Educational only: This article summarizes FINRA, CFTC, IRS, and published custodian fee schedules in general terms. It is not financial, tax, or legal advice. Fee figures are provider-specific observations or sourced ranges, not industry averages. Customers should speak to a financial or tax advisor before making decisions. Goldco does not offer tax or legal advice. Past performance does not guarantee future results.

The most hidden Gold IRA cost is the dealer markup over spot — often ~1%–10% on standard bullion but reaching 100%–300%+ on some numismatic or "exclusive" coins — because it is embedded in the purchase price rather than billed as a separate fee.

Source: CFTC — Precious Metals Fraud. Markup ranges are typical reported ranges, not fixed prices; confirm every figure against a written quote.

Key takeaways

- The biggest hidden cost is usually the embedded dealer markup, not the visible annual fees — it is built into the purchase price and can exceed years of custodian charges.

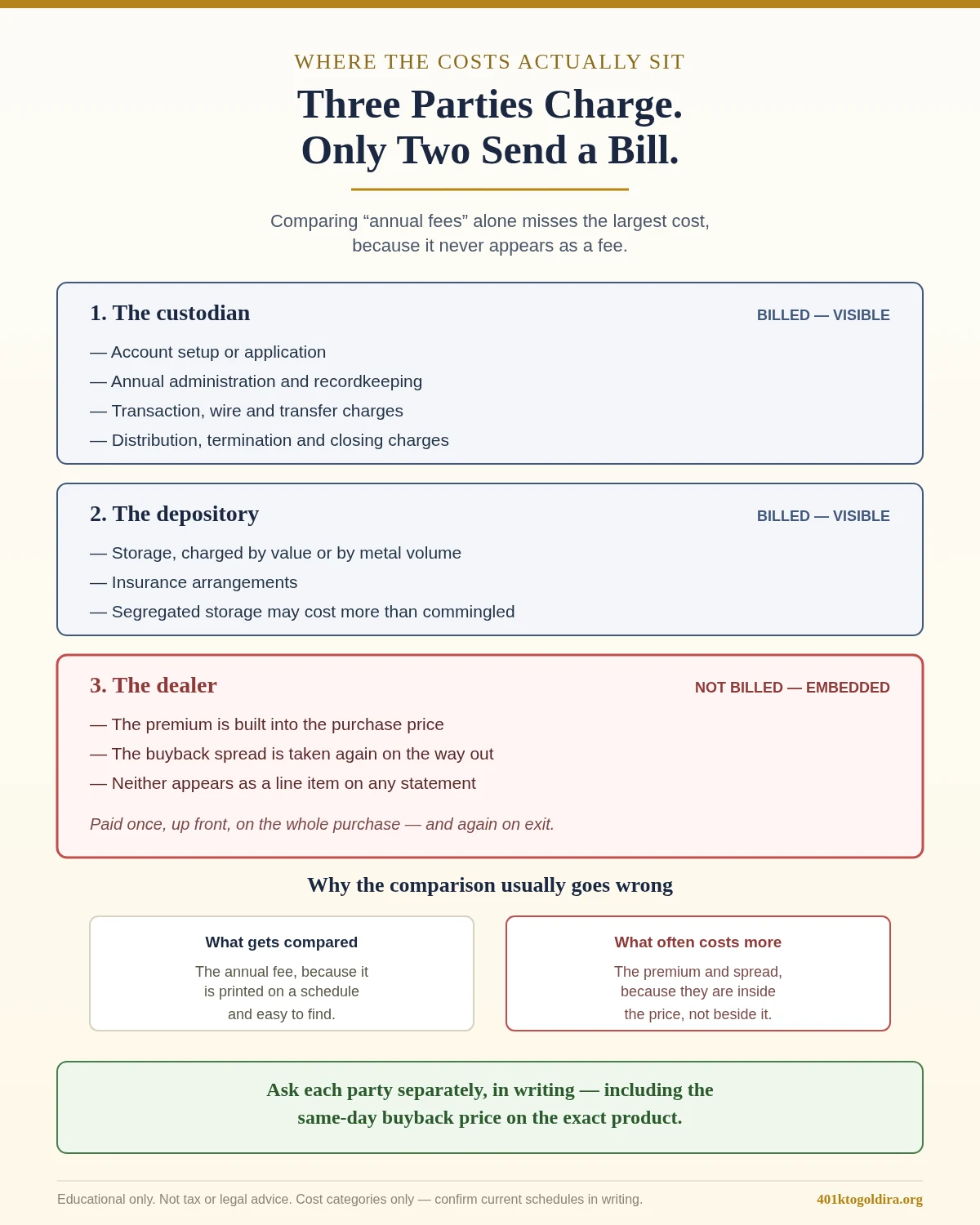

- Fees come from separate parties: dealer (markup/spread), custodian (setup + annual + wire/transaction), and depository (storage + insurance).

