Educational only: This article summarizes IRS rules and general planning considerations. It is not financial, tax, or legal advice, and contribution limits, RMD ages, and rules can change. Customers should speak to a financial or tax advisor before making decisions. Goldco does not offer tax or legal advice. Past performance does not guarantee future results.

Gold does not replace earned income, regular contributions, broad stock and bond exposure, emergency reserves, or a realistic retirement budget. The stronger question is not whether age 55 is too late — it is whether a Gold IRA would serve a clear role inside a balanced portfolio without weakening growth, liquidity, or income planning.

Quick Answer: Is 55 Too Late for a Gold IRA?

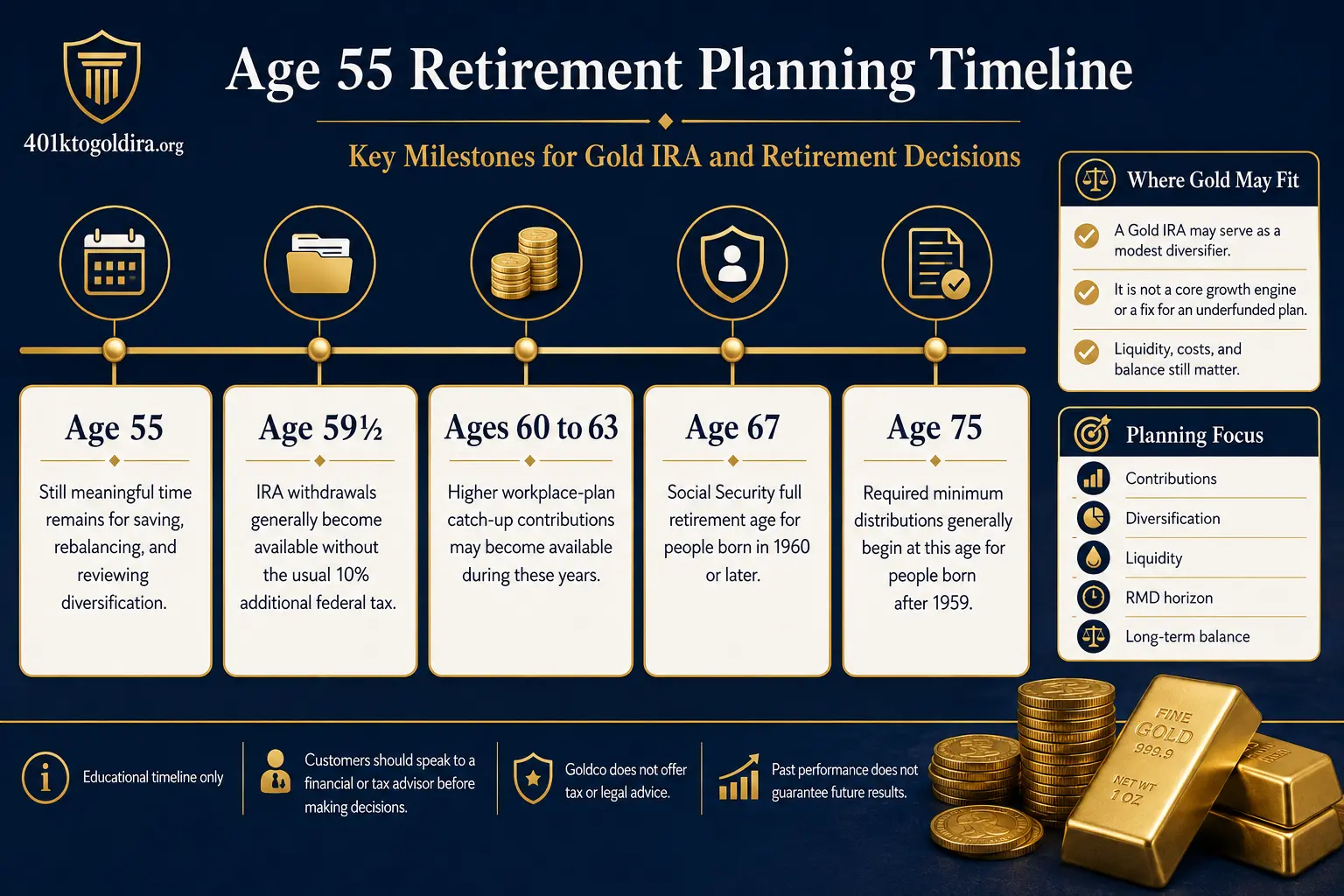

Age 55 is not too late to open or fund a Gold IRA. It can still leave a long holding period before retirement distributions or required withdrawals begin. Several timing facts matter:

- Social Security full retirement age is 67 for people born in 1960 or later.

