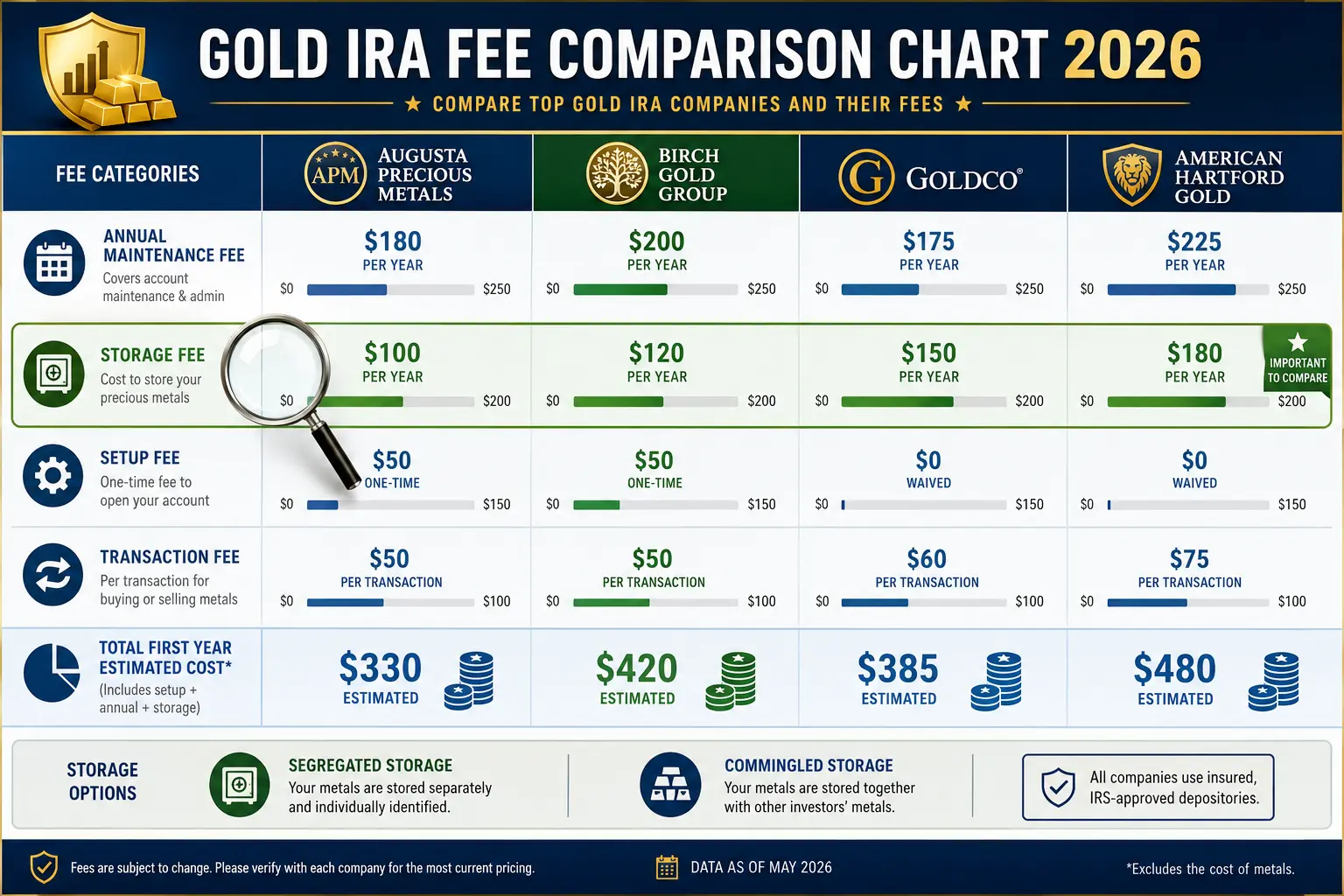

Educational only: This guide summarizes Investor.gov, FINRA, and Morningstar-reported material in general terms and is not financial, tax, or legal advice, and it is not market-timing guidance. Preparation cannot remove market risk. Customers should speak to a financial or tax advisor before making decisions. Goldco does not offer tax or legal advice. Past performance does not guarantee future results.