- Watch for value-based storage that scales with the account (e.g. a percentage of asset value above a threshold), which can grow silently as metal appreciates.

- A buyback spread — the gap between the sell price and the same-day repurchase quote — is a real round-trip cost that a headline "low fee" claim hides.

- There is no reliable public database of Gold IRA fees; every figure must be confirmed in a written, dated quote for the specific products and account.

No reliable public database establishes one universal Gold IRA fee, dealer markup, or buyback spread. Providers use different products, account sizes, storage methods, and pricing models. A careful comparison therefore needs written figures for the exact account and metal being considered.

Quick Answer: Where Hidden Gold IRA Costs Actually Live

The most visible expenses are usually the easiest to compare: the account establishment fee, the annual custodian or recordkeeping fee, the depository storage and insurance charge, and wire, check, shipping, distribution, and termination fees. The less visible costs often sit inside the transaction: the dealer premium above spot, a sales commission included in the metal price, a larger markup on proof, graded, or specialty coins, the difference between the purchase price and the dealer's immediate buyback price, and percentage-based administration or storage charges that rise with account value.

FINRA states that a dealer sells metal above spot and repurchases it below spot; the difference is the spread, and FINRA advises obtaining all fees, commissions, costs, and the agreed retail price in writing before transferring money. The dealer markup can be the largest and least obvious cost in a specific transaction — but no defensible public dataset proves it is the largest cost in every Gold IRA, so the safest framing is "potentially the largest embedded cost," not a universal claim. The Gold IRA break-even calculator combines the markup with setup, storage, custodian, and buyback-spread costs to estimate how much the metal must appreciate before an account recovers them. Customers should speak to a financial or tax advisor before making decisions involving retirement accounts, rollovers, withdrawals, or taxes. Goldco does not offer tax or legal advice.

