Educational only: This guide summarizes FINRA, CFTC, IRS, Investor.gov, and independent research in general terms. It is not financial, tax, or legal advice, and it does not recommend for or against any asset or company. Customers should speak to a financial or tax advisor before making decisions. Goldco does not offer tax or legal advice. Past performance does not guarantee future results.

Research shows that couples do not always coordinate retirement choices efficiently. An NBER study using retirement-plan and tax data found that 24% of couples in its sample could have received more employer matching funds by shifting existing contributions between spouses' plans, and that active coordination reduced inefficient contribution choices by 11 to 14 percentage points (NBER, "Do Married Couples Coordinate Their Retirement Savings Efficiently?"). Money discussions can also create tension: a 2026 CFP Board survey reported that 52% of respondents who were married or in a serious relationship had experienced financial tension with a spouse or partner. That survey does not prove a Gold IRA causes conflict, but it shows why a structured conversation matters.

Quick Answer: How a Household Can Evaluate a Gold IRA Idea Together

A household can evaluate a Gold IRA idea without treating the conversation as an argument about who understands the economy better. The discussion can be divided into five questions:

- What problem is the proposed Gold IRA meant to address?

- How much of the total retirement portfolio would move?

- What products, costs, dealer spreads, custody arrangements, and exit terms apply?

- What would the household give up by moving money from the current assets?

- What evidence would cause both partners to approve, reduce, postpone, or reject the proposal?

This method turns "a husband wants gold IRA" or "one spouse wants precious metals" into a due-diligence process. It also gives both partners the same information before a rollover or purchase is discussed. The Financial Industry Regulatory Authority and the Commodity Futures Trading Commission advise prospective precious-metals customers to compare the spot value, dealer premium, spread, fees, commissions, storage charges, and next-day repurchase value before turning over retirement money. Customers should speak to a financial or tax advisor before making decisions involving allocation, retirement-account transfers, rollovers, distributions, or taxes. Goldco does not offer tax or legal advice.

Why One Partner May Be Drawn to Gold

One partner may become interested in gold after hearing a sales presentation, watching economic news, speaking with a friend, or reading about inflation, government debt, currency risk, or stock-market volatility. Those concerns do not make the proposal automatically sound or unsound. They explain the goal the proposed asset is expected to serve. Common goals may include reducing dependence on stocks, holding a tangible asset inside a retirement account, adding an asset that may behave differently from stocks and bonds, responding to inflation or policy uncertainty, reducing anxiety about a concentrated portfolio, or following a recommendation from a trusted friend, media figure, or salesperson.

Gold prices can be affected by supply and demand, inflation expectations, the U.S. dollar, geopolitical events, interest-rate conditions, and investor sentiment. Those forces do not move gold in one direction at all times. The CFTC states that precious-metals prices can be volatile and that promotional claims based on past performance should not be treated as reliable forecasts. The first useful question is therefore not, "Is gold good?" It is, "What household risk is this proposal expected to address?" A partner concerned about inflation may need a different comparison than a partner concerned about stock concentration. A partner reacting to a high-pressure pitch may need time and independent sources before discussing allocation.

Separate the Emotion From the Numbers

Behavior and math both matter in a couples retirement disagreement gold discussion. A sales pitch may begin with a real concern but move quickly to a large transaction. That sequence can make a disagreement feel personal: one partner may hear caution as dismissal, while the other may hear enthusiasm as recklessness. A neutral worksheet can separate the concerns from the transaction.

Write Down the Concern

Each partner can state the main concern in one sentence, such as inflation, market concentration, retirement timing, distrust of paper assets, or worry about future income. The concern should then be tested against the current household balance sheet. A portfolio that already includes inflation-linked bonds, international stocks, real estate, and cash may have different gaps from one concentrated in a single employer or a few stock funds.

