Educational only: This article summarizes IRS rules, a public court decision, and federal regulator guidance in general terms. It is not financial, tax, or legal advice. Precious metals can be volatile, and federal regulators warn against sales pitches that present metals as certain protection or rely on fear and pressure. Customers should speak to a financial or tax advisor before making decisions. Goldco does not offer tax or legal advice. Past performance does not guarantee future results.

The central preparedness question is not whether home bullion or a Gold IRA is universally superior. The better question is which job each asset is expected to perform. Personally held bullion can provide direct possession outside the retirement system. A Gold IRA can provide a tax-advantaged retirement wrapper, formal recordkeeping, and qualified third-party custody. Those are different functions, and combining them into one claim creates legal and planning mistakes.

Quick Answer: Where a Gold IRA Fits a Preparedness Mindset

A preparedness plan often separates near-term access from long-term retirement planning. Under that approach, personally held cash and lawful non-IRA property serve immediate needs, while retirement accounts remain focused on later-life goals. A Gold IRA may fit the second category: it can hold certain qualifying coins and bullion through a trustee or custodian, and the account keeps the tax character of a traditional or Roth IRA.

That structure does not provide direct household access to the metal while it remains inside the IRA. Federal law generally treats gold and other bullion as collectibles, with exceptions for specified coins and qualifying bullion held in the physical possession of a bank or approved nonbank trustee. The IRS states that the possession rule also applies when an IRA-owned limited liability company buys the bullion indirectly. So a balanced prepper gold investing plan can treat a Gold IRA as a retirement-diversification tool rather than an emergency cache. Customers should speak to a financial or tax advisor before making decisions involving taxes, rollovers, withdrawals, or storage. Goldco does not offer tax or legal advice.

Two Different Preparedness Jobs

Precious metals for preppers are often discussed as though every ounce serves the same purpose. In practice, direct-access property and retirement property have different rules. A tax-advantaged framework can divide the issue into two buckets:

- Direct-access assets: personally controlled cash, bank deposits, and lawful non-IRA property that can be reached without an IRA distribution process.

- Retirement assets: accounts designed for long-term savings, subject to contribution, custody, rollover, withdrawal, and tax rules.

A Gold IRA belongs in the second bucket. The IRA owns the metals for the benefit of the account holder, and a qualified custodian or trustee administers the account. The Tax Court has emphasized that independent custody and recordkeeping are central parts of the IRA structure. This distinction reduces category errors: direct possession can support access and control; IRA custody can support retirement tax treatment. One asset does not need to perform both roles.

