Educational only: This guide summarizes IRS and FINRA guidance and published custodian processes in general terms. It is not financial, tax, or legal advice. RMD rules and figures should be confirmed against current IRS guidance for the specific year. Customers should speak to a financial or tax advisor before making decisions. Goldco does not offer tax or legal advice. Past performance does not guarantee future results.

A traditional Gold IRA follows the same RMD rules as any traditional IRA: distributions begin at age 73, the first-year amount uses a 26.5 Uniform Lifetime factor on the prior year-end value, and a missed RMD carries an excise tax of up to 25% of the shortfall.

Source: IRS — Required Minimum Distributions FAQs. The excise tax can fall to 10% if corrected within the permitted two-year period (Form 5329).

Key takeaways

- RMDs begin at age 73; the amount is the prior December 31 account value divided by the applicable life-expectancy factor (26.5 at 73 under the Uniform Lifetime Table).

- A Gold IRA needs a reliable year-end valuation of the metal before the RMD can be calculated.

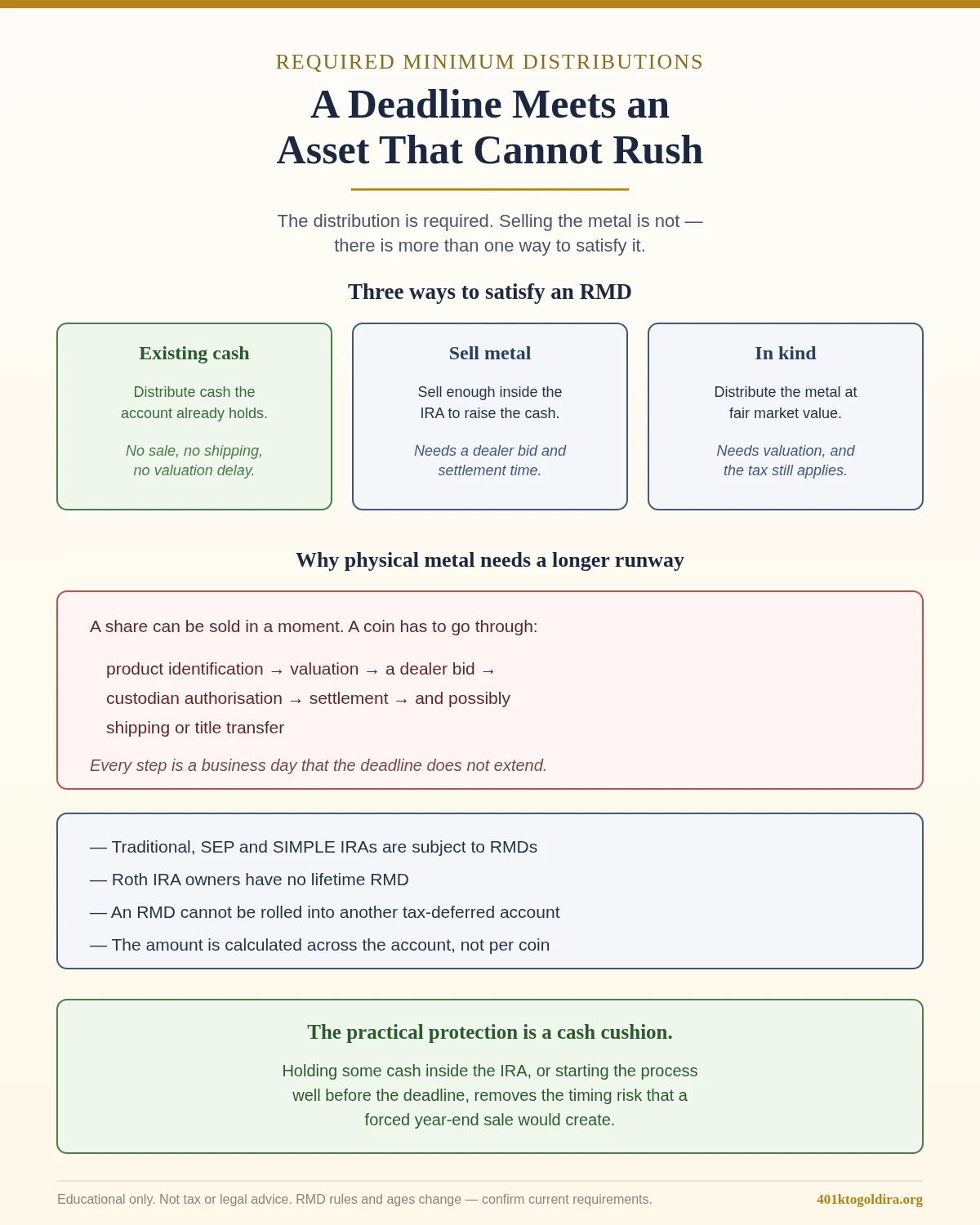

- The RMD can be taken as cash (custodian sells metal) or in-kind (specific coins/bars distributed) — the assigned value counts toward the RMD, and the metal becomes personally owned outside the IRA.

- An in-kind gold RMD is generally taxable at ordinary rates; receiving metal instead of cash does not remove the tax.

- Missing an RMD triggers an excise tax of up to 25% of the shortfall, reducible to 10% if corrected timely.