Write Down the Proposed Transaction

The proposal should include the dollar amount to be moved, the percentage of all retirement assets involved, the source account, the assets that would be sold, the proposed custodian and dealer, the specific metals and products, every one-time and recurring cost, the expected holding period, and the planned exit method. This step often reveals whether the discussion is about adding a small diversifier or replacing a large part of the retirement plan.

Compare Like With Like

A Gold IRA should not be compared only with cash under a mattress or one stock-market downturn. It should be compared with the actual assets that would be sold and the role those assets play — including liquidity, income, costs, taxes, and the effect on the household's full retirement plan.

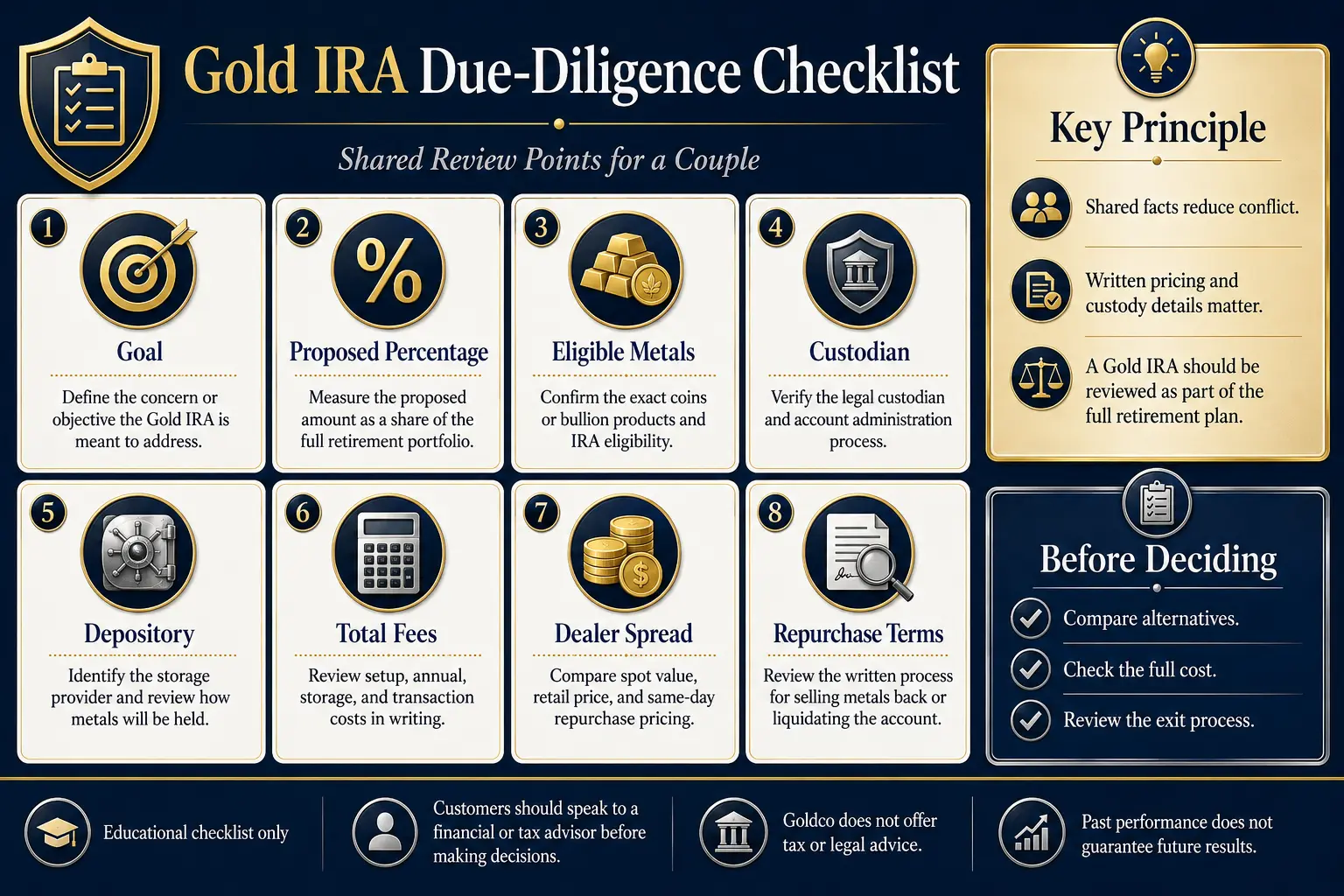

The Facts Both Partners Should Confirm

Gold IRA due diligence spouse discussions should use written documents rather than verbal summaries.