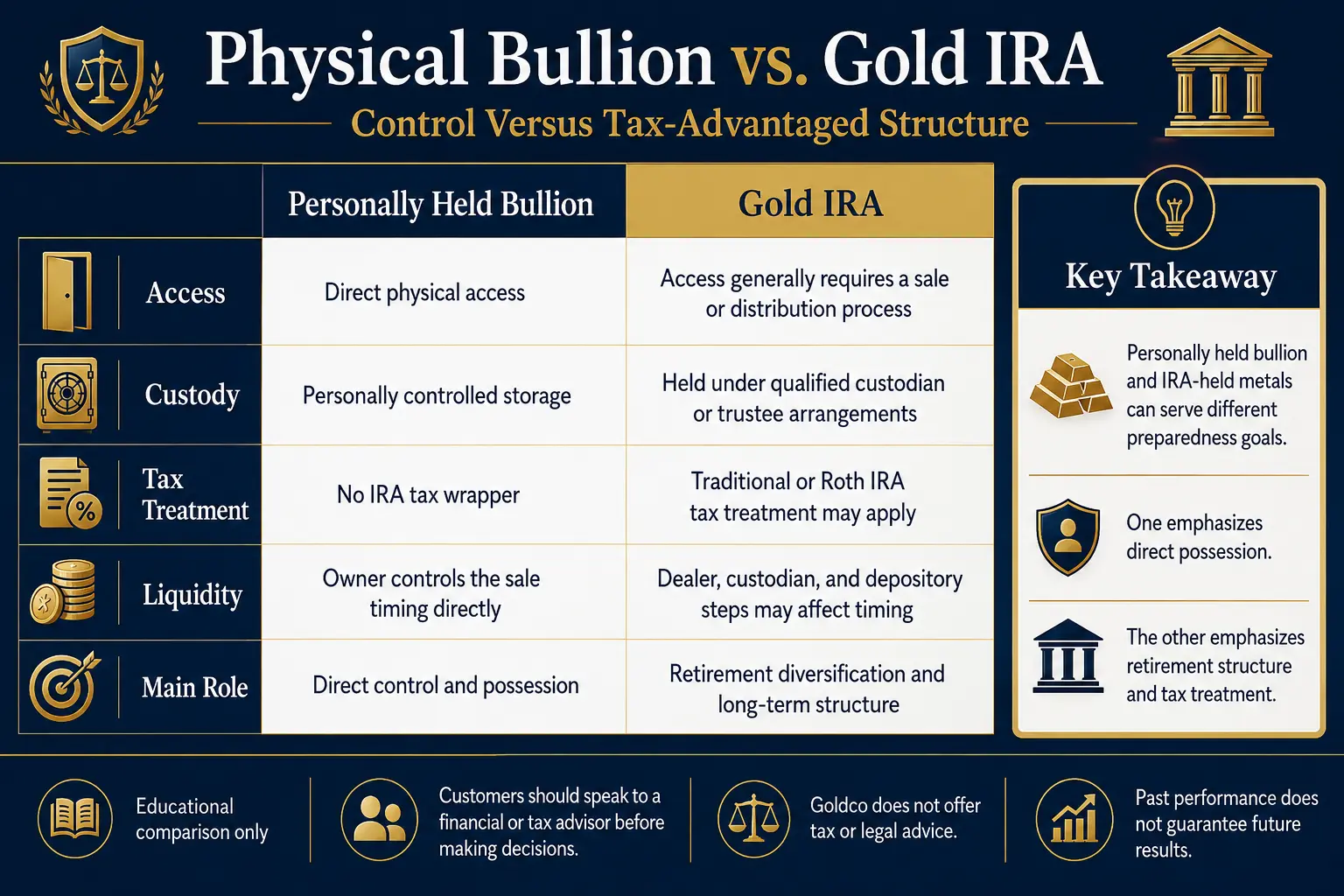

Physical Bullion vs a Gold IRA: Control Versus Tax Advantage

The main tradeoff is straightforward. Home-stored bullion provides direct control, while a Gold IRA provides an IRA structure. Personally held bullion offers direct possession, direct physical access, an owner-chosen storage and sale process, and no IRA tax wrapper. A Gold IRA offers qualified trustee or custodian possession, traditional or Roth IRA tax rules, and long-term retirement diversification, but access requires a sale or reportable in-kind distribution and custodian fees may apply.

Personally held bullion is not sheltered merely because it is gold. The IRS treats long-term gains from metals such as gold, silver, and platinum bullion as collectibles gain, subject to a maximum federal capital-gain rate of 28%; the actual result depends on holding period, taxable income, basis, losses, and other circumstances. Inside a traditional IRA, gains and losses are not reported on each internal purchase or sale — traditional IRA distributions are generally taxed when received, except for properly tracked after-tax basis, while qualified Roth distributions may be tax-free. The IRA treatment is not automatically more favorable in every case: traditional distributions can create ordinary taxable income, Roth qualification rules matter, early distributions can face an additional tax, and custodial costs can reduce returns. Customers should speak to a financial or tax advisor before making decisions involving tax treatment, withdrawals, or account structure. Goldco does not offer tax or legal advice.

Why the Gold IRA Home-Storage Myth Is a Legal Trap

The gold IRA home storage myth usually starts with an attractive claim: an IRA can own an LLC, the LLC can buy coins, and the account holder can keep those coins at home while the assets remain inside the IRA. That claim leaves out the federal custody rules. Internal Revenue Code Section 408 requires an IRA trustee to be a bank or another person approved to administer IRA assets. The statute excludes certain coins and qualifying bullion from the collectibles restriction, but qualifying bullion must be in the physical possession of a trustee described in Section 408(a). The IRS states the same rule applies to an indirect purchase made through an IRA-owned LLC.

