Educational only: This is a balanced overview, not a case that tangible assets beat financial ones — most diversified plans are built mainly from financial assets. It summarizes IRS, USDA, Investor.gov, and US Mint material in general terms and is not financial, tax, or legal advice. Customers should speak to a financial or tax advisor before making decisions. Goldco does not offer tax or legal advice. Past performance does not guarantee future results.

Quick Answer: What Tangible Assets Are and Where They Fit

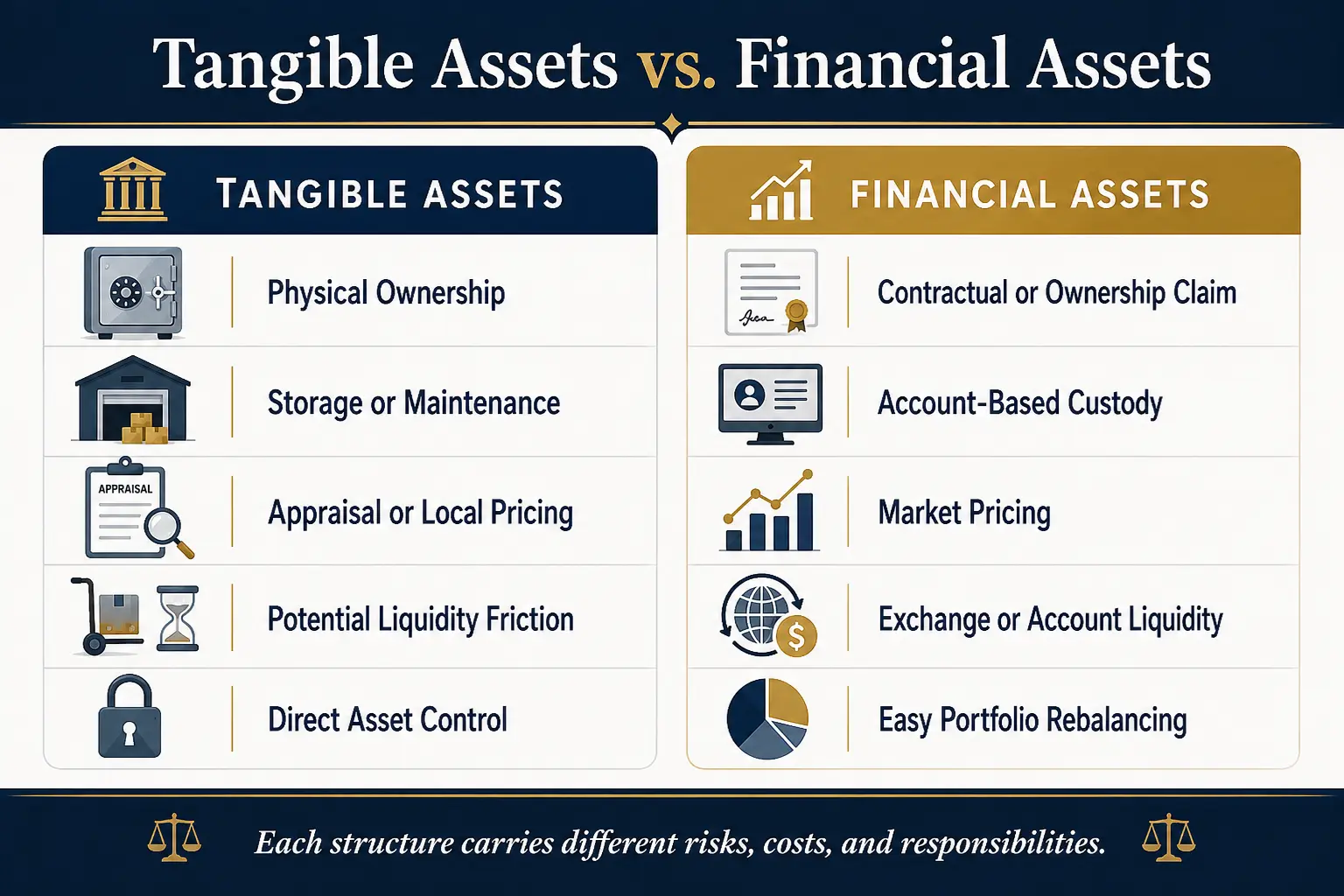

A tangible asset is physical property with value. A financial asset is a legal or contractual claim, such as a share of stock, a bond, a bank deposit, or a fund interest. The difference matters because direct physical ownership changes the source of risk: a stock depends on the company and the market for its shares, a bond depends on the issuer's ability to make payments, and a directly owned property, coin, bar, or collectible exists as an object — but the owner still faces title, theft, damage, storage, insurance, valuation, liquidity, and sale-price risks. A balanced retirement plan usually begins with goals, time horizon, withdrawal needs, and risk tolerance. Investor.gov explains that asset allocation divides investments among categories such as stocks, bonds, and cash, and that the suitable mix changes with the investor's time horizon and ability to accept loss (Investor.gov).

Tangible exposure may then be considered for a limited role: real estate may provide rent and possible appreciation, but direct ownership requires maintenance, taxes, insurance, and local-market liquidity; farmland may produce lease or operating income, but results depend on land quality, tenants, weather, and management; collectibles may have specialist-market value, but authentication, condition, provenance, and resale can be difficult; and physical gold and silver provide direct metal ownership, but they do not produce contractual income and may involve premiums, storage, insurance, and spreads. Diversification can reduce concentration, but it does not prevent all losses — Investor.gov states that diversification spreads exposure across investments and may reduce risk, while broad market declines can still affect a diversified portfolio (Investor.gov).

Tangible vs. Financial Assets: The Real Difference