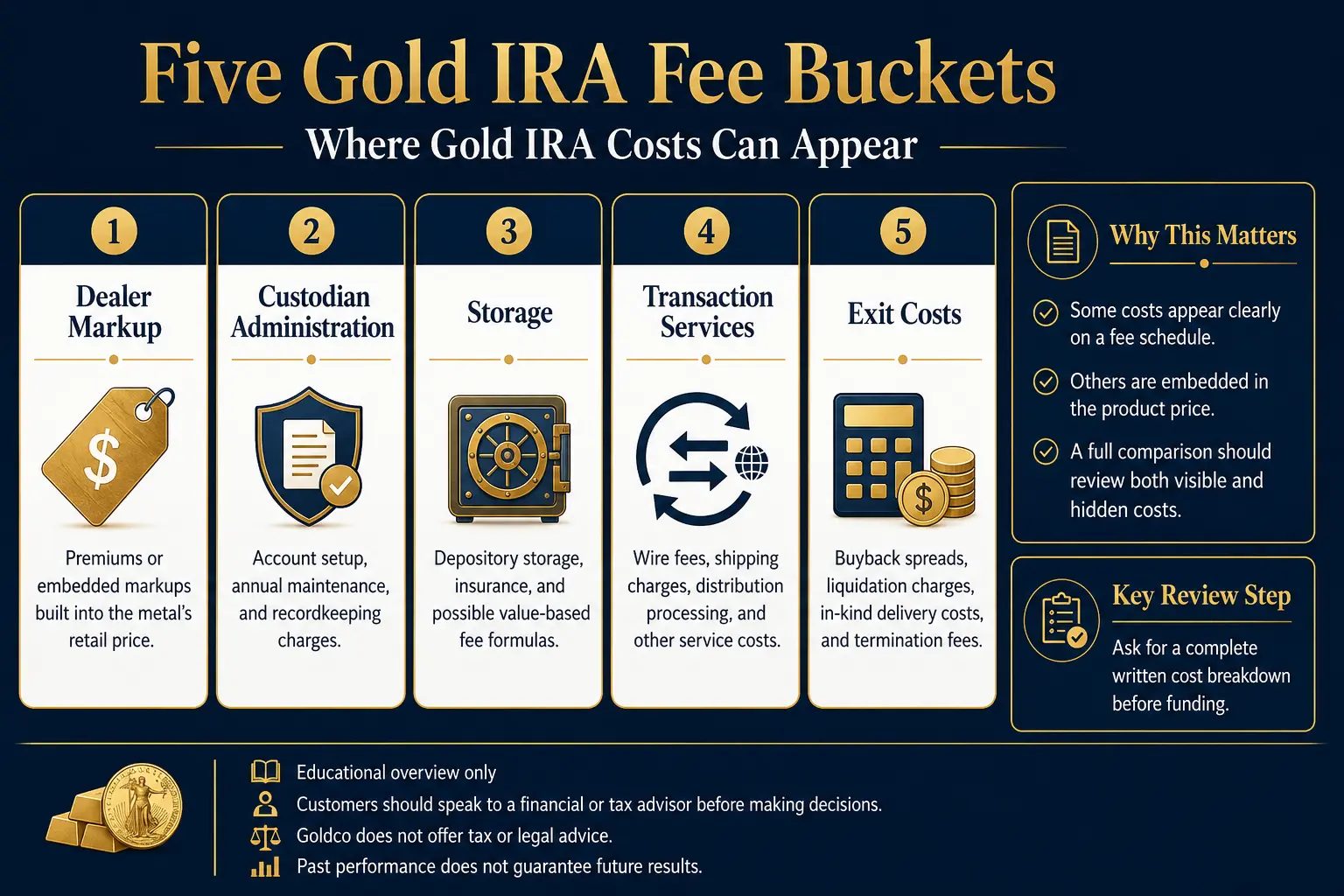

How to Spot Hidden Gold IRA Fees Across Five Cost Buckets

A Gold IRA total cost of ownership is easier to understand when charges are placed into five buckets.

| Cost bucket | Common examples | Usually visible? | Main verification step |

|---|---|---|---|

| Dealer pricing | Premium, markup, commission, product substitution | Often embedded | Compare metal value with the written retail price |

| Custodian administration | Establishment, annual recordkeeping, maintenance | Usually listed | Read the current custodian fee schedule |

| Depository storage | Commingled, segregated, insurance, value-based | Listed, but formulas vary | Ask for the exact annual charge at the expected balance |

| Transaction services | Wire, check, shipping, rush, distribution, re-registration | Often scattered across forms | Request a complete transaction and exit schedule |

| Exit costs | Buyback spread, liquidation shipping, in-kind delivery, termination | Frequently overlooked | Get an immediate buyback quote and closing-cost estimate |