Quick Answer: What Changes for a Gold IRA at Age 73

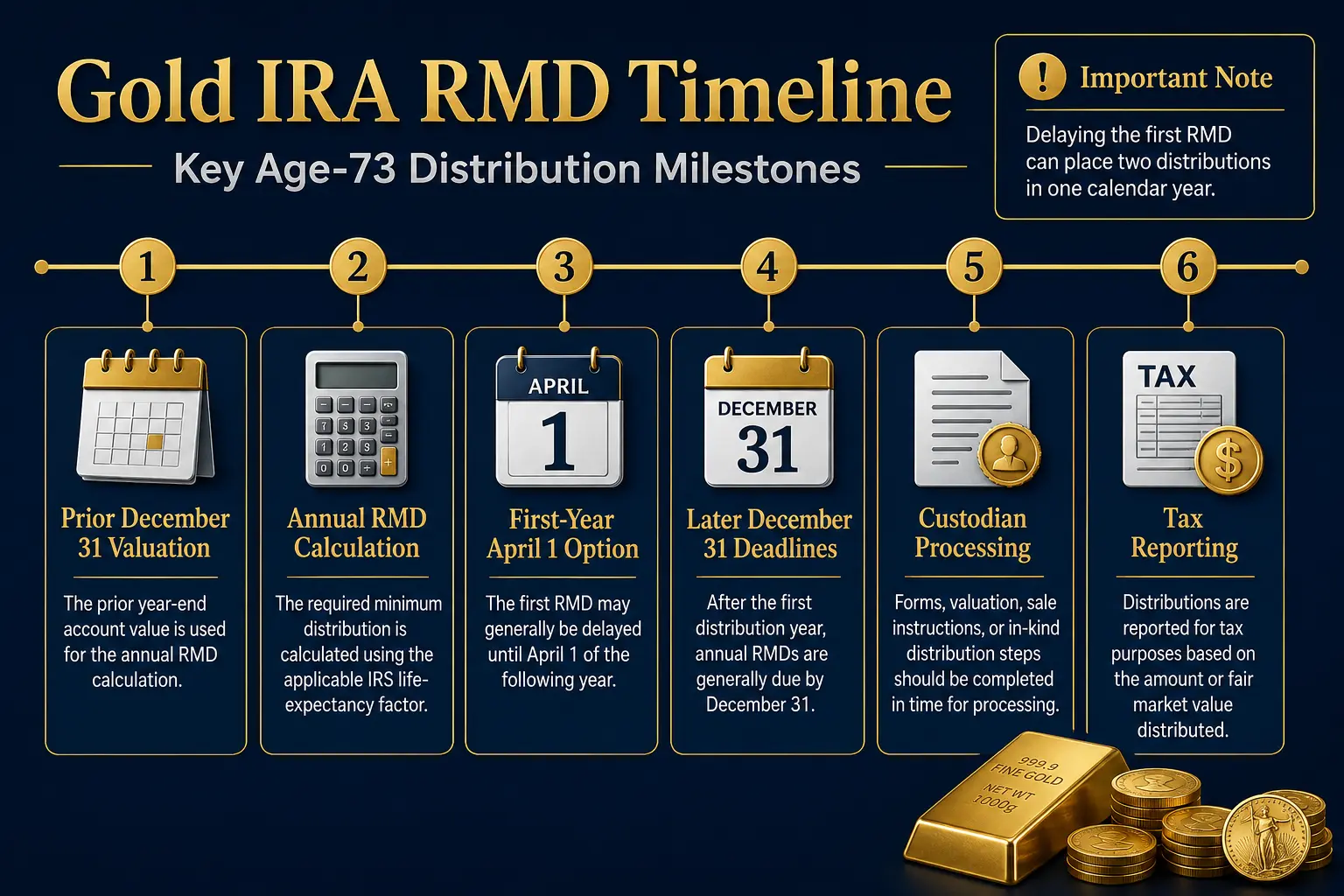

The current IRS rule generally requires traditional IRA owners to begin RMDs for the year they reach age 73 when they reached age 72 after December 31, 2022. The first RMD may be delayed until April 1 of the following year, but the second RMD is still due by December 31 of that same following year. Delaying the first payment can therefore place two taxable distributions in one calendar year (IRS: RMD FAQs). SECURE 2.0 also provides a later age-75 starting point for people who attain age 74 after December 31, 2032; that future rule does not change the present age-73 phase for current retirees (IRS: Final RMD Regulations).

For a traditional Gold IRA, the annual process has four parts: confirm the prior December 31 account value; calculate the RMD using the applicable IRS life-expectancy factor; decide whether to distribute cash, physical metal, or a combination; and complete the custodian and depository paperwork before the deadline. The RMD is a minimum withdrawal, not a requirement to close the Gold IRA. More can be distributed, but an excess distribution does not reduce a future year's RMD (IRS: Publication 590-B). Customers should speak to a financial or tax advisor before making decisions involving an RMD, distribution method, withholding, IRA aggregation, or taxes. Goldco does not offer tax or legal advice.

Gold IRA Strategy After Age 73: How the RMD Is Calculated

The Basic Formula

The IRS generally calculates an IRA owner's RMD by dividing the adjusted market value of the IRA on the previous December 31 by the applicable distribution period from an IRS life-expectancy table. Most owners use Table III, the Uniform Lifetime Table. A different table applies when the spouse is the sole beneficiary and is more than 10 years younger (IRS: RMD Comparison Chart). The basic formula is: RMD = prior December 31 IRA value ÷ applicable IRS denominator. Table III uses a denominator of 26.5 at age 73, 25.5 at age 74, and 24.6 at age 75. An illustrative age-73 calculation:

| Input | Example value |

|---|---|

| Prior December 31 Gold IRA value | $265,000 |

| Age-73 denominator (Table III) | 26.5 |