The phrase "tangible vs financial assets" describes ownership form, not a contest with a universal winner. Tangible assets are physical — a rental home, farmland, a commercial building, gold or silver bullion, art, rare coins, classic vehicles, equipment. Direct ownership normally gives the holder control over the object, subject to title, contract, tax, zoning, or custody rules, and the asset does not depend on an exchange listing to exist. That does not remove outside dependencies: real estate depends on legal title, tenants, contractors, insurers, and local demand; farmland may depend on a tenant or operator; stored metals depend on secure custody and a reliable buyer at sale; and collectibles depend on authentication and a specialist market. Financial assets represent claims or ownership interests recorded through contracts and accounts — stocks are ownership interests in companies, bonds are debt obligations, and fund or ETF shares are interests in pooled portfolios. Investor.gov explains that ETFs pool money from many investors, hold portfolios of securities or other assets, and trade on national exchanges at market prices that can differ from net asset value (Investor.gov). They are often easier to divide into small units, trade, value from market prices, and rebalance, but they carry market, issuer, credit, interest-rate, management, tracking, and fee risks.

Exposure is not the same as possession. A real-estate fund provides financial exposure to property without direct ownership of a building — Investor.gov explains that REITs let individuals share in income-producing real estate without buying and managing commercial property directly (Investor.gov). A gold ETF or trust can provide price exposure through a security, while physical bullion creates direct ownership or a specific custody claim, depending on the product structure. The Gold IRA vs. Gold ETF guide compares those forms in detail. Neither structure is automatically superior — the useful choice depends on the required liquidity, fees, tax treatment, custody preferences, withdrawal plan, and desired level of direct control.

Why Some Investors Want Something Physical

The appeal of hard assets is partly practical and partly psychological. Direct ownership and tangibility: a physical object can be inspected, stored, insured, transferred, or sold, and some investors value that direct connection because the asset is not merely a number on an account statement. The World Gold Council describes gold as an asset that is no one else's liability and carries no credit risk — a statement that applies to gold itself, not to every dealer, custodian, fund, vault, or financing arrangement used to hold it, and one that should be read as industry analysis rather than neutral government guidance (World Gold Council). Direct ownership can reduce one type of counterparty exposure, but it creates other responsibilities: a physical asset can be stolen, damaged, misidentified, poorly insured, difficult to divide, or costly to sell.