Quick Answer: How to Prepare a 401(k) for a Market Downturn

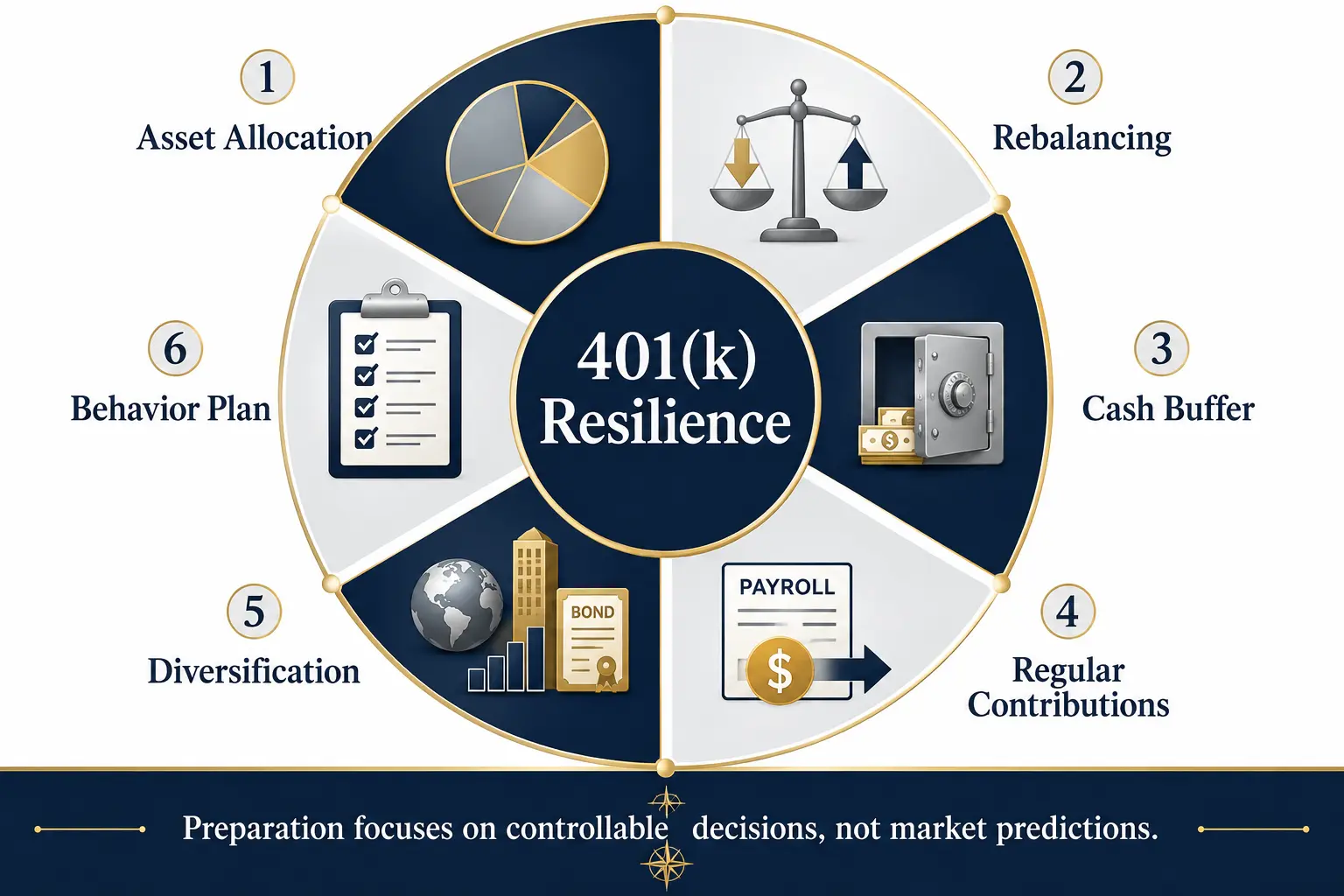

The most useful steps are under the account holder's control:

- Check the current allocation. The stock, bond, cash, and other holdings should match the saver's time horizon and risk tolerance.