1. What a Gold IRA Is

A "Gold IRA" is a common marketing name for a self-directed individual retirement account that holds qualifying precious metals. FINRA describes these accounts as self-directed IRAs and warns that the account holder carries more responsibility for investigating the assets and transaction. The tax category remains an IRA; the metal does not create a separate special tax treatment.

2. Which Metals Are Eligible

The IRS generally treats metals and coins as collectibles, but Internal Revenue Code Section 408(m) provides exceptions for certain coins and for gold, silver, platinum, or palladium bullion meeting the required fineness when a bank or approved nonbank trustee has physical possession. The IRS consumer guidance does not provide one simple page containing every current product and fineness detail, so the household should obtain the exact product name, metal content, mint, weight, and written eligibility confirmation from the custodian before purchase. Marketing language such as "IRA-approved" should not replace that check. Buying a nonqualifying collectible through an IRA can be treated as a distribution, with ordinary income tax and a possible additional tax for an early distribution.

3. Who Holds the Metals

The IRS states that qualifying bullion generally must remain in the physical possession of a bank or an IRS-approved nonbank trustee, and that this custody rule applies when an IRA-owned limited liability company indirectly acquires bullion. A household should confirm the legal custodian, the storage provider, the account registration, the insurance arrangement, and how statements identify the metals. "Home storage" claims deserve independent tax and legal review before any transaction. Goldco does not offer tax or legal advice.

4. What the Dealer Premium and Spread Are

The spot price is the market price for immediate delivery of the metal. A dealer normally sells above spot through a premium and repurchases below the selling price. FINRA defines the difference between the dealer's buy and sell prices as the spread. The couple should request, in writing: current spot value; retail purchase price; dollar premium over spot; percentage premium over spot; same-day dealer repurchase price; percentage spread between purchase and repurchase prices; and sales commission or compensation. FINRA advises customers to ask what the dealer would pay if the metal had to be sold back the next day, which can make the immediate transaction cost easier to understand.

5. What Fees Apply

Possible Gold IRA costs can include account setup, annual administration, transaction charges, storage, insurance, wire fees, shipping, and account-closing charges. CFTC guidance states that self-directed IRA fees are typically higher than directed-IRA fees and recommends reviewing account statements to confirm that the expected bullion was purchased at a reasonable price. The fee review should calculate both the first-year cost and a five- or ten-year total under the household's intended holding period. The storage fee calculator and fee calculator can help organize those figures.

6. How the Repurchase Process Works

A dealer's repurchase program is a business policy, not an IRS feature of the IRA. The household should request the written process for obtaining a quote, selling metals, sending instructions through the custodian, paying transaction or shipping charges, and receiving cash back into the IRA. The document should also explain whether the dealer may decline a repurchase or change the quoted spread. The questions to ask before opening a Gold IRA provides a broader due-diligence list.

Red Flags in a Precious-Metals Pitch

Red flags do not prove that every proposed transaction is improper. They identify claims that deserve independent verification. FINRA and the CFTC specifically warn about unsolicited calls, emails, direct mail, late-night promotions, social-media pitches, inflated prices, large spreads, high fees, and sales messages that oversell safety. A couple can pause the process when a pitch includes:

- Pressure to make a decision during the call.

- A request to move most or all retirement assets.

- Predictions presented as certain outcomes.

- Claims that a political, religious, or media connection proves trustworthiness.

- Collectible or "exclusive" coins priced far above bullion value.