Store-of-value and inflation-hedge arguments: some investors use real assets or physical metals because their supply cannot be expanded in the same way as a financial claim, and real estate, farmland, commodities, and metals can respond to inflation, scarcity, replacement cost, or changes in currency purchasing power. That relationship is not stable in every period — a property can lose value during inflation if financing costs rise or local demand weakens, farmland returns can be affected by crop prices and operating costs, gold and silver can decline even when consumer prices rise, and collectible prices can depend more on specialist demand than on broad inflation. The World Gold Council argues gold has historically added diversification and liquidity, while its own disclosures state that diversification does not eliminate losses and that modeled outcomes are not promises. No primary source establishes one tangible-asset percentage appropriate for every retiree. Behavioral comfort: some savers find physical property easier to understand than a complex security, but familiarity can also create overconfidence — a visible asset can still be overpriced, illiquid, uninsured, concentrated, or poorly documented, so a retirement decision should rest on the full economic terms rather than tangibility alone.

The Trade-Offs: Income, Costs, Spreads, Liquidity, and Valuation

Income is uneven across categories. The claim that tangible assets produce no income is too broad: rental real estate and farmland can produce rent, and productive equipment can generate business income, while physical gold, silver, art, and most collectibles do not create contractual interest or dividends — their financial return depends mainly on sale price after costs. A retiree using non-income-producing property may need separate cash, bonds, dividends, rent, Social Security, pensions, or planned sales to fund spending. Storage and insurance costs: physical metals, art, vehicles, and valuable collections may require secure storage and specialized insurance, and real estate and farmland may require property insurance, taxes, repairs, inspections, and management — these expenses belong in net return, because a price increase does not equal a net gain when premiums, maintenance, storage, insurance, taxes, appraisal, and selling costs are ignored. The segregated vs. commingled storage guide and the storage legality matrix cover custody questions for retirement accounts.

Premiums and transaction spreads: physical bullion normally trades above raw metal value at purchase — the U.S. Mint states that bullion coin pricing generally reflects the market value of the metal plus a premium for minting, distribution, and marketing (U.S. Mint) — and the sale price may be below the dealer's retail price, with the difference between a purchase quote and an immediate buyback quote being the starting spread. Real estate has transaction friction through inspections, repairs, commissions, taxes, legal work, and closing costs; collectibles may involve auction commissions, grading, authentication, dealer margins, and shipping. Liquidity friction: a publicly traded security can often be sold in small amounts during market hours, while a house, parcel of farmland, painting, classic car, or bullion holding may take longer to value, market, transfer, and settle — and liquidity varies within a category, so a common bullion coin may have a broader resale market than an unusual collectible. Investor.gov notes that publicly traded REITs trade on exchanges while non-traded REITs may be illiquid and hard to value. Valuation and authentication: financial markets publish frequent prices for listed securities, while physical assets often need appraisal or comparison with recent sales; the U.S. Mint distinguishes bullion coins, valued mainly by metal weight, from numismatic coins, whose value can reflect rarity, condition, age, and limited mintage. A retirement plan should treat an uncertain appraisal as a range rather than a cash equivalent.