- Set a rebalancing rule. A calendar date or allocation band can replace emotional decisions.

- Review the glide path. A saver approaching retirement may need less short-term volatility than a saver with several decades remaining.

- Build a cash buffer outside the growth portion of the portfolio. Near-retirees may use cash or short-term high-quality bonds for planned withdrawals.

- Keep contributing when employment and cash flow permit. Regular payroll contributions buy more fund shares when prices are lower and fewer when prices are higher.

- Diversify across and within asset classes. Diversification can reduce concentration risk, although it cannot prevent all losses.

- Treat gold as one optional diversifier. It is not a shield against every decline and should not replace a complete allocation.

- Write a no-panic plan. The plan should state what would justify a change and what would not.

The Gold vs. S&P 500 Calculator and Gold Allocation Backtest can support historical comparisons, but neither predicts the next downturn.

What History Shows About Downturns and Recoveries

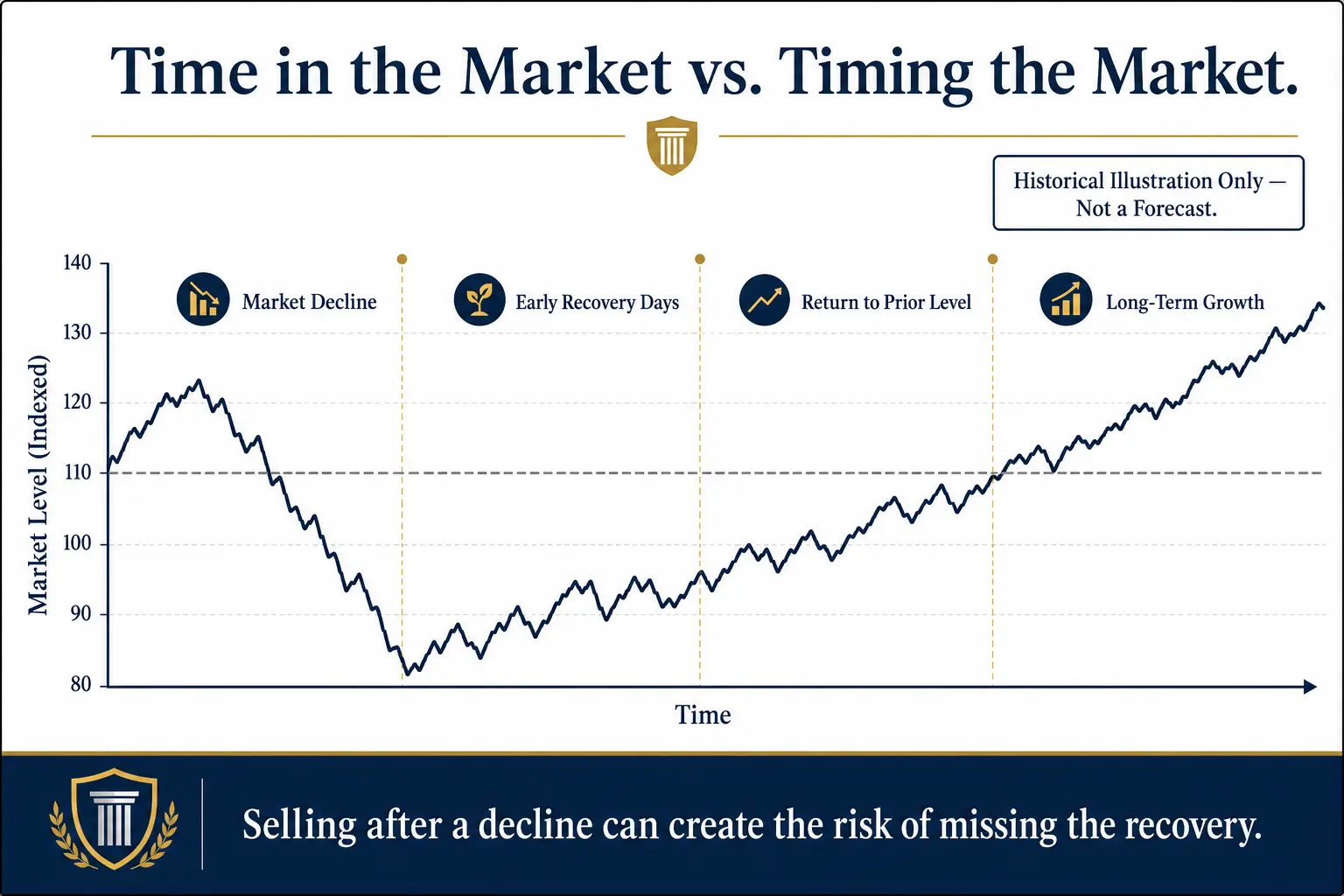

Market declines are normal parts of long-term investing, but their depth and recovery time vary. The Associated Press reported in March 2026 that the U.S. stock market had recovered from every prior steep decline and later reached new highs, while also noting that a recovery can take years and that no future recovery timetable is certain (Associated Press). That history does not mean every 401(k) behaves like the S&P 500 — a workplace account may hold U.S. stocks, international stocks, bonds, stable-value funds, cash, target-date funds, or company stock. A diversified account may fall less than an all-stock index, while a concentrated or stock-heavy account may fall more.

Investor.gov explains that diversification spreads money across investments and asset classes; it cannot ensure that a portfolio avoids losses when the market falls, but it may reduce the damage compared with a concentrated portfolio (Investor.gov). A downturn also does not create one correct response for every saver: a 32-year-old contributing through payroll has a different time horizon from a 64-year-old planning