| RMD | $10,000 |

This example uses simple arithmetic and does not estimate future gold prices or account fees.

The First-Year Deadline Can Create Two Distributions

The first RMD is for the year in which the account owner reaches age 73. It can be taken by December 31 of that year or delayed until April 1 of the next year. Every later RMD is due by December 31. A delayed first RMD does not delay the second one: an account owner who postpones the first distribution until the following spring may need another RMD by the end of that same year. The combined taxable income may affect tax brackets, Medicare-related income calculations, deductions, and other planning items. No universal choice is preferable — the decision depends on total income, charitable planning, withholding, estimated taxes, and liquidity.

Traditional and Roth Gold IRAs Are Different

Traditional, SEP, and SIMPLE IRAs generally have lifetime RMD rules. Roth IRAs do not require lifetime RMDs for the original owner, although beneficiaries are subject to post-death distribution rules. The tax label of the IRA therefore matters as much as the asset held inside it. Physical gold does not create a separate RMD system.

Year-End Valuation for Physical Gold

Why Valuation Matters

An RMD calculation begins with the prior December 31 account value. IRS guidance states that plan assets must be valued at fair market value rather than historical cost, and accurate valuation is necessary for tax compliance (IRS: Valuation of Plan Assets at Fair Market Value). A Gold IRA custodian normally reports the IRA's year-end fair market value and administers the RMD process. The method used to value metals should be reviewed before year-end because a bar, common bullion coin, graded coin, or specialty product may not have the same resale market. The account file should identify metal type and product name, weight and purity, quantity held, the December 31 price source, whether the value reflects bid/ask/spot or another method, who supplied the valuation, and whether any asset lacked a current market quote. A custodian's reported value is used for administration, but it does not promise that a dealer will pay that amount during a sale.