- IRA withdrawals before age 59½ can generally face a 10% additional federal tax unless an exception applies.

- People born after 1959 generally have an applicable required minimum distribution age of 75 under the final Treasury regulations.

- Workers age 50 or older can use catch-up contribution limits when their workplace plans permit them.

These rules create several planning windows: the years from 55 to 59½ may focus on contributions and avoiding unnecessary withdrawals; 59½ to retirement may allow more flexible distribution planning; and the years before age 75 can support Roth-conversion, withdrawal, and RMD planning. A gold IRA at 55 may fit as a modest diversifier — it should not become the main growth engine, emergency fund, or entire strategy. Customers should speak to a financial or tax advisor before making decisions involving contributions, allocations, rollovers, withdrawals, or RMDs. Goldco does not offer tax or legal advice.

Retirement Planning at 55 With Precious Metals: The Time Horizon

The phrase "10-year retirement horizon" can be useful, but it can also be too simple. A 55-year-old who expects to stop full-time work at 65 has about a decade before that date; a person born after 1959 reaches Social Security full retirement age at 67, a 12-year span from age 55. Retirement assets may then need to support spending for many more years. That means a portfolio at 55 can have several time horizons at once — cash needed in the next few years has a short horizon, money for the first part of retirement has a medium horizon, and assets for later retirement or heirs can have a much longer one.

Investor.gov explains that asset allocation depends heavily on the time horizon and ability to tolerate loss: a shorter horizon often supports less exposure to volatile assets, while a longer horizon can allow more risk. This is why age alone cannot determine the right allocation at 55 — income, savings rate, pension benefits, Social Security timing, debts, health costs, liquidity needs, and risk tolerance all matter. Age 55 is still early enough to improve a plan, but late enough that major mistakes (high-cost products, concentrated positions, unnecessary taxable withdrawals) can be harder to repair. A remaining decade can let returns compound, but new savings can be equally important — the Gold IRA calculator can organize account values for educational review, though it does not replace a complete retirement-income analysis.