withdrawals — the younger saver may have decades for recovery and future contributions, while the near-retiree must also manage sequence-of-returns risk and cash needs. Historical recovery data should therefore be used for perspective, not for market timing. The useful lesson is that selling after a fall can turn a temporary decline into a realized loss and may leave the account outside the market when the recovery begins.

Get the Asset Allocation Right for the Saver's Age and Timeline

Asset allocation is the mix of stocks, bonds, cash, and other investments. Investor.gov states that the appropriate mix depends on the investment time horizon and risk tolerance — longer horizons may support more volatile assets, while shorter horizons may call for less volatility (Investor.gov). Age is a useful starting point, but it is not the only factor: two savers of the same age may have different pensions, Social Security expectations, emergency savings, debts, health needs, family obligations, and retirement dates. A practical review can divide the 401(k) into three jobs — growth (assets to support spending many years in the future), stability (assets to reduce overall volatility), and near-term liquidity (money expected to be needed soon after retirement). Stocks usually carry more short-term volatility than high-quality bonds or cash; reducing stock exposure can reduce some downside, but moving too far toward cash can weaken long-term growth and purchasing-power protection. The goal is not the lowest possible daily movement — it is a mix the saver can hold through a full cycle.

How a Glide Path Works

A glide path gradually changes the investment mix as retirement approaches. Investor.gov defines a target-date fund as a diversified fund that automatically shifts toward a more conservative mix as the target year approaches, with the fund manager handling allocation, diversification, and rebalancing (Investor.gov). A target-date fund can simplify a 401(k), but the year in the fund name does not prove that the risk level fits every saver — different funds can use different stock percentages, bond mixes, fees, and glide paths, so the current holdings should be reviewed rather than inferred from the date alone.