Valuation and Liquidity Are Not the Same

A year-end statement may show a value based on metal prices, while an actual liquidation can produce a lower amount after dealer spreads, product-specific discounts, shipping, or transaction charges. FINRA advises physical-metals customers to compare spot value, retail price, all charges, and the amount a dealer would pay to repurchase the item immediately (FINRA: Buying Physical Gold, Silver, or Other Metals). For RMD planning, valuation determines the annual RMD calculation, while liquidation proceeds determine how much cash a sale produces — and those figures can differ.

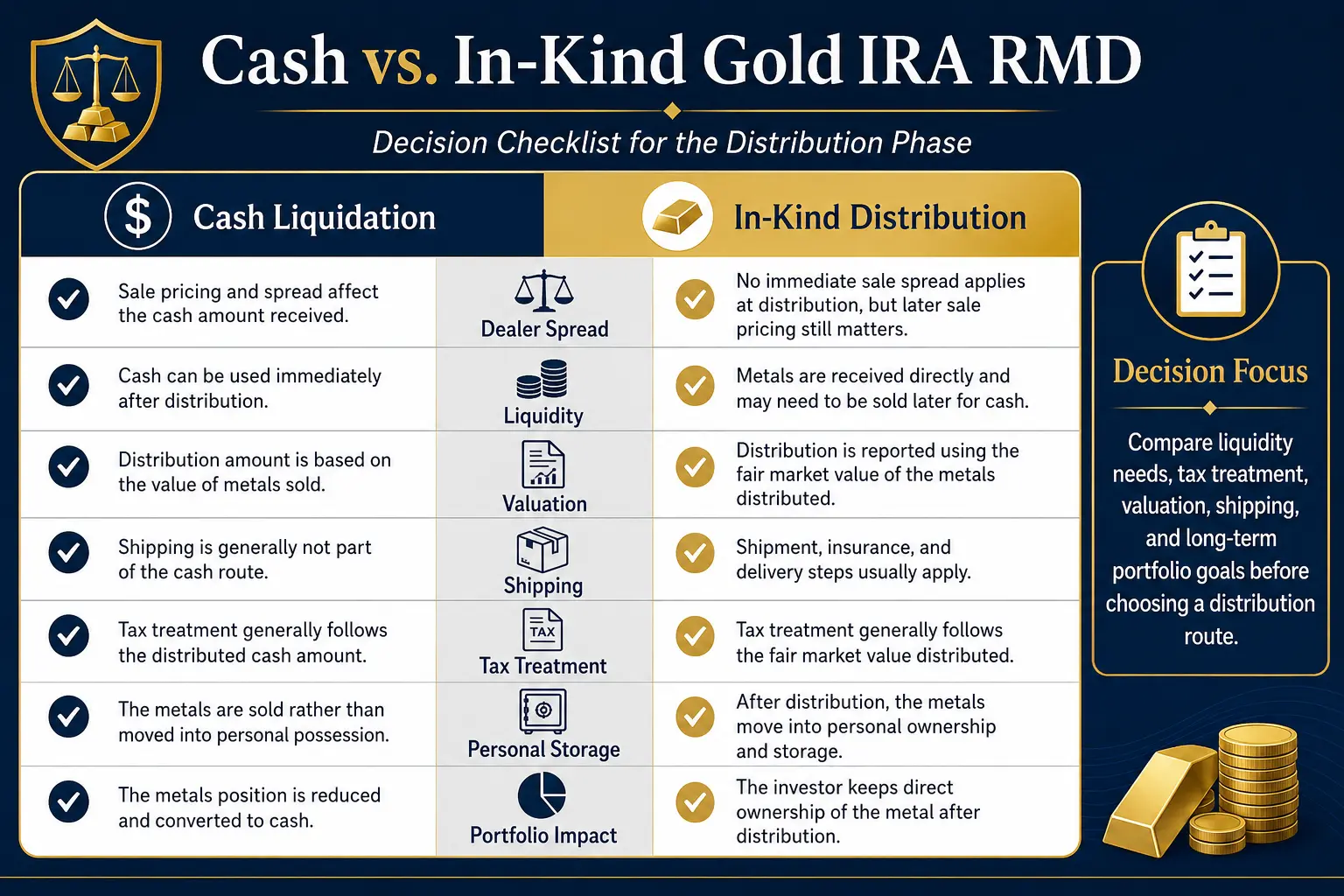

Cash Distribution of a Gold IRA RMD

A gold ira rmd cash transaction generally requires enough cash inside the IRA to make the distribution. Cash may already be present, or some metals may need to be sold. A common operational sequence: the account owner gives liquidation instructions to the custodian; sale details are confirmed with a precious-metals dealer; the depository releases the selected metal for settlement; sale proceeds return to the IRA as cash; and the custodian sends the cash distribution and reports it for tax purposes. GoldStar Trust's published RMD process states that when an account lacks sufficient cash, liquidation paperwork may be required and sale details must be arranged with the precious-metals dealer, and that distribution fees can apply. Custodian procedures and fees vary and should be confirmed directly (GoldStar Trust: Education).

Dealer Spreads Affect the Cash Route

The cash route exposes the account to the dealer's current repurchase price. The dealer may quote below spot, especially for specialty coins, small products, or items with limited resale demand. The written liquidation record should include the current spot price, exact product and quantity sold, dealer bid or repurchase price, percentage of spot received, shipping or processing charges, custodian distribution charge, and net cash returned to the IRA. A cash RMD may be operationally simple after liquidation, but selling during an unfavorable price period can reduce the metal position more than expected. A planned cash reserve inside the IRA can reduce the need for a late-year forced sale.

In-Kind Distribution of Physical Metals