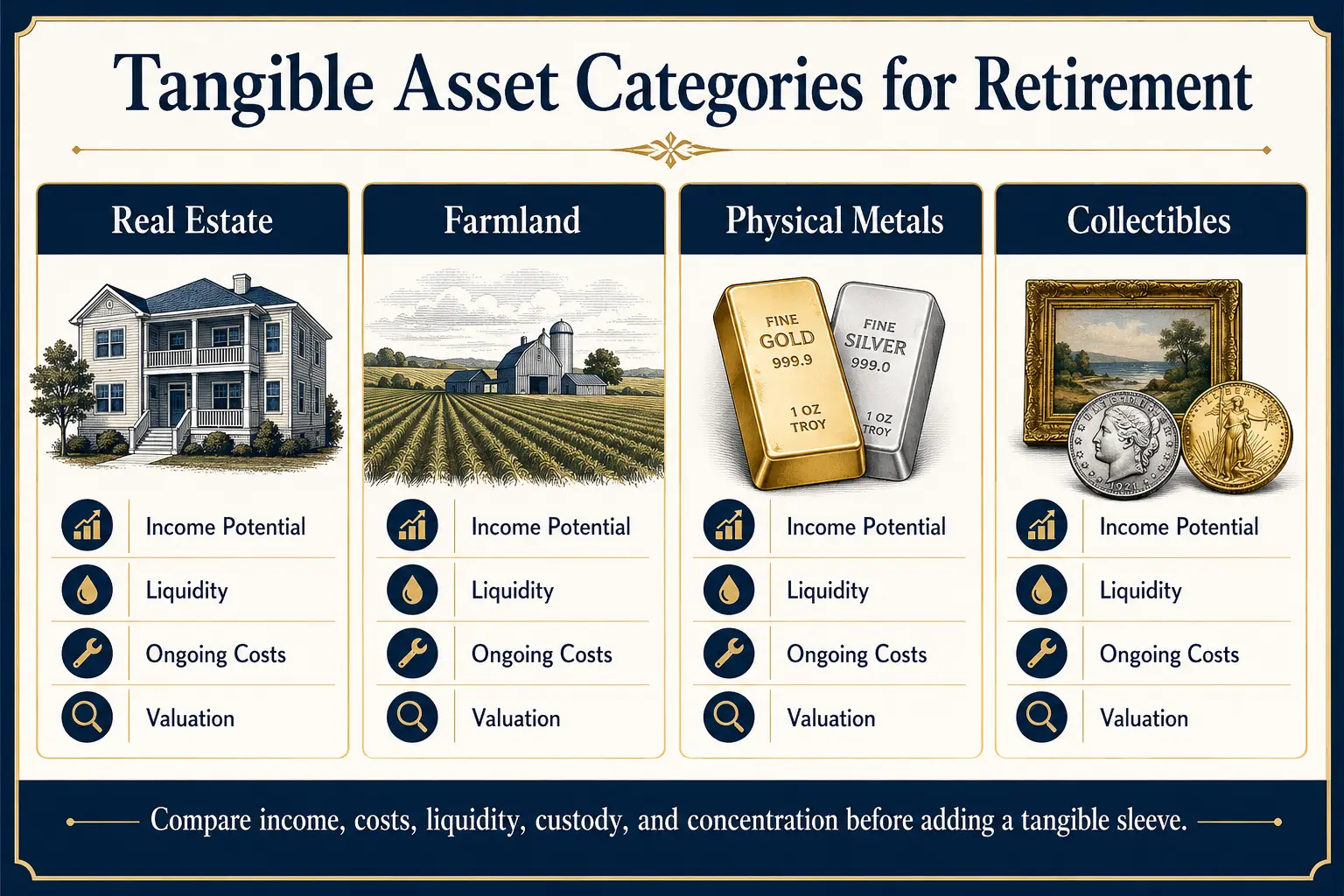

The Main Tangible Asset Categories

Real estate. Direct real estate can provide use, rent, and possible appreciation, but it can also create concentration because one property may represent a large share of net worth. A practical review covers location and local demand, net rent after vacancies and expenses, property taxes and insurance, maintenance and capital repairs, financing terms, management needs, and sale time and transaction costs. A REIT is a financial alternative — Investor.gov states that REITs allow investors to participate in income-producing real estate without buying the property directly, while publicly traded and non-traded REITs have different liquidity, valuation, and fee profiles (Investor.gov).

Farmland. Farmland is both real property and a productive asset, operated directly or rented to a farmer. The USDA Economic Research Service studies farmland ownership, tenants, rental markets, land values, and transfer patterns, noting that farmland is owned by both operators and non-operators and that rental arrangements are a major part of the U.S. farmland market (USDA Economic Research Service). A farmland review should consider soil and water resources, local crop and livestock economics, tenant quality, lease structure, taxes and insurance, environmental obligations, access and improvements, local sale activity, and management and legal costs. Farmland is not a simple inflation trade — income and value can change with weather, interest rates, commodity conditions, policy, and local demand.