- Refusal to provide the spot value, premium, spread, or compensation in writing.

- Statements that the custodian has approved the economic merits of the purchase.

- Claims of secret tax treatment or special rollover rules.

- Resistance to involving a spouse, tax professional, or independent advisor.

- A buyback statement without written pricing terms.

The CFTC notes that precious-metals fraud promotions sometimes use political or religious affinity to build trust and may use economic anxiety to create pressure. The Gold IRA scam warning signs guide can support the review without labeling a company based on one sales conversation.

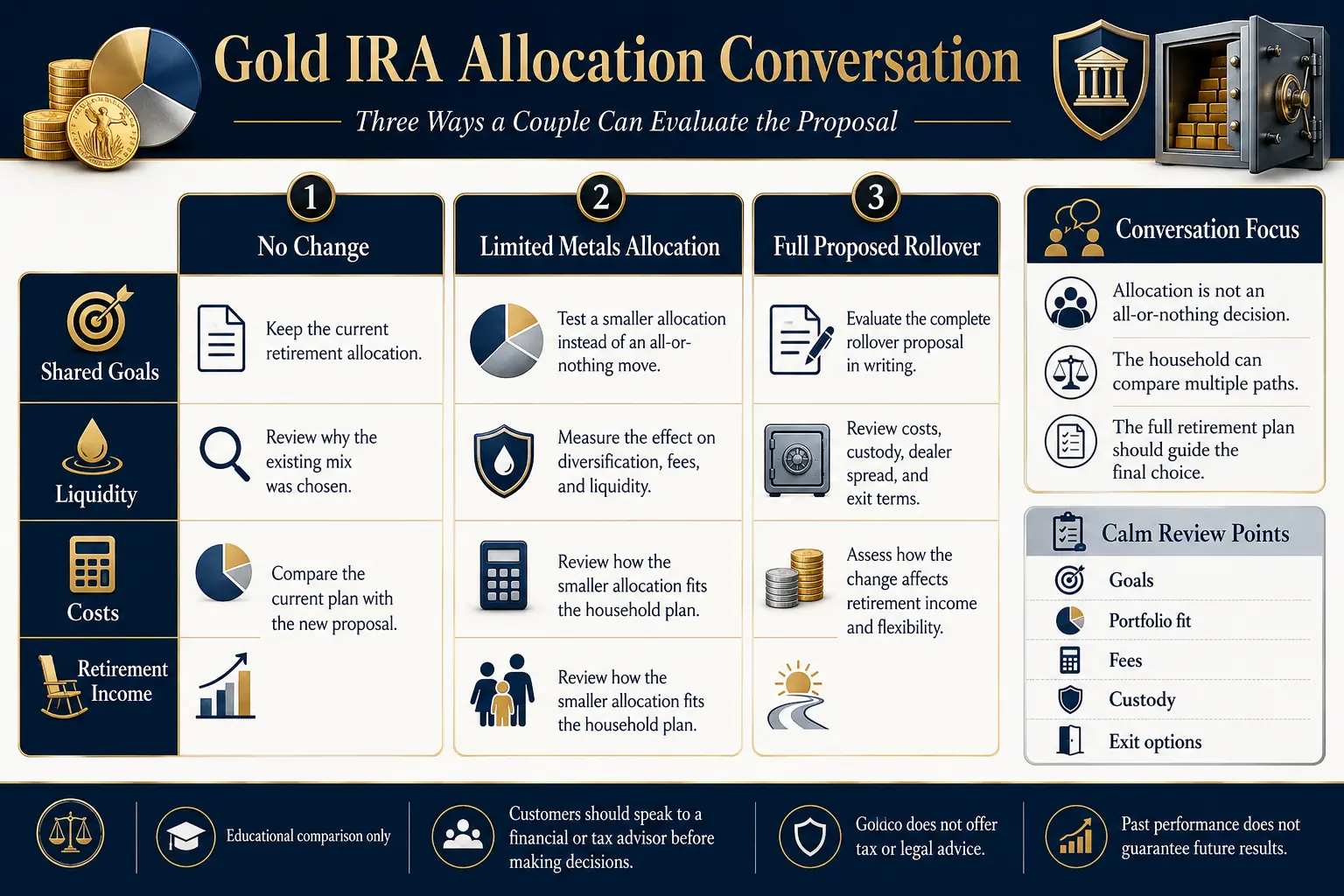

Frame the Choice as Allocation, Not All-or-Nothing

When a partner wants gold and silver IRA exposure, the most useful question is usually not whether gold belongs in the portfolio at all. It is how any proposed amount affects the full allocation. Investor.gov explains that asset allocation divides a portfolio among categories such as stocks, bonds, and cash, and lists precious metals among other asset categories that some portfolios may include, while noting that each category has specific risks. Diversification does not remove loss risk; its purpose is to reduce dependence on one asset, sector, or market outcome.

There Is No Universal Gold Percentage

Research does not establish one gold allocation that fits every household. A World Gold Council analysis of a hypothetical pension portfolio studied gold allocations from 2% to 10% and reported improved historical risk-adjusted results over its 1999-2019 sample; the World Gold Council represents the gold industry, and the result depends on its sample, assumptions, and rebalancing method. An academic paper reviewing strategic gold weights states that there is no consensus on the proportion of gold that should be included in a portfolio and that many different allocations can produce similar performance measures. Other research has found that gold did not consistently hedge stock markets during the 2007-2009 financial crisis or the COVID-19 period, showing that diversification behavior can change across market conditions.

These findings support using ranges as test scenarios rather than rules. A household could compare no gold exposure with small, moderate, and larger allocations, then review the effect on expected income, volatility, fees, liquidity, and concentration — without assuming the historical outcome will repeat. The how much gold should be owned in retirement guide and Gold IRA allocation backtest can help organize that comparison. Customers should speak to a financial or tax advisor before making allocation, rollover, or withdrawal decisions. Goldco does not offer tax or legal advice.

A Calm Joint-Decision Checklist

The following checklist can help when a spouse wants gold IRA exposure and the household needs a shared process.