What McNulty v. Commissioner decided

In McNulty v. Commissioner (157 T.C. No. 10), a taxpayer directed a self-directed IRA to fund a single-member LLC. The LLC bought American Eagle coins, and the taxpayer received and controlled the coins. The U.S. Tax Court held that the taxpayer received taxable IRA distributions equal to the cost of the coins when physical custody was obtained. The court did not hold that every self-directed IRA investment through an LLC is invalid — it focused on personal possession and control of the IRA coins, explaining that a qualified custodian must maintain custody, records, and transaction oversight. The practical lesson is narrow but important: an LLC label does not erase the custody requirement. Personally controlled coins can be treated as a distribution even when paperwork says the LLC owns them. This case is one of several documented in the scam warning signs guide.

"IRS-approved depository" is often imprecise wording

Marketing pages often use the phrase "IRS-approved depository." The more precise federal rule concerns the trustee or custodian. The IRS maintains a list of approved nonbank trustees and custodians under Treasury Regulation Section 1.408-2(e). A metals depository may hold assets under an arrangement directed by the custodian, but the IRS does not endorse a dealer, metal product, or storage pitch merely because a facility is described as approved. Prepper gold storage rules should therefore begin with written confirmation from the IRA custodian identifying the trustee or custodian, the depository, the storage arrangement, the reporting process, and the procedure for sale or in-kind delivery. Customers should speak to a financial or tax advisor before making decisions involving IRA custody, LLC structures, physical possession, or storage. Goldco does not offer tax or legal advice.