Collectibles. Collectibles can include art, antiques, rugs, stamps, coins, wine, memorabilia, and classic vehicles. The appeal may combine personal interest with scarcity, while the drawbacks include uncertain valuation, narrow markets, authentication problems, storage, insurance, condition risk, and high commissions. The IRS lists art, rugs, antiques, metals, gems, stamps, coins, alcoholic beverages, and certain other tangible personal property as collectibles for retirement-plan purposes, subject to limited exceptions (Internal Revenue Service). A collectible should not be treated as readily available retirement cash unless there is a realistic sale process and current independent valuation.

Physical gold and silver. Physical gold and silver can be held as bars, rounds, or coins — bullion products are mainly valued by metal content, while collectible coins may carry additional premiums for rarity or condition. Potential roles include diversification, direct ownership, and exposure to a monetary or commodity asset; trade-offs include no contractual income, purchase premiums, dealer spreads, storage and insurance, theft or loss risk, product verification, tax and custody rules, and liquidity needs during retirement. Gold may behave differently from stocks and bonds in some periods, but it is not a shield against every loss — the World Gold Council presents gold as a diversifier and highly liquid global asset while also warning that diversification does not eliminate loss. The gold allocation backtest and how much gold to hold guide can help frame scenarios without creating a personal allocation recommendation.

Holding Tangible Exposure: Directly, Through a Fund, or in a Self-Directed IRA

The same economic theme can be held through different legal structures. Direct ownership means holding the property or a specific title to it — advantages may include control, use, inspection, and a direct claim to the asset, while disadvantages may include concentration, storage, insurance, maintenance, legal work, valuation, and slower sales. Direct physical ownership also requires a reliable inventory: deeds, titles, invoices, assay records, serial numbers, appraisals, photographs, insurance schedules, and storage instructions should be organized. Fund, ETF, or REIT exposure provides a financial security rather than personal possession of the underlying property — Investor.gov explains that ETF shares trade on exchanges and may trade at a premium or discount to net asset value, and that investors should review the prospectus, strategy, fees, holdings, and redemption structure (Investor.gov). Potential advantages include easier brokerage access, smaller transaction sizes, published market prices, simpler rebalancing, and no personal storage; potential disadvantages include fund expenses, market-price differences from underlying value, tracking differences, manager or structure risk, and no direct possession. A real-estate ETF and a rental house are not interchangeable, and a gold fund and an allocated bullion holding are not the same legal claim.

Self-directed IRA physical assets: a self-directed IRA can hold certain alternative assets, but tax rules limit which physical items qualify. The IRS states that an IRA that acquires a collectible can be treated as making a distribution, and the collectible definition includes many metals, coins, art, antiques, and other tangible items, with limited exceptions for specified coins and qualifying gold, silver, platinum, or palladium bullion; for qualifying bullion, a bank or approved nonbank trustee must keep physical possession (Internal Revenue Service). That physical-possession rule means IRA-owned metals are not handled like personally owned bullion — the custodian administers the account and the approved custody arrangement holds the metal. The full cost may include custodian setup and administration, transaction processing, dealer premiums and spreads, depository storage, insurance, distribution or liquidation charges, and transfer-out or closure fees. Customers should speak to a financial or tax advisor before making decisions involving allocation, taxes, an IRA, a rollover, a self-directed account, or physical-asset custody. Goldco does not offer tax or legal advice. The Gold IRA Calculator can organize cost assumptions and the suitability quiz can organize research questions; neither determines whether an account or asset is appropriate.

How a Modest Tangible Sleeve Fits a Diversified Plan

Tangible assets work best when their purpose is defined. A plan might use a tangible sleeve for diversification from traditional securities, rental or lease income, partial inflation sensitivity, direct ownership, legacy or personal-use value, or exposure to a specialist asset — and it should also define what the sleeve will not do: physical metals will not generate interest or rent, a rental property will not provide instant liquidity, a collectible will not have a continuously quoted price, and farmland may require a tenant or operating plan. A proportionate process begins with the financial core:

- Estimate retirement spending and emergency needs.