- Agree on the goal. Both partners should write down the risk or goal the Gold IRA is expected to address.

- Set a no-pressure research period. No account transfer should begin while either partner still lacks the written documents needed for review.

- Map the whole retirement portfolio. Include both spouses' 401(k)s, IRAs, pensions, brokerage accounts, cash, real estate, and existing metals.

- Calculate the proposed percentage. Divide the dollar amount by total retirement assets, not only by the account being approached by the salesperson.

- Compare three alternatives. Keeping the current allocation, adding a smaller metals position, and making the full proposed transaction.

- Obtain written costs. Retail price, spot value, premium, spread, custodian fees, storage fees, transaction fees, and account-closing costs.

- Verify custody and eligibility. Confirm the exact custodian, depository, account title, and metal products before funds move.

- Review the exit. Calculate the amount that would be received if the metals were sold immediately and under several future price scenarios.

- Check the salesperson and firm. FINRA and CFTC guidance recommends checking relevant registration and disciplinary databases; retail physical-metal dealers may not be federally regulated in the same way, so state regulators, attorneys general, complaint records, ownership history, and written disclosures also matter.

- Record the decision rule. Agree in advance on what would lead to approval, a smaller allocation, more research, or no transaction.

A comparison of educational providers can begin with the best Gold IRA companies page. The Gold IRA quiz can help organize research priorities, but neither resource replaces independent tax or financial guidance.

When to Bring in a Neutral Professional

A neutral professional may be useful when the proposed transaction involves a large share of retirement assets, a workplace-plan rollover, complex taxes, an inherited account, required minimum distributions, a disagreement about retirement income, or a pitch that one partner feels unable to evaluate. The professional should understand the whole household plan rather than evaluating only the proposed metal purchase. The household should ask whether the professional is acting as a fiduciary, how the professional is paid, whether referral compensation exists, which alternatives will be reviewed, and whether the analysis will be provided in writing. A tax professional can review rollover and distribution consequences, an independent financial planner can examine allocation and retirement-income effects, and an attorney may be appropriate for unusual custody, LLC, estate, or beneficiary questions. Customers should speak to a financial or tax advisor before making decisions. Goldco does not offer tax or legal advice.