Self-Directed IRA Physical Gold Rules

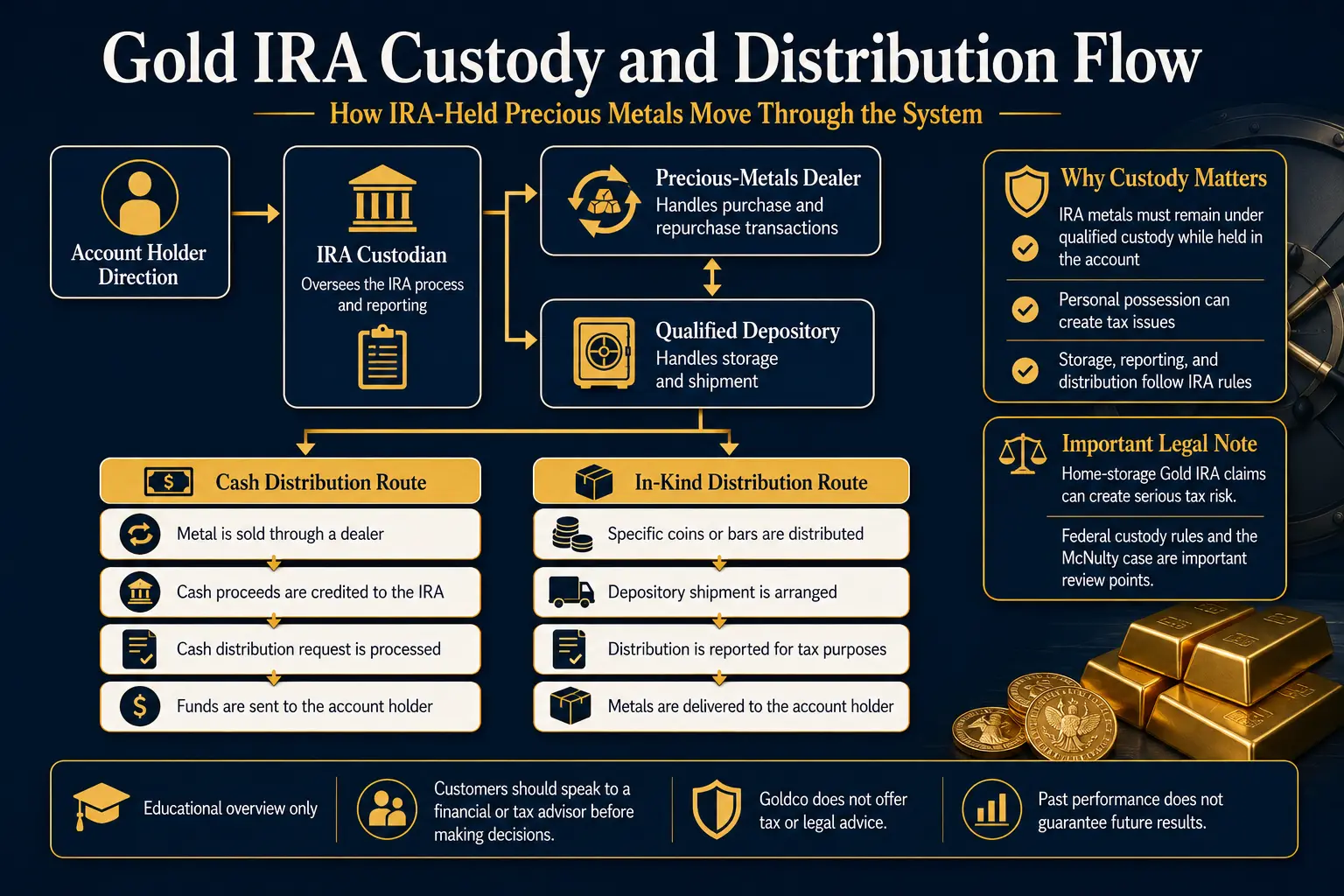

A self-directed IRA is not a separate tax class. It is an IRA in which the custodian permits a broader menu of assets and the account holder directs transactions — the same federal IRA rules still apply. Federal law generally treats metals and coins as collectibles, then creates exceptions for specified U.S. coins, certain state-issued coins, and qualifying gold, silver, platinum, or palladium bullion that meets statutory fineness requirements and remains in proper trustee possession. A dealer's description of a product as "IRA eligible" is not a substitute for custodian acceptance; custodian operating rules can include product, refiner, condition, and packaging requirements beyond the basic federal framework.

The custodian, dealer, and depository have different roles. The custodian administers the IRA, processes directions, maintains records, and reports account events. The dealer quotes and sells or repurchases the metal. The depository receives, records, stores, and ships the physical product under the custody arrangement. FINRA and the CFTC warn that self-directed IRA customers often bear responsibility for evaluating the dealer, price, spread, and asset because the account is self-directed. A custodian's willingness to process a direction does not mean the custodian has judged the price or quality of the metal, so written dealer quotes, buyback terms, fee schedules, and depository details remain central due-diligence documents.

The Tax-Advantaged Structure: What It Actually Provides

The phrase "gold IRA tax benefits for preppers" can sound broader than the law allows. The account provides IRA tax treatment; it does not give gold a separate tax exemption. A traditional IRA is a tax-advantaged personal savings plan: contributions may be deductible depending on income, filing status, and workplace-plan coverage; amounts inside can generally grow without annual tax reporting for each internal purchase or sale; and distributions are generally taxable in the year received, except for properly documented basis. A Roth IRA is funded with after-tax money and is not deductible, but qualified distributions may be tax-free, and an original Roth owner is not required to take lifetime required minimum distributions.

Existing retirement money may sometimes move into a self-directed IRA through a transfer or rollover. A direct trustee-to-trustee movement avoids personal receipt of the money; when an eligible distribution is paid to an individual, the normal rollover deadline is 60 days, subject to federal rules and limited waiver procedures. A rollover does not make unsuitable metal suitable, remove storage requirements, or remove later distribution taxes — it only moves eligible retirement assets under the applicable rollover rules. Customers should speak to a financial or tax advisor before making decisions involving contributions, transfers, rollovers, Roth conversions, or distributions. Goldco does not offer tax or legal advice.

Gold IRA Liquidity for Preppers: The Emergency Reality

A Gold IRA can be liquidated, but it should not be described as instant-access money. The process can involve a dealer, a custodian, a depository, shipping or internal transfer, sale proceeds, and a separate distribution request. One custodian (STRATA) publishes an estimated 5 to 13 business days for the dealer-transfer stage of a precious-metals liquidation, and requires the dealer to remit proceeds within five business days after receiving the metals. Once sufficient cash is already available in the IRA, STRATA states that cash distributions are generally processed within two to five business days, depending on delivery method — these are provider estimates, not a universal industry timeline. The full exit picture is in the exit strategies guide.