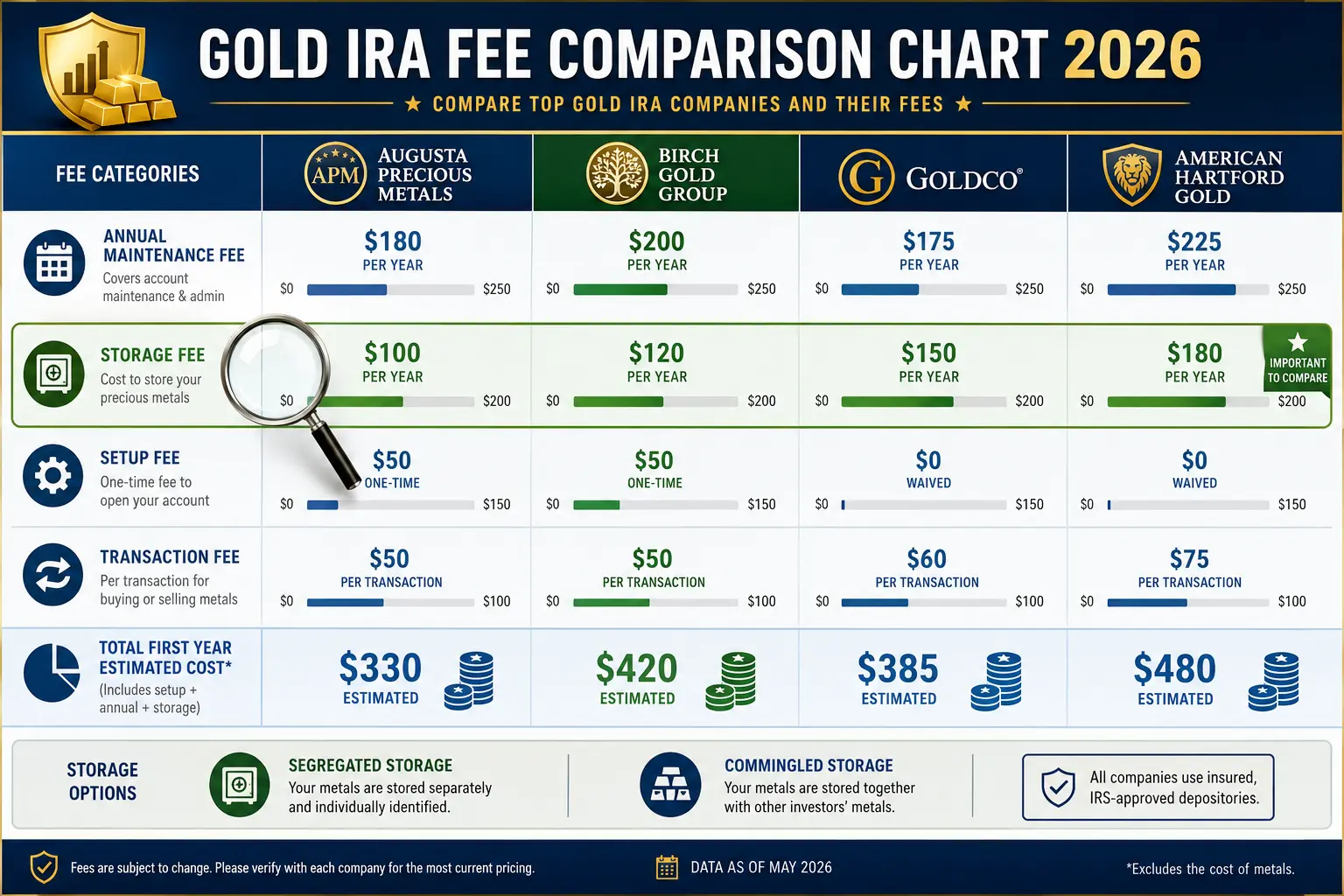

These categories can overlap. A custodian can charge no purchase or sale fee while the depository charges shipping. A dealer can advertise no commission while earning money through the premium. The goal is not to find a provider with no costs — physical metals require dealers, custody, administration, storage, and eventual liquidation. The goal is to identify where each party earns money and calculate the complete cost before funding. The Gold IRA fees benchmark for 2026 provides a broader educational comparison of published fee schedules.

The Biggest Hidden Cost: Dealer Markup Embedded in the Price

The dealer markup hidden inside a quote is different from a line-item account fee. Spot is the cash-market reference price for immediate delivery, usually per troy ounce; the metal value in a product can be estimated by multiplying its fine-metal weight by the current spot price. The CFTC publishes the premium formula: premium % = (sales price − spot value) ÷ spot value × 100, and recommends converting spot to the same weight as the product and comparing that value with the quoted sales price. A transparent quote should identify the exact product, quantity, fine-metal weight per item, the spot price and its timestamp, the total spot/melt value, the total retail price, the dollar premium, and the premium percentage. Without those details, the buyer sees a final number but cannot tell how much represents metal versus dealer compensation.

"No commission" does not mean no markup

A dealer can truthfully state that no separate commission appears on the invoice while earning revenue through the difference between wholesale cost and retail price. FINRA recommends asking how the salesperson is paid and whether compensation is included in the spread. The useful questions are: what is the retail price, the current spot value, the premium percentage, what the dealer would pay to buy the same product back immediately, and whether the salesperson receives higher compensation for one product than another.

Proof and specialty coin markups

A proof-coin markup can differ sharply from a common bullion premium. GoldStar Trust's precious-metals disclosure states that dealer markups, premiums, or commissions have generally been greater for proof coins than for bullion, and that the spot values shown on account statements do not include dealer markups, premiums, discounts, or commissions. FINRA describes "semi-numismatic" as a made-up industry term with no special meaning and notes that products sold as collectible may be less liquid than bullion. No defensible public source establishes one universal proof-coin markup — any numeric claim should identify the dealer, product, quote date, and comparison method. A careful comparison asks for two quotes at the same time: a common bullion coin or recognized bar, and the proof/graded/specialty product being proposed, both showing metal weight, spot value, retail premium, and same-day buyback price. The dealer markup data can organize product-level comparisons.

Custodian Fees: Setup, Maintenance, and Recordkeeping

Custodian fees are usually more transparent because regulated account administration requires written agreements and schedules. Even so, the pricing model can be misunderstood.