- Keep enough liquid assets for near-term withdrawals.

- Set the stock, bond, and cash mix from time horizon and risk tolerance.

- Identify the specific job for each tangible asset.

- Measure all ongoing and exit costs.

- Test a slow-sale or lower-valuation scenario.

- Limit concentration in one property, metal, or collection.

- Review titling, insurance, taxes, and estate documents.

- Rebalance when the tangible sleeve moves far from the intended range.

- Review the plan at least annually and after major life changes.

Investor.gov explains that rebalancing restores a portfolio to its intended allocation after market movements change its risk mix (Investor.gov). No universal allocation was verified for tangible assets for retirement — the amount should be driven by liquidity, income needs, costs, risk capacity, expertise, and the rest of the portfolio. Customers should speak to a financial or tax advisor before making decisions about retirement allocation, taxes, IRA structures, or physical assets. Goldco does not offer tax or legal advice.

Frequently Asked Questions

What are tangible assets for retirement?

Tangible assets are physical property with value, including real estate, farmland, precious metals, art, collectibles, vehicles, and equipment. Their retirement role depends on income, liquidity, costs, valuation, and the full asset allocation.

Are tangible assets safer than stocks and bonds?

Not automatically. Tangible assets replace some market or issuer exposure with property-specific risks such as theft, damage, maintenance, concentration, title problems, storage, appraisal uncertainty, and slower sales.

Do tangible assets protect against inflation?

Some real assets may respond to inflation, scarcity, rent growth, or replacement costs, but the relationship varies by asset and period. No tangible asset provides certain inflation protection.

Do physical gold and silver produce retirement income?

Physical bullion does not produce contractual interest, dividends, or rent. Financial results depend on the eventual sale price after premiums, spreads, storage, insurance, and taxes.

Can physical metals be held in an IRA?

Certain coins and qualifying bullion may be held under limited IRS exceptions. Qualifying bullion must meet the applicable rules and remain in the physical possession of a bank or approved nonbank trustee.

Is a gold ETF the same as physical gold?

No. An ETF is a traded security with a defined fund or trust structure. Physical gold is a directly held asset or a specific custody interest. The two can differ in fees, liquidity, custody, tax treatment, and access.

How much of a retirement portfolio should be tangible?

No universal percentage fits every retiree. The decision should follow the retirement income plan, liquidity needs, time horizon, costs, risk capacity, existing property exposure, and ability to manage the asset.

Conclusion

Tangible assets can add useful features to a retirement plan, including direct ownership, rental potential, specialist value, or exposure that differs from traditional securities. They also create real trade-offs — storage, insurance, maintenance, premiums, appraisal, authentication, taxes, and slow sales can reduce practical value. The balanced approach does not treat tangible assets as superior to financial assets: it uses a diversified financial core, assigns a clear job to any physical holding, preserves enough liquidity for retirement spending, and reviews the total cost before purchase.

Sources

- Internal Revenue Service. Investments in Collectibles in Individually Directed Qualified Plan Accounts.

- Investor.gov (U.S. SEC). Asset Allocation.

- Investor.gov (U.S. SEC). Diversify Your Investments.

- Investor.gov (U.S. SEC). Real Estate Investment Trusts (REITs).

- Investor.gov (U.S. SEC). Mutual Funds and ETFs.

- USDA Economic Research Service. Land Use, Land Value & Tenure.

- U.S. Mint. Collectible Coins.

- World Gold Council. The Relevance of Gold as a Strategic Asset (industry body).

Article reviewed and edited by Daniel M. — editor, 401kToGoldIRA.org. A balanced overview sourced to the IRS, the USDA Economic Research Service, the SEC's Investor.gov, the U.S. Mint, and the World Gold Council (industry source flagged); educational only, not financial, tax, or legal advice.