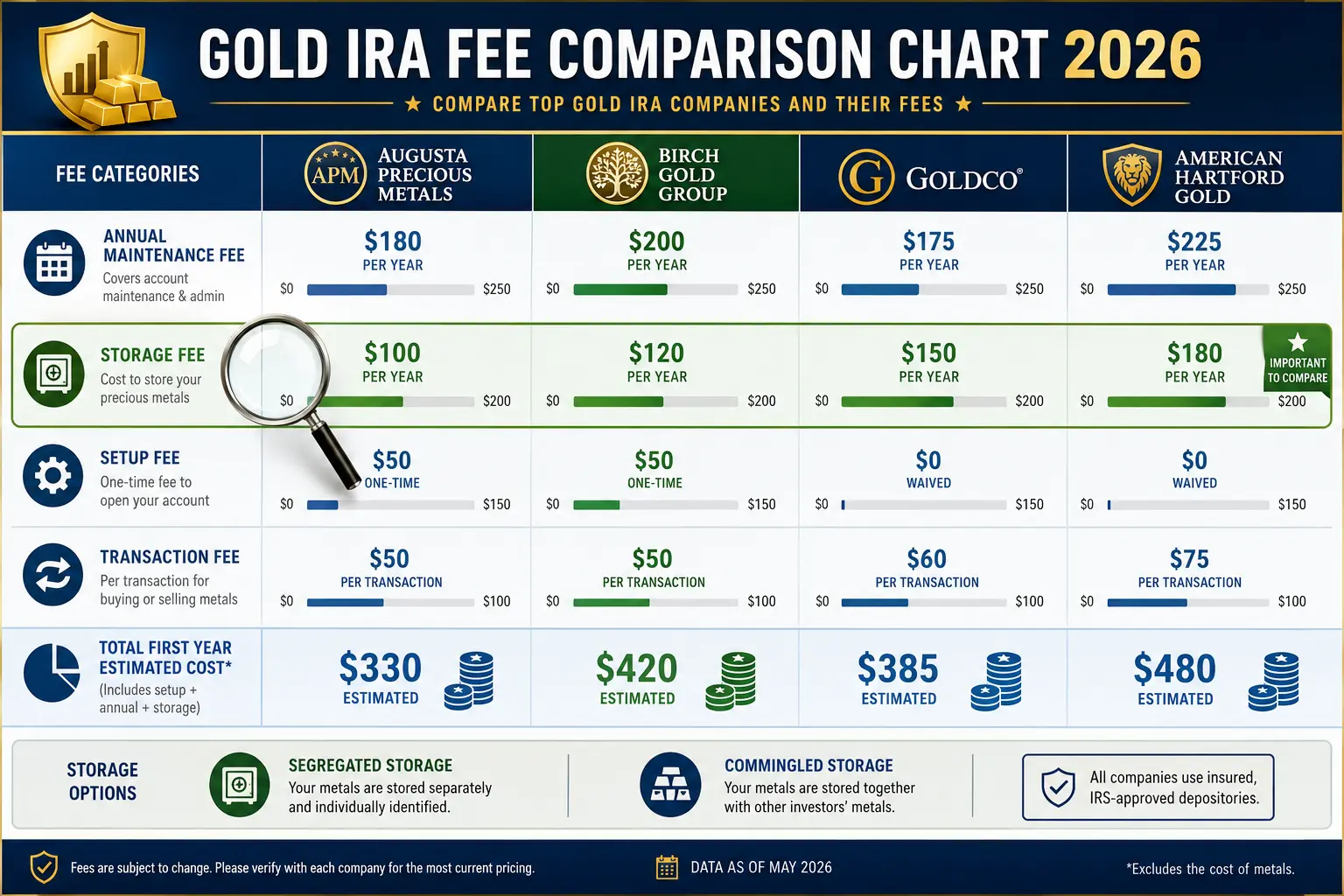

Precious metals can be discussed as one optional diversifier. The World Gold Council's 2026 strategic-asset report states that gold may improve diversification and liquidity in a broad portfolio. The World Gold Council represents the gold industry, so its research should be weighed with independent analysis and the fact that gold prices can rise or fall (World Gold Council). No verified source establishes one optimal precious-metals percentage for every late starter, and a modest allocation that complements stocks, bonds, and cash is different from treating gold as the sole repair for a retirement gap. The article How Much Gold Should Someone Own in Retirement? explains allocation questions without presenting a universal percentage. Retirement Planning at 55 and Precious Metals discusses the shorter runway faced by savers in their mid-50s. Gold IRA Strategy After Age 73 covers later-life distribution issues, while The 4% Rule and Gold IRAs reviews withdrawal assumptions and their limits. The Gold IRA Suitability Quiz can organize research questions but does not determine suitability. Past performance does not guarantee future results. Customers should speak to a financial or tax advisor before making decisions involving diversification, precious metals, an IRA rollover, or an allocation change. Goldco does not offer tax or legal advice.