A gold ira rmd in kind transfers actual IRA-owned coins or bars out of the retirement account rather than selling them for cash. GoldStar Trust describes an in-kind distribution as a payment made with securities or other property instead of cash, requiring a distribution request that identifies the specific assets. The Entrust Group also distinguishes cash and in-kind self-directed IRA distributions and explains that in-kind treatment can be used for noncash assets (Entrust Group: Self-Directed IRA Distribution Rules). A typical sequence: the custodian calculates or confirms the remaining RMD; the account owner selects specific metals; the custodian prepares the distribution and tax reporting; the depository ships or transfers the metals; and the distributed metals become personally owned outside the IRA. The value assigned to the in-kind distribution counts toward the RMD; because valuation methods and processing dates can vary, the exact amount credited should be confirmed with the custodian before the transaction is completed.

An In-Kind RMD Is Still a Taxable Distribution

The IRS states that an RMD from a traditional IRA is generally taxed at the account owner's income-tax rate, except to the extent the withdrawal represents after-tax basis. Receiving metal instead of cash does not by itself avoid income tax. After distribution, the metal is outside the IRA, and future personal sales follow the tax rules applicable to personally owned property. Customers should speak to a financial or tax advisor before choosing an in-kind distribution, determining basis, arranging withholding, or later selling distributed metal. Goldco does not offer tax or legal advice.

In-Kind Distributions Can Be Uneven

Physical products come in fixed units. One coin or bar may be worth more or less than the exact remaining RMD. Possible approaches include combining an in-kind metal distribution with cash, selecting smaller-denomination products, distributing slightly more than the minimum, or taking part of the total IRA RMD from another traditional IRA. Any amount above the current-year RMD is still a distribution, but it does not create credit against later RMDs.

Aggregating RMDs Across Traditional IRAs

An owner with more than one traditional IRA must calculate the RMD separately for each account. The separate amounts may then be added together, and the total may be withdrawn from one traditional IRA or from more than one. This rule can make physical gold rmd planning more flexible. For example, a household might calculate a $14,000 traditional brokerage IRA RMD and a $6,000 Gold IRA RMD for a $20,000 total; the $20,000 may generally be taken from the brokerage IRA, the Gold IRA, or a combination, provided the accounts are eligible for IRA aggregation and the full amount is distributed by the deadline. This flexibility may allow a Gold IRA to remain invested while a more liquid IRA supplies the annual cash distribution.