Rebalancing a 401(k)

Market gains and losses can push a portfolio away from its intended allocation. Investor.gov explains that rebalancing restores the original mix and can be done on a schedule or when an asset class moves beyond a preset band, and notes that rebalancing is generally intended to be relatively infrequent (Investor.gov). A simple policy might call for an annual review or a review when a major asset class moves several percentage points away from its target — the exact band is a planning choice, not a universal rule. Rebalancing before a downturn can prevent a long stock rally from quietly creating more risk than intended, and rebalancing during a downturn can direct new contributions toward the underweight asset class without requiring a large sale. Customers should speak to a financial or tax advisor before making decisions about 401(k) allocation, rebalancing, rollovers, or IRA assets. Goldco does not offer tax or legal advice.

Sequence-of-Returns Risk for Savers Near Retirement

Sequence-of-returns risk is most important when withdrawals are starting. A large decline early in retirement can damage portfolio longevity because money is leaving while asset prices are low. An account that is still receiving payroll contributions faces a different pattern — lower prices allow the same contribution to purchase more shares, whereas a retired account drawing money may need to sell more shares to produce the same cash amount. Morningstar's retirement guidance, reported by the Associated Press, describes a bucket approach that holds near-term spending in cash or high-quality bonds so stocks are less likely to be sold during a downturn, which can help new retirees manage sequence risk and fund spending while growth assets recover (Associated Press).

A separate 2026 Associated Press article based on Morningstar guidance described a cash cushion equal to roughly one to two years of expected portfolio withdrawals, not one to two years of total living expenses — Social Security, pensions, or other income may cover part of the household budget (Associated Press). That range is a framework, not a personal requirement: a larger cash buffer may reduce pressure to sell in a weak market, but too much cash may reduce long-term growth, and the right amount depends on outside income, spending flexibility, taxes, retirement timing, and the rest of the allocation. A pre-retirement plan can state which expenses will be paid from cash, which account will fund the first withdrawals, when the cash reserve will be refilled, which assets can be sold after gains, and which optional expenses can be delayed after a poor year. The goal is to avoid making the first withdrawal decision during a stressful market week.

The Biggest Self-Inflicted Risk: Panic-Selling and Missing the Recovery

Panic-selling often creates two decisions: when to leave and when to return. Both must be correct. The Associated Press reported that moving a 401(k) out of stocks during a steep decline can cause the saver to miss the recovery and later gains, and stressed that money needed soon should not depend on stock-market stability in the first place (Associated Press). Kiplinger reported J.P. Morgan Asset Management research covering 2004 through 2024, in which missing the ten strongest S&P 500 days cut the total return roughly in half compared with remaining invested; the article also noted that many strong days occurred during volatile periods, which makes a successful exit-and-reentry plan difficult (Kiplinger). The exact result depends on the index, period, taxes, fees, and assumptions, but the broader lesson is more stable: the recovery may begin before the news feels comfortable.

A written behavior policy can reduce reaction risk. It may include no allocation change based only on headlines, no full move to cash after a market decline, a waiting period before any major change, a scheduled review with a qualified professional, rebalancing only under the written rule, and a separate emergency fund for nonretirement needs. A saver who cannot tolerate the planned decline level may have an allocation problem, not a news problem — the better time to reduce structural risk is during a calm review, not after the account has already fallen.