GoldStar Trust (January 2026 schedule): $50 establishment; $90 annual maintenance; $125 annual commingled storage; $225 minimum annual segregated storage (no stated maximum); no custodian fee for buying, selling, or exchanging metals; $50 wire; $75 partial transfer or in-kind distribution; $150 full termination; $10 plus shipping on liquidations and in-kind distributions. The same schedule adds $1.80 per $1,000 of precious-metals value above $125,000 beside the segregated-storage entry. These are current provider-specific observations, not an industry average.

The Entrust Group (revised January 9, 2026): $50 establishment; $219 annual recordkeeping for one asset below $50,000; $329 for two or more assets below $50,000; the same base plus 0.17% of total non-cash asset value above $50,000; a $2,299 annual recordkeeping cap; $0 for a precious-metals purchase, sale, or exchange (storage and shipping can still apply); $30 wire; $250 account termination processing. Entrust's own example: two assets worth $150,000 create a $499 annual recordkeeping fee ($329 plus 0.17% of the $100,000 above the threshold). These schedules show why a "low annual fee" cannot be compared without the account size and number of assets.

Setup-fee waivers and promotions

A dealer may offer to reimburse or cover a custodian or storage fee. That payment does not make the expense disappear — the reimbursement may be funded by the dealer's margin. FINRA advises asking how a business earns money when it appears to offer large gifts or free metals. The correct comparison records the published custodian fee, the amount the customer pays, the amount the dealer reimburses, the metal premium charged, the buyback price, the waiver duration, and the fees due after the promotional period.

Gold IRA Storage Fees and Sliding-Scale Charges

Storage fees can be flat, tiered, or value-based, and the label alone does not show the future cost. Commingled storage generally places similar assets from multiple accounts in a custodian-controlled area; segregated storage identifies and separates the account's specific metals and often costs more (GoldStar's January 2026 schedule lists $125 commingled vs a $225 minimum segregated, plus the value-based charge over $125,000). A comparison should verify whether silver can be segregated, whether the quoted fee covers every metal type, whether the charge is per account/asset/depository/year, whether the first and last partial years are billed in full, whether insurance is included, and whether shipping is separate.

A sliding-scale fee increases with account value and may appear under recordkeeping, administration, asset holding, or storage rather than under the word "percentage." Entrust's 0.17% charge above $50,000 is a clear value-based recordkeeping example; GoldStar's schedule includes a value-based precious-metals charge above $125,000 in its storage section. A percentage that looks small can become significant as the balance grows, so the comparison should calculate at several balances — opening, after five years, after ten years, and a higher-value scenario after a major price increase. The fee calculator can help compare flat and percentage-based structures over time.

Gold IRA Spread Cost and the Buyback Price

The spread cost is the round-trip difference between buying and selling. FINRA states that dealers sell above spot and buy below spot, each dealer sets its own spread, and the greater the spread and other costs, the more the spot price must rise before break-even. A 2021 CFTC advisory stated that physical precious-metals spreads can often be 10% or more — that is broad regulator guidance about physical precious metals, not a current market-wide average for every Gold IRA dealer or product, and it should not be converted into a universal Gold IRA spread. FINRA's separate reference to fraudulent spreads above 300% is an enforcement warning, not a normal-market benchmark.

The same-day buyback test

Before funding, the dealer should provide the exact retail purchase price, the current spot value, the exact amount the dealer would pay to repurchase the product that day, the dollar difference, the percentage difference, and any condition, packaging, minimum-quantity, or shipping requirements. This does not predict a future quote — it measures the entry and immediate exit gap at one point in time. A vague "buyback program" is not a price; a repurchase policy should explain how the bid is calculated and whether the company can decline a purchase. A dealer may charge no separately labeled buyback fee while offering a lower bid — the economic cost is still present in the spread. Model the round-trip on the quote checklist.

How to Get Every Fee in Writing Before Funding

FINRA states that unavailable written fees are a red flag, and recommends obtaining all fees, costs, commissions, and the agreed retail price before signing or transferring money. A complete written fee schedule should be assembled from three parties:

- Dealer document: product and quantity, fine-metal weight, spot price and timestamp, spot/melt value, retail price, premium in dollars and percentage, sales compensation, same-day buyback amount, cancellation terms, promotional reimbursement terms.

- Custodian document: establishment, annual maintenance/recordkeeping, percentage or asset-value charge, transaction and wire fees, distribution charges, statement/research charges, account termination, late-fee policy.

- Depository document: commingled or segregated method, annual base fee, percentage or tier formula, insurance treatment, shipping and handling, partial-year policy, in-kind delivery charges, fee-change process.