Accounts That Should Not Be Mixed Into the IRA Total

The aggregation rule is not a universal retirement-account rule. Employer-plan RMDs generally follow separate account requirements, and inherited IRAs can have different aggregation limits. A 401(k) RMD should not automatically be combined with a traditional IRA RMD. The account types, ownership, beneficiary status, and plan rules should be confirmed before aggregation.

Taxes and the Missed-RMD Excise Tax

Income-Tax Treatment

Traditional IRA distributions are generally included in taxable income, except for any verified return of nondeductible basis. The custodian normally issues Form 1099-R for the distribution. A Gold IRA distribution may affect federal taxable income, state taxable income, estimated tax payments, withholding choices, Medicare income-related adjustments, and taxation of Social Security benefits. Those effects depend on the complete tax return and cannot be determined from the Gold IRA alone.

The Current Missed-RMD Penalty

The IRS states that an RMD shortfall may be subject to a 25% excise tax. The rate may be reduced to 10% when the missed amount is corrected within the permitted two-year correction period. Form 5329 is used to report the shortfall and related tax. IRS regulations also allow a waiver when the failure was due to reasonable error and reasonable steps are being taken to correct it; a waiver is not automatic in every case. A missed or incomplete distribution should be addressed promptly with the custodian and a tax professional.

Calm Gold IRA Decumulation Planning

Gold ira decumulation is the process of turning an accumulated account into distributions while preserving the desired remaining allocation. A calm plan can use several layers:

- Keep a cash sleeve inside the IRA. Cash can cover upcoming custodian charges and some or all of the RMD, replenished during planned sales rather than a rushed year-end liquidation.

- Set a metal-sale schedule. Reviewing the account earlier in the year creates time to compare dealer bids, confirm settlement dates, and handle paperwork. A schedule does not remove price risk — it reduces administrative pressure.

- Use IRA aggregation deliberately. When other traditional IRAs contain liquid assets, the combined IRA RMD may be paid from those accounts, reducing metal sales, although it may change the asset mix.

- Rebalance after the distribution. A cash withdrawal from a bond or stock IRA can leave gold as a larger percentage of remaining retirement assets even if no new metal is purchased, so the allocation should be measured after distributions, not only before them.

- Coordinate RMDs with spending needs. An RMD is a tax rule, not a spending command. Cash not needed for living expenses can generally be reinvested in a taxable account after distribution, subject to normal rules. An in-kind distribution preserves ownership of the metal outside the IRA but creates personal storage, insurance, recordkeeping, and future-sale responsibilities.

The Gold IRA RMD strategy guide and Gold IRA exit strategies provide related planning frameworks. The need cash from a Gold IRA guide covers liquidation questions in more detail. Customers should speak to a financial or tax advisor before making allocation, distribution, reinvestment, or withholding decisions. Goldco does not offer tax or legal advice.

Coordinating With Beneficiaries and Estate Plans

A Gold IRA in the retirement income phase should have a current beneficiary designation and clear records for the custodian, products, depository, and account value. The IRS states that many non-spouse designated beneficiaries are subject to a 10-year distribution rule, while surviving spouses and certain other eligible designated beneficiaries may have different options (IRS: Retirement Topics — Beneficiary). Physical metals add practical questions for beneficiaries: whether the inherited account will sell or retain the metals; whether distributions will be cash or in kind; how products will be valued; which dealer can provide a current bid; who pays storage, shipping, and custodian charges; and whether the year-of-death RMD has been completed. The beneficiary form should be coordinated with the broader estate plan — a will does not automatically replace the beneficiary designation held by the IRA custodian. The Gold IRA beneficiary rules guide covers post-death planning in more detail, the Gold IRA tax mistakes guide identifies common issues, and the Gold IRA quiz can organize research questions before a company discussion.

A Practical Annual Checklist After Age 73

- Confirm the correct RMD starting age and deadline.

- Obtain the prior December 31 fair market value.

- Verify the IRS table and denominator.

- Calculate each traditional IRA RMD separately.

- Decide whether IRA aggregation will be used.