Diversification and Low-Correlation Assets

Diversification is not the same as owning many funds — several funds may hold the same large companies or the same bond exposures. Investor.gov recommends spreading money across asset classes and within each class, and warns that narrowly focused mutual funds or ETFs may not provide broad diversification and that investors should check top holdings for overlap (Investor.gov). A 401(k) diversification review can examine U.S. and international stocks; large, mid-sized, and small companies; government and corporate bonds; short-, intermediate-, and longer-term bonds; cash or stable-value options; company-stock concentration; and any real assets or other diversifiers available in the plan. Low-correlation assets are holdings that do not always move in the same direction or by the same amount — correlations can change during stress, so no asset should be treated as a permanent offset. The Protect Retirement Purchasing Power guide explains how inflation, cash flow, and diversification interact over a long retirement.

Can Gold Protect Retirement From a Crash?

Gold cannot be counted on to protect a 401(k) from every crash. It can rise, fall, or remain flat while stocks decline, and it should not be described as a shield or a substitute for a complete asset-allocation plan. The World Gold Council, an industry organization, argues in its 2026 strategic-asset research that gold can complement stocks and bonds through diversification and liquidity; the same page states that diversification does not eliminate loss and that hypothetical portfolio outcomes do not assure future results (World Gold Council). The honest answer to "can gold protect retirement from a crash?" is therefore conditional: a modest position may reduce reliance on stocks and bonds in some periods, but it can also add price volatility, transaction costs, storage costs for physical metal, and tracking differences depending on the vehicle.

Many 401(k) plans do not offer physical gold. Available exposure may come through a precious-metals fund, a mining-stock fund, or another market-based option, and these are not equivalent — mining shares are operating companies and can behave differently from bullion, and a gold ETF and physical metal also have different custody, fee, tax, and liquidity features. A rollover to an IRA is not required simply because a plan has limited gold options; any rollover should be reviewed for plan fees, investment choices, creditor protections, tax treatment, and long-term objectives. Customers should speak to a financial or tax advisor before making decisions about precious-metals allocation, 401(k) rollovers, or IRA purchases. Goldco does not offer tax or legal advice. The Gold IRA Calculator, How Much Gold Should Be Held in Retirement guide, and Gold IRA vs. Gold ETF guide can support a proportionate comparison.

Keep Contributing: Dollar-Cost Averaging Through Volatility

Regular 401(k) payroll contributions are a form of dollar-cost averaging: the same dollar contribution purchases more fund shares when prices are lower and fewer shares when prices are higher. FINRA explains that dollar-cost averaging means investing equal portions at regular intervals, which can reduce the pressure to choose a perfect entry date but does not assure a profit or protect against loss in a falling market (FINRA). For an employed saver with stable cash flow, stopping contributions after a decline can remove the chance to purchase at lower prices, and may reduce or forfeit an employer match if the plan requires current contributions. No assumption should be made about a specific employer match — the plan's summary plan description and benefits portal should be checked for the formula, vesting rules, contribution limits, and eligibility terms.

Continuing contributions does not mean increasing risk without review: new payroll money can be directed according to the target allocation, and a saver who discovers excessive stock exposure may adjust future contributions and rebalance under the written policy rather than moving everything at once because of a headline. Dollar-cost averaging also should not be confused with holding a large lump sum in cash and slowly investing it — FINRA notes that the comparison changes when all money is already available, because delaying investment can create opportunity costs (FINRA).

A Pre-Downturn 401(k) Preparedness Checklist

- Inventory every holding. List each fund, its asset class, expense ratio, top holdings, and percentage of the account. Several funds with different names may hold similar securities.

- Write the target allocation. Set target percentages for stocks, bonds, cash, and any other available assets, reflecting the retirement date, withdrawal needs, other savings, and risk tolerance.

- Compare the current mix with the target. A long bull market may have raised stock exposure above the intended level; rebalancing can restore the planned risk level (Investor.gov).

- Review the target-date fund. Check the fund's current stock percentage, bond mix, fees, and glide path. A target year is not a complete risk description (Investor.gov).

- Address company-stock concentration. Employer stock can link employment income and retirement savings to the same company; review the account for concentration rather than assuming the employer stock is diversified.