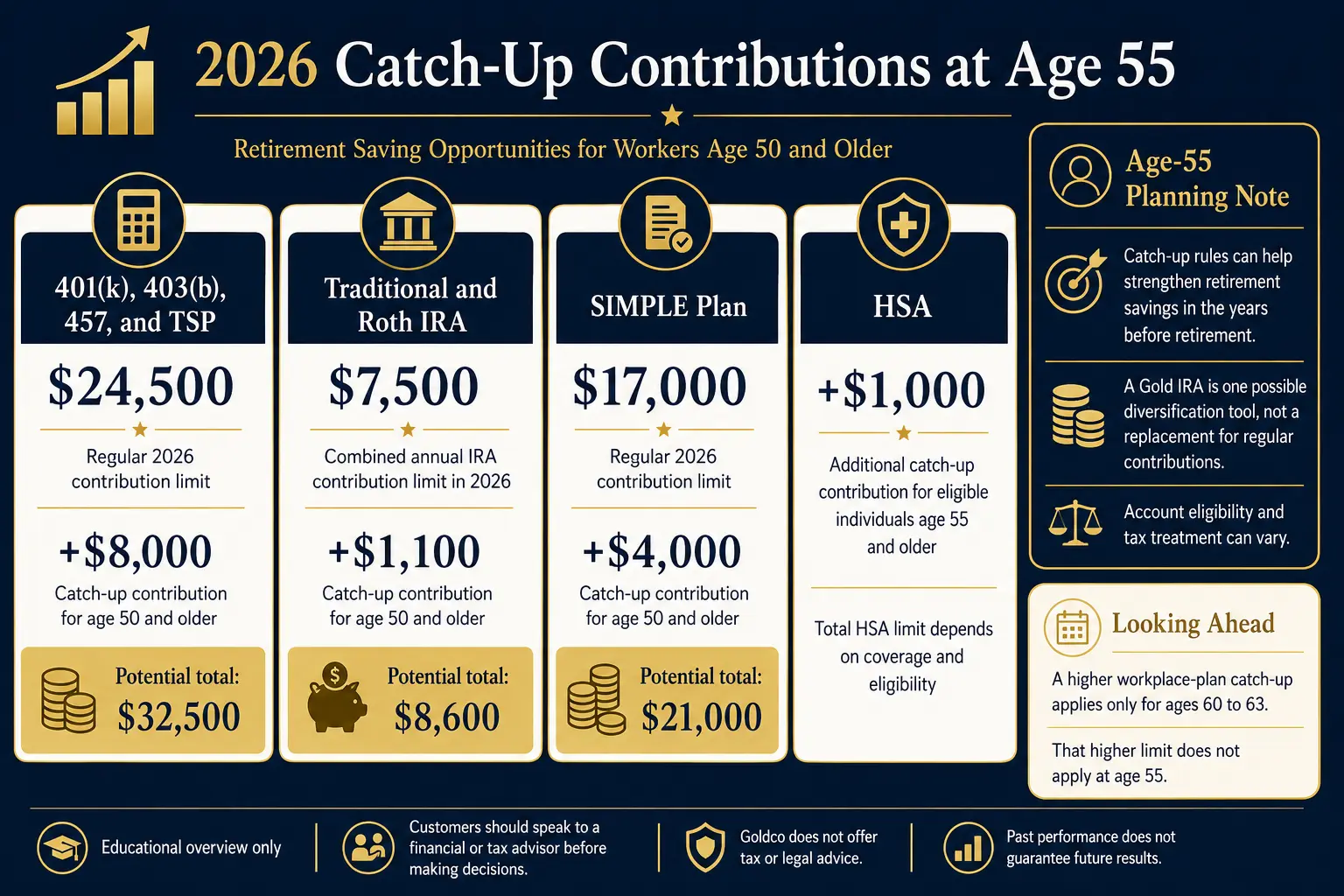

Catch-Up Contributions and Account Options at 55+

Federal catch-up rules become available before age 55. A participant who is age 50 or older by the end of the year may qualify when the plan permits catch-up contributions.

| Account or plan | Regular 2026 limit | Catch-up at 55 | Potential total at 55 |

|---|---|---|---|

| Most 401(k), 403(b), 457, TSP | $24,500 | $8,000 | $32,500 |

| Traditional + Roth IRA (combined) | $7,500 | $1,100 | $8,600 |

| Most SIMPLE plans | $17,000 | $4,000 | $21,000 |

| HSA (when otherwise eligible) | Coverage-based | +$1,000 | Depends on coverage |

The IRS published the 2026 workplace-plan, IRA, and catch-up limits in November 2025. IRA contribution eligibility and deductibility can depend on compensation, income, filing status, and workplace-plan coverage. These limits are annual maximums, not automatic recommendations — employer plan terms, compensation, tax circumstances, and household cash flow can reduce the practical amount.

SECURE 2.0 rules relevant at age 55

SECURE 2.0 created a higher workplace-plan catch-up limit for participants who turn 60, 61, 62, or 63 during the year. For 2026, that higher limit is $11,250 instead of the standard $8,000 catch-up. A 55-year-old does not qualify for the age-60-to-63 limit yet, but the rule can become part of a five-year savings plan. Beginning in 2026, participants in plans with Roth features generally must make catch-up contributions on a Roth basis when prior-year wages from the plan sponsor exceeded $150,000 — that rule applies to workplace-plan catch-up contributions and does not convert an existing traditional IRA or Gold IRA into a Roth account. Customers should speak to a financial or tax advisor before making decisions involving catch-up contributions, Roth treatment, IRA deductibility, or account selection. Goldco does not offer tax or legal advice.

Balanced Diversification, Not a Single Asset

A balanced portfolio near retirement usually has more than one job: continue growing faster than inflation, reduce the effect of a major market decline near retirement, provide liquid assets for near-term spending, support predictable withdrawals, and limit fees and unnecessary tax costs. Investor.gov states that asset allocation is personal and should reflect the time horizon and risk tolerance, and notes that many people hold less stock and more bonds and cash as retirement approaches. That does not mean eliminating growth assets at 55 — stocks have historically provided greater growth potential than bonds and cash, while also producing more short-term volatility, and precious metals carry their own category-specific risks. Gold should therefore be evaluated as one possible diversifier, not a replacement for the entire stock, bond, and cash structure. A balanced portfolio can also use rebalancing, which returns holdings toward a planned allocation after market movements — Investor.gov advises focusing on goals, horizon, and risk tolerance rather than chasing whichever asset recently performed well.