- Review cash already available inside the Gold IRA.

- Compare cash liquidation with in-kind distribution.

- Obtain a written dealer repurchase quote before any sale.

- Confirm custodian forms, fees, withholding, and processing time.

- Complete the distribution before the deadline.

- Save the valuation, instructions, dealer quote, and tax forms.

- Recalculate the household asset mix after the withdrawal.

- Review beneficiary designations and depository records.

Frequently Asked Questions

Does a Gold IRA have RMDs at age 73?

A traditional Gold IRA generally follows the same age-73 RMD rules as another traditional IRA. Roth IRAs do not have lifetime RMDs for the original owner.

How is a Gold IRA RMD calculated?

The prior December 31 adjusted market value is divided by the applicable IRS life-expectancy factor. Most owners use the Uniform Lifetime Table. At age 73, the Table III denominator is 26.5.

Can physical gold satisfy an RMD?

An IRA custodian may process an in-kind distribution of specific coins or bars. The assigned distribution value counts toward the RMD, and the metals become personally owned outside the IRA. Custodian procedures and valuation methods should be confirmed before processing.

Is an in-kind gold RMD tax free?

No. A traditional IRA RMD is generally taxable at ordinary income-tax rates, except to the extent it represents verified after-tax basis. Receiving property instead of cash does not by itself remove the tax.

Can a Gold IRA RMD be paid from another IRA?

Each traditional IRA RMD must be calculated separately, but the combined amount can generally be withdrawn from one or more traditional IRAs. Employer plans and some inherited accounts follow different rules.

What is the penalty for missing a Gold IRA RMD?

The IRS states that the excise tax can be 25% of the shortfall and may fall to 10% when corrected within the permitted two-year period. Form 5329 is used for reporting.

Conclusion

A gold ira strategy after age 73 is not a one-time withdrawal decision. It is an annual cycle of valuation, calculation, liquidity planning, tax reporting, and portfolio review. Cash distributions can support spending but may require selling metal at the dealer's current bid. In-kind distributions can preserve physical ownership outside the IRA but still create taxable income and personal storage duties. IRA aggregation can add flexibility when other traditional IRAs hold liquid assets. The strongest plan starts early in the year, verifies the prior December 31 value, documents the distribution route, and reviews the remaining allocation after the RMD is complete. Customers should speak to a financial or tax advisor before making decisions involving RMDs, taxes, withholding, aggregation, beneficiaries, or physical-metal distributions. Goldco does not offer tax or legal advice.

Sources

- Internal Revenue Service. Retirement Plan and IRA Required Minimum Distributions FAQs.

- Internal Revenue Service. Retirement Topics — Required Minimum Distributions.

- Internal Revenue Service. RMD Comparison Chart — IRAs vs. Defined Contribution Plans.

- Internal Revenue Service. Publication 590-B (Distributions from IRAs).

- Internal Revenue Service. Valuation of Plan Assets at Fair Market Value.

- Internal Revenue Service. Internal Revenue Bulletin 2024-33 — Final RMD Regulations.

- Internal Revenue Service. Retirement Topics — Beneficiary.

- FINRA. Buying Physical Gold, Silver or Other Metals.

- GoldStar Trust Company. Education (Required Minimum Distributions).

- The Entrust Group. Self-Directed IRA Distribution Rules.

Article reviewed and edited by Daniel M. — editor, 401kToGoldIRA.org. Sourced to the IRS, FINRA, and published custodian processes; educational only, not tax or legal advice. RMD figures should be confirmed against current IRS guidance for the applicable year.

Further Reading

Gold IRA RMD StrategyPlanning required minimum distributions when an IRA holds physical metals.

Gold IRA RMD StrategyPlanning required minimum distributions when an IRA holds physical metals. What Happens If Investors Need Cash From a Gold IRA?Cash-vs-in-kind exit routes, timelines, fees, and spreads.

What Happens If Investors Need Cash From a Gold IRA?Cash-vs-in-kind exit routes, timelines, fees, and spreads. Gold IRA Beneficiary RulesInheritance, trusts, the 10-year rule, and physical-metal distributions.

Gold IRA Beneficiary RulesInheritance, trusts, the 10-year rule, and physical-metal distributions.