A Realistic Catch-Up Example

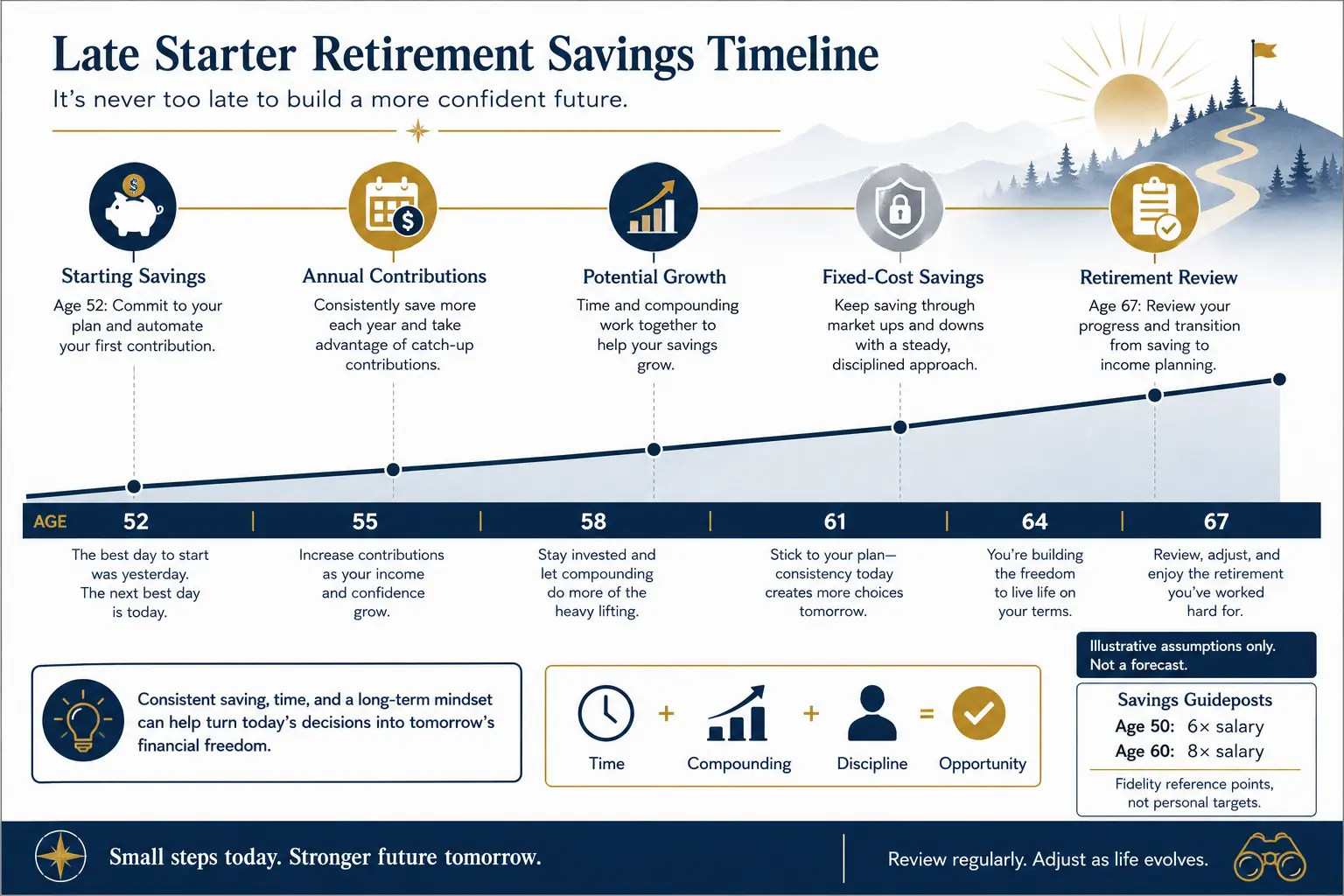

The following example is illustrative, not a forecast. A 52-year-old saver has $150,000 in retirement accounts and contributes $30,000 at the end of each year until age 67. The contribution is below the 2026 maximum available to many workers age 50 or older, but future legal limits and personal eligibility can change (Internal Revenue Service). Assumptions: starting balance $150,000; annual contribution $30,000; time 15 years; annual return assumption 5% before fees, taxes, and inflation; contributions at year-end; no withdrawals.