- Build the appropriate cash buffer. Near-retirees can decide how planned withdrawals will be funded if stocks fall near the retirement date. Morningstar's bucket framework commonly starts with one to two years of expected portfolio withdrawals in cash, but the amount should be customized (Associated Press).

- Confirm contribution and match rules. Record the contribution percentage, employer match formula, vesting schedule, and automatic escalation setting — these details come from the individual plan.

- Set the rebalancing trigger. Choose an annual review date, a percentage band, or both. Avoid daily monitoring.

- Write the panic-selling rule. State that market headlines alone do not trigger a full move to cash, and identify the life changes that would justify an allocation review, such as a changed retirement date, job loss, major health event, or revised spending need.

- Review beneficiaries and account access. Confirm beneficiary designations, contact information, passwords, and the location of plan documents. These steps do not change market risk, but they improve account readiness.

- Stress-test the plan. Model a stock decline, a slower recovery, higher inflation, and an earlier retirement. The result should show whether the saver needs a different allocation, larger cash reserve, lower planned spending, or a longer work timeline.

- Schedule the next review. A resilient plan is maintained; the next review date should be set before volatility arrives.

Frequently Asked Questions

Should a 401(k) be moved to cash before a market crash?

A future market peak cannot be known in advance. Moving to cash requires a correct exit and a correct reentry. A calmer approach is to hold an age-appropriate allocation, keep near-term money out of volatile assets, and rebalance under a written rule.

What usually happens to a 401(k) during a recession?

The result depends on the holdings. A stock-heavy account may fall sharply, while bonds, cash, or stable-value options may reduce the decline. Diversification cannot prevent every loss.

How should asset allocation change near retirement?

A shorter time horizon may support a less volatile mix, especially for money needed soon. Investor.gov states that time horizon and risk tolerance are central to allocation decisions, while target-date funds generally become more conservative near their target year.

Does gold protect against a market crash?

Not reliably in every downturn. Gold may add diversification, but it can also decline and should not replace stocks, bonds, cash, and a withdrawal plan. No universal gold percentage fits every saver.

Should 401(k) contributions continue during a downturn?

Regular payroll contributions purchase more shares when prices are lower and fewer when prices are higher. FINRA notes that this dollar-cost-averaging method can support discipline but does not assure a profit or prevent loss.

How much cash should a near-retiree hold?

There is no universal amount. Morningstar guidance reported by the Associated Press describes one to two years of expected portfolio withdrawals as a common bucket starting point, but outside income, spending, taxes, and risk capacity can change the answer.

Conclusion

Preparing a 401(k) for the next market crash is not about predicting the date or escaping every decline. The strongest plan aligns allocation with time horizon, rebalances by rule, limits concentration, protects near-term spending, continues disciplined contributions, and keeps diversification proportionate. Gold may play a supporting role, but it is not a shield and should not carry the full burden of retirement protection. The saver's greatest advantage is a plan written before the market becomes stressful — that plan can replace fear-driven decisions with a short list of actions that remain useful in both calm and volatile markets.

Sources

- Associated Press. Markets have recovered from every prior steep decline (2026).

- Associated Press (Morningstar guidance). Bucket approach and sequence-of-returns risk.

- Associated Press (Morningstar guidance). Cash cushion for near-retirees.

- FINRA. Three Things to Know About Dollar-Cost Averaging.

- Investor.gov. Asset Allocation.

- Investor.gov. Target-Date Fund.

- Investor.gov. Diversify Your Investments.

- Kiplinger. How to Keep Your 401(k) on Track Amid Dire News (J.P. Morgan data).

- World Gold Council. The Relevance of Gold as a Strategic Asset (2026).

Article reviewed and edited by Daniel M. — editor, 401kToGoldIRA.org. A neutral downturn-preparedness guide sourced to Investor.gov, FINRA, Morningstar (via the Associated Press), Kiplinger, and the World Gold Council; educational only, not financial, tax, or legal advice.