Where a Modest Precious-Metals Allocation May Fit

No public rule establishes one correct gold percentage for every 55-year-old. Any exact allocation depends on the full portfolio, retirement date, income needs, risk tolerance, existing metal exposure, and cost structure — research can provide scenarios, but not a personal answer. A 2026 State Street Global Advisors study tested hypothetical multi-asset portfolios with 2%, 5%, and 10% allocations to a gold-backed exchange-traded product; over the historical period from January 2005 through March 2026, the hypothetical portfolios with gold showed higher risk-adjusted returns and lower maximum drawdowns than the comparison portfolio without gold, while State Street also states that results vary with allocation choices and market performance. Those percentages are research scenarios from an asset manager that sponsors a gold product. They are not an allocation rule for a Gold IRA, and they do not show that the same result will occur in the future. The useful lesson is narrower: study-based ranges often test a minority allocation rather than replacing the core portfolio. The how much gold to own in retirement guide provides a broader framework without treating any range as universally suitable.

A modest gold allocation can be easier to integrate with stock exposure for long-term growth, bonds for income and lower volatility, cash for near-term needs, Social Security and pension income, and RMD and tax planning. A larger allocation can increase concentration risk and may reduce exposure to income-producing or growth-oriented assets. FINRA and the CFTC warn that dealer premiums, buyback spreads, storage, insurance, administration, and taxes can affect precious-metals results, and advise obtaining all costs and the dealer's repurchase price in writing. A self-directed Gold IRA holds qualifying physical metals through a trustee or custodian, while other regulated products can provide metals-price exposure inside some existing brokerage IRAs with different ownership, liquidity, fee, counterparty, and tax features — so the correct comparison is not only gold versus no gold, but physical Gold IRA custody versus regulated market products.

Liquidity, RMD Horizon, and the Shift Toward Stability

At age 55, liquidity deserves more attention than it did earlier in a career. Traditional and Roth IRA distributions before age 59½ can generally face a 10% additional federal tax on the taxable portion unless an exception applies — that makes the next several years important, and money expected to cover near-term needs may not belong in an illiquid or costly retirement holding. A Gold IRA can be sold or distributed, but the process can involve a dealer, custodian, depository, transaction paperwork, and delivery or wire instructions, and dealer spreads and administrative costs can reduce the amount available.

The final Treasury regulations state that people born after 1959 generally have an applicable RMD age of 75, and a person who is 55 in 2026 falls within that group — creating about 20 years before traditional IRA RMDs would generally begin (original Roth IRA owners do not take lifetime RMDs). The long runway does not remove the need for planning: a physical-metals IRA may eventually need enough cash or planned metal sales to cover fees and required distributions. The Gold IRA RMD strategy guide explains later-life distribution issues; for a current 55-year-old, the key point is that RMD planning can start long before the first required withdrawal. Customers should speak to a financial or tax advisor before making decisions involving liquidity, early distributions, Roth conversions, or RMD planning. Goldco does not offer tax or legal advice.

Rolling Existing Retirement Money Into a Self-Directed IRA

A Gold IRA is usually funded through a new IRA contribution, a transfer between IRAs, or an eligible rollover from a workplace plan. A direct rollover or trustee-to-trustee transfer sends retirement money from the existing plan or IRA to the receiving trustee or custodian; the IRS states that a direct trustee-to-trustee movement does not use the 60-day rollover deadline because the individual does not receive the funds. In a 60-day rollover, an eligible distribution is paid to the individual, who must redeposit the eligible amount within 60 days — and workplace-plan distributions paid to an individual can be subject to withholding, which can create a funding gap. Direct handling is often simpler because it reduces timing and withholding problems, though not every account or distribution is eligible.

Gold and other metals are generally treated as collectibles inside an IRA, with exceptions for specified coins and qualifying bullion that must remain in the physical possession of a bank or an IRS-approved nonbank trustee. A self-directed custodian processes the account, but custodian acceptance does not prove that a dealer price or allocation is appropriate — FINRA states that self-directed IRA customers remain responsible for evaluating the asset, dealer, costs, and risks. The rollover guide provides a fuller explanation of direct and indirect rollover mechanics. Customers should speak to a financial or tax advisor before making decisions involving a rollover, transfer, Roth conversion, or self-directed IRA. Goldco does not offer tax or legal advice.