At a 0% return, the saver would finish with $600,000: the $150,000 starting balance plus $450,000 of contributions. At the 5% assumption, the projected balance is about $959,196 — roughly $359,196 above the no-growth total, though actual markets will not deliver a smooth return, and fees, taxes, inflation, and market declines can reduce the result. If the same contribution pattern continued for 18 years to age 70, the 5% illustration rises to about $1,204,964; the extra three years add contributions and compounding, while the later retirement date may also increase Social Security benefits through age 70 (Social Security Administration). If a fixed-cost review freed another $800 per month and all $9,600 per year was added to retirement savings, the 15-year 5% illustration rises to about $1,166,350 — a difference of about $207,154 compared with contributing $30,000 per year. The example shows why a retirement gap is rarely solved by one dramatic move: the larger effect can come from combining a higher savings rate, lower fixed costs, a longer timeline, and a diversified portfolio.

A Prioritized 90-Day Catch-Up Plan

Days 1–30: Measure. Collect all retirement, pension, debt, and HSA statements; obtain current Social Security estimates at several claiming ages; calculate current annual spending and the expected retirement gap; list every recurring cost that could change within two years.

Days 31–60: Improve cash flow. Capture the full employer match; increase workplace contributions by a manageable amount; review debt rates, insurance, vehicles, housing, and subscriptions; decide whether downsizing or phased retirement deserves a full cost comparison.

Days 61–90: Build the long-term structure. Set a target contribution path toward the 2026 catch-up limits; review IRA and HSA eligibility; compare retirement dates and Social Security claiming ages; review the portfolio for concentration, fees, liquidity, and near-term cash needs; document the plan and schedule a review every six months. A late starter does not need a perfect plan in one weekend — a written sequence of manageable decisions is more useful than a large target with no operating steps.

Frequently Asked Questions

Is it too late to save for retirement at 50?

No. A saver at 50 may still have 15 to 20 years before a traditional retirement date. Catch-up contributions, lower fixed costs, employer matching, a later retirement date, and delayed Social Security can materially improve the plan. The final result still depends on income, existing savings, health, spending, and market outcomes.

How much should someone have saved by age 50?

Fidelity uses 6 times salary at age 50 as an aspirational guidepost under specific assumptions, including saving 15% from age 25 and retiring at 67. It is not a universal requirement and may be too high or too low for a particular household.

What are the 2026 retirement catch-up contribution limits?

For most covered workplace plans, the 2026 employee limit is $24,500, plus an $8,000 catch-up for age 50 or older. Ages 60 through 63 may qualify for an $11,250 catch-up instead. The IRA limit is $7,500, plus a $1,100 age-50 catch-up.

Does delaying Social Security always make sense?

No. Benefits increase after full retirement age and stop increasing at age 70, but health, household cash flow, marital status, survivor needs, and expected longevity affect the decision.

Can an HSA help with retirement savings?

An eligible HSA can hold unused funds from year to year, and qualified medical withdrawals can be tax-free. Nonmedical withdrawals after age 65 avoid the additional 20% tax but can still be taxable income.

Can precious metals fix a retirement savings shortfall?

No single asset can repair every retirement gap. Precious metals may serve as one modest diversification tool, but contributions, spending, timeline, Social Security, taxes, and the broader portfolio usually have larger planning roles.

Conclusion

Feeling behind on retirement savings is a reason to organize the plan, not abandon it. The most useful order is straightforward: calculate the gap, capture the employer match, use catch-up contributions, review the retirement date, lower fixed costs, use suitable tax-advantaged accounts, and maintain diversification. Precious metals can be considered in proportion, alongside stocks, bonds, cash, and other assets, rather than as the entire solution. Late starters may not reproduce the result of someone who saved from age 25, but they can still improve retirement income, reduce the amount the portfolio must support, and create a more workable path through a series of legal and measurable changes.

Sources

- Internal Revenue Service. 401(k) limit increases to $24,500 for 2026; IRA limit increases to $7,500.

- Internal Revenue Service. IRA Deduction Limits.

- Internal Revenue Service. Publication 969 (Health Savings Accounts).

- Social Security Administration. Delayed Retirement Credits.

- Social Security Administration. Working While Receiving Benefits (Earnings Test).

- Social Security Administration. my Social Security Account.

- Social Security Administration. Plan for Retirement.

- Fidelity. How much do I need to retire?.

- Consumer Financial Protection Bureau. Planning for Retirement.

- World Gold Council. The Relevance of Gold as a Strategic Asset (2026).

Article reviewed and edited by Daniel M. — editor, 401kToGoldIRA.org. A neutral, practical catch-up guide sourced to the IRS, SSA, CFPB, Fidelity, and the World Gold Council; educational only, not financial, tax, or legal advice.