Customers should speak to a financial or tax advisor before making decisions involving an IRA, rollover, distribution, or tax treatment. Goldco does not offer tax or legal advice.

Comparing Gold IRA Total Cost of Ownership

The lowest opening fee does not always produce the lowest long-term cost. A fair comparison uses the same assumptions for every provider: same funding amount, product type and fine-metal weight, spot price and quote time, storage method, holding period, number of purchases, ending account value, and liquidation route. A useful educational formula is: total cost of ownership = dealer premium + custodian fees + storage fees + transaction costs + exit spread and closing costs, tested over one, five, and ten years. The calculation should not assume metal prices rise — it should first measure costs independently, then test how changing account value affects percentage-based fees. Some costs cannot be known in advance (future spot price, future buyback bid, future shipping, future fee changes, future balance, product condition); these should be labeled unknown, not filled with invented numbers. The best Gold IRA companies page is a starting point for research, but the current written quote should control the comparison.

Gold IRA Fee Red Flags

- No product-level price breakdown. The quote shows a total but omits metal weight, spot value, premium, or product-level price.

- The custodian fee is disclosed but the dealer price is not. A salesperson focuses on a modest annual account charge while avoiding the embedded markup.

- "No fees" without a revenue explanation. The company claims no commissions, setup, or storage but does not explain the retail premium or how promotions are funded.

- Proof or specialty products replace the requested bullion without a side-by-side markup and buyback comparison.

- Only a future buyback promise is provided — no same-day written buyback price for the exact product.

- Storage is described as flat without the formula (tiers, percentage charges, or separate depository costs hidden underneath).

- Exit fees are missing from the opening packet (wire, shipping, liquidation, in-kind distribution, re-registration, termination).

- Fees are spread across multiple documents with no consolidated total.

- Pressure replaces documentation. FINRA's March 2026 guidance warns against immediate-decision pressure and advises a full written accounting of account-opening, commission, storage, management, and other fees. More red flags are in the markup data.

Frequently Asked Questions

What is the most common hidden Gold IRA fee?

The dealer premium is one of the most important embedded costs because it may be included in the product price rather than shown as a separate fee. No reliable public dataset proves that it is always the largest cost.

How can a Gold IRA markup be calculated?

The metal's spot value can be compared with the retail sales price. The CFTC formula is the sales price minus spot value, divided by spot value, multiplied by 100.

Are Gold IRA custodian fees always flat?

No. Current published schedules include flat, tiered, and value-based models. Entrust adds 0.17% of non-cash asset value above $50,000, while GoldStar publishes a value-based precious-metals charge above $125,000 in its storage schedule.

Are proof-coin markups higher than bullion markups?

GoldStar's disclosure states that dealer markups, premiums, or commissions have generally been greater for proof coins than for bullion. No universal numeric difference can be verified for every dealer and product.

What is a Gold IRA buyback spread?

It is the difference between the dealer's retail selling price and repurchase price. The spread can exist even when the dealer charges no separately labeled buyback fee.

Which fees should be requested before funding?

The written package should include the product premium, sales compensation, custodian setup and annual fees, storage formula, wire and transaction charges, shipping, liquidation, in-kind distribution, buyback terms, and termination fee.

Update Log

- 2026: Initial publication. Sourced to FINRA and CFTC investor guidance, IRS custody/collectibles rules, and the published GoldStar Trust (January 2026) and Entrust Group (January 9, 2026) fee schedules. Fee figures are provider-specific and change without notice — reverify against the current schedule before relying on any figure.

Sources

- FINRA. 10 Things to Ask Before Buying Physical Gold, Silver or Other Metals.

- FINRA. Physical Precious Metals.

- Commodity Futures Trading Commission. CustomerAdvisory COVID19PreciousMetals.

- Commodity Futures Trading Commission. 8373 21.

- Commodity Futures Trading Commission. Precious Metals Fraud.

- The Entrust Group. Master Account Fee Schedule Jan 26.

- GoldStar Trust. Fee%20Schedule Altmetrics.

- GoldStar Trust. Precious metals iras investment disclosure.

- GoldStar Trust. Precious metals.

- Internal Revenue Service. Retirement Plans FAQs Regarding IRAs.

- Internal Revenue Service. Investments in Collectibles in IRA Accounts.

- Internal Revenue Service. Approved Nonbank Trustees and Custodians.

Article reviewed and edited by Daniel M. — editor, 401kToGoldIRA.org. Sourced to FINRA, the CFTC, the IRS, and published custodian schedules; educational only, not tax or legal advice.