Questions to Ask Before Adding Metals at 55

A useful review should begin with the retirement plan rather than the product:

- What retirement date is being planned, and how much annual spending must the portfolio support?

- Which expenses will be covered by Social Security, pensions, or other income, and how much liquid cash is needed before and after retirement?

- Is the current portfolio too concentrated in stocks, employer shares, cash, real estate, or another asset?

- What specific role would precious metals perform, and what percentage would remain after considering every existing metals holding?

- Which assets would be reduced to fund the metals allocation, and how would that change expected growth, income, and liquidity?

- What are the dealer premium and written buyback price, and the custodian, storage, insurance, wire, distribution, and close-out fees?

- How long could liquidation take, and is a physical Gold IRA necessary or could another regulated form of metals exposure meet the same goal?

- Would additional workplace-plan or IRA contributions have greater planning value, and how would the account fit into future Roth-conversion and RMD planning?

The Gold IRA quiz can organize some of these educational questions before a company conversation.

Frequently Asked Questions

Is 55 too late to open a Gold IRA?

No federal rule makes age 55 too late. The decision depends on the retirement horizon, total portfolio, liquidity needs, fees, risk tolerance, and the role assigned to precious metals.

How much can a 55-year-old contribute in 2026?

A participant age 55 can generally contribute up to $24,500 plus an $8,000 catch-up to most 401(k), 403(b), governmental 457 plans, and the TSP when the plan permits it. The combined traditional-and-Roth IRA limit is $7,500 plus a $1,100 catch-up, subject to eligibility rules.

Does the higher age-60-to-63 catch-up apply at 55?

No. The higher workplace-plan catch-up applies only in years when the participant turns 60, 61, 62, or 63. For 2026, that limit is $11,250 instead of the standard $8,000 catch-up.

What gold percentage is appropriate at age 55?

No universal percentage can be verified. Some industry-sponsored hypothetical studies have tested allocations from 2% to 10%, but those scenarios are not personal recommendations and do not predict future results. Any exact allocation depends on the full portfolio, retirement date, income needs, and risk tolerance.

When would RMDs begin for a person who is 55 in 2026?

A person who is 55 in 2026 was born after 1959. Under the final Treasury regulations, the applicable RMD age for people born after 1959 is generally 75, which creates about 20 years before traditional IRA RMDs would generally begin. Original Roth IRA owners do not take lifetime RMDs.

Can an existing 401(k) be rolled into a Gold IRA?

An eligible workplace-plan distribution may be rolled into an IRA, but eligibility depends on the plan and transaction. A direct rollover moves funds to the receiving custodian, while a payment made to the individual normally carries a 60-day rollover deadline and possible withholding.

Update Log

- 2026: Initial publication. 2026 contribution and catch-up figures per IRS Notice 2025-67 and the IRS 2026 limits release; RMD age per the final Treasury regulations; allocation scenarios cited from a State Street Global Advisors study (sponsor-published, not a recommendation). Confirm current figures with the IRS or a professional before acting.

Sources

- Social Security Administration. 1960.

- Internal Revenue Service. 401k limit increases to 24500 for 2026 ira limit increases to 7500.

- Internal Revenue Service. Retirement Topics — Catch-Up Contributions.

- Internal Revenue Service. N 25 67.

- Internal Revenue Service. Publication 969 (HSAs and Other Tax-Favored Plans).

- Internal Revenue Service. Tc557.

- Internal Revenue Service. 2024 33 IRB.

- Internal Revenue Service. Publication 590-B (Distributions from IRAs).

- Internal Revenue Service. Rollovers of Retirement Plan and IRA Distributions.

- Internal Revenue Service. Verifying rollover contributions to plans.

- Internal Revenue Service. Investments in Collectibles in IRA Accounts.

- Internal Revenue Service. Retirement Plans FAQs Regarding IRAs.

- Investor.gov (SEC). Beginner's Guide to Asset Allocation.

- Investor.gov (SEC). Asset Allocation Basics.

- FINRA. 10 Things to Ask Before Buying Physical Gold, Silver or Other Metals.

- State Street Global Advisors. Spdr invest in gold.

Article reviewed and edited by Daniel M. — editor, 401kToGoldIRA.org. Sourced to IRS.gov, the Social Security Administration, FINRA, and Investor.gov; educational only, not tax or legal advice.