Frequently Asked Questions

What should happen when one spouse wants a Gold IRA and the other does not?

The household can pause the transaction, define the goal, collect written costs and account documents, and compare several allocation options. The decision should be based on the full retirement plan rather than one partner's confidence or one sales presentation.

Can one spouse move a retirement account without the other spouse?

Ownership and consent rules depend on the account type, plan terms, state law, beneficiary elections, and the transaction. A tax professional, plan administrator, or attorney should confirm the rules for the specific account. Goldco does not offer tax or legal advice.

Are all gold coins allowed in an IRA?

No. The IRS generally treats coins and metals as collectibles, with exceptions for certain coins and qualifying bullion held by a bank or approved nonbank trustee. The exact product should be verified with the custodian before purchase.

Can Gold IRA metals be stored at home?

IRS guidance states that qualifying bullion generally must be in the physical possession of a bank or an IRS-approved nonbank trustee. Claims involving home storage should receive independent tax and legal review.

What is the most important price question to ask a dealer?

The household should ask for the current spot value, total retail price, premium, spread, and the amount the dealer would pay to repurchase the metal immediately. FINRA recommends obtaining all fees, commissions, and agreed prices in writing.

Is there a standard gold allocation for retirement?

No universal percentage is supported by research. Published studies test different allocations under different assumptions, and academic research notes that no consensus exists. Allocation should be evaluated in the context of the household's total assets, income needs, time horizon, and risk tolerance.

Conclusion

When a spouse wants gold IRA exposure, the strongest household response is neither automatic agreement nor automatic rejection. A careful process identifies the concern behind the proposal, tests the numbers, confirms IRS eligibility and custody, measures premiums and spreads, reviews recurring fees, checks the repurchase process, and compares the proposed allocation with the full retirement plan. The couple can then make one shared decision: proceed, reduce the amount, keep researching, choose another diversification method, or decline the transaction. Gold may serve as one possible diversifier; it also has price volatility, transaction costs, custody requirements, and no contractual income. The evidence does not support treating it as a certain solution for inflation, market losses, or economic uncertainty. A written process protects the retirement plan and the relationship better than a decision made under pressure.

Sources

- National Bureau of Economic Research. Efficiency in Household Decision Making: Evidence from the Retirement Savings of U.S. Couples.

- National Bureau of Economic Research. Do Married Couples Coordinate Their Retirement Savings Efficiently?

- CFP Board. Financial FOMO: A Survey About Money and Relationships.

- Internal Revenue Service. Investments in Collectibles in Individually Directed Qualified Plan Accounts.

- Internal Revenue Service. Retirement Plans FAQs Regarding IRAs.

- Financial Industry Regulatory Authority. 10 Things to Ask Before Buying Physical Gold, Silver or Other Metals.

- Commodity Futures Trading Commission. 10 Things to Ask Before Buying Physical Gold, Silver, or Other Metals.

- Commodity Futures Trading Commission. The Truth Behind Gold and Silver IRA Scams.

- Commodity Futures Trading Commission. Gold Is No Safe Investment.

- Investor.gov. Beginners' Guide to Asset Allocation, Diversification, and Rebalancing.

- World Gold Council. Investing in Gold.

- Lucey, Peat & Vigne. What Is the Optimal Weight for Gold in a Portfolio?

- Drake, Pamela Peterson. The Gold-Stock Market Relationship During COVID-19. Finance Research Letters.

Article reviewed and edited by Daniel M. — editor, 401kToGoldIRA.org. Sourced to FINRA, CFTC, IRS, Investor.gov, and independent research; educational only, not tax or legal advice.