An in-kind distribution is another route: the depository ships the metal out of the IRA, and the custodian reports the transaction as a distribution, with postage, insurance, and packaging costs. A distribution before age 59½ can be subject to an additional 10% federal tax unless an exception applies. The liquidity lesson is simple: a Gold IRA can provide an exit route, but it is not the same as a checking account or a directly held coin. A preparedness plan that may require same-day funds generally needs a separate liquid reserve — Consumer Financial Protection Bureau research links emergency savings with stronger household financial security and shows that retirement withdrawals are more common among households without adequate emergency savings. Customers should speak to a financial or tax advisor before making decisions involving emergency withdrawals, liquidation, withholding, or in-kind distributions. Goldco does not offer tax or legal advice.

Diversification, Not Disaster Marketing

Preparedness can support careful planning without extreme predictions. Investor.gov defines diversification as spreading money among different investments to reduce risk, and explains that it cannot remove all loss risk. Gold may behave differently from stocks, bonds, or cash during some periods, but it remains a market-priced asset; the CFTC states that precious-metals prices can be highly volatile and warns that fear-heavy or high-pressure sales tactics can be associated with fraud. A balanced approach therefore avoids two extremes: treating gold as unnecessary in every retirement plan, and treating gold as the only asset needed for preparedness. The relevant issues are purpose, time horizon, cash needs, total allocation, fees, tax status, and the role of other assets. FINRA and the CFTC advise comparing the dealer's retail price with spot, asking for the buyback price, identifying the spread, and obtaining all commissions and fees in writing, noting that collectible or semi-numismatic products can be harder to resell than common bullion. A framework for how much metal fits a plan is in the due-diligence questions.

Storage: Qualified Custody, Segregated, and Commingled

The federal tax rule focuses on qualified custody; commercial storage contracts then determine how the metal is organized inside the vault. Under an allocated or commingled arrangement, metals are recorded for an account but stored alongside similar products belonging to other accounts, and the account may later receive equivalent metal of the same type, weight, and standard rather than the exact original pieces. Under segregated storage, the specific coins or bars are kept separately for the account, which usually costs more. These are commercial custody terms, not separate IRA tax categories, and neither changes the basic rule that IRA metals must remain within qualified custody until a sale, transfer, or distribution is completed. The full trade-off is covered in segregated vs commingled storage. A storage review should cover the custodian and depository legal names and roles, whether the arrangement is segregated or commingled, annual storage and insurance charges, the inventory and statement process, the procedure and cost for dealer shipment or in-kind delivery, and the depository's audit and claims procedures. Customers should speak to a financial or tax advisor before making decisions involving storage, custody, distributions, or account ownership. Goldco does not offer tax or legal advice.

Questions Preppers Should Ask Before Funding a Gold IRA

- Is the purpose immediate access or retirement diversification? A retirement account should not be assigned the same role as an emergency-cash reserve.

- Is the account traditional or Roth? The type affects deductibility, later taxation, required distributions, and Roth qualification. The word "gold" does not change those rules.

- Is the funding a contribution, transfer, or rollover? Each has different limits, paperwork, and tax consequences. Direct trustee-to-trustee movements reduce the risk of personal receipt.

- Which products will the custodian accept? Get the exact coin or bar, refiner or mint, fineness, condition, and packaging requirements in writing.

- What is the dealer's same-day buyback price? The spread between retail and repurchase price affects the break-even point. Get prices, fees, and buyback terms in writing.

- What happens when cash is needed? The written process should explain dealer selection, quote approval, depository transfer, custodian processing, cash delivery, withholding, fees, and timing.

- What happens during an in-kind distribution? The answer should cover valuation, Form 1099-R reporting, shipping, insurance, and the exact point personal possession begins. It is a reportable IRA event, not a way to move metal home while keeping IRA status.

- Who is providing tax or legal guidance? A dealer, custodian, and depository perform different functions. Marketing material from a transaction promoter is not independent tax analysis — a point the McNulty opinion emphasized.

Customers should speak to a financial or tax advisor before making decisions involving funding, rollovers, withdrawals, tax reporting, or storage. Goldco does not offer tax or legal advice. Not sure if a Gold IRA fits the plan at all? The 2-minute quiz is educational and makes no recommendation.

Frequently Asked Questions

Is a Gold IRA useful for preppers?

A Gold IRA may fit a preparedness-minded retirement plan when the goal is long-term diversification inside a traditional or Roth IRA. It is less suitable for assets expected to provide immediate physical access, because the metals must remain under qualified custody while held in the IRA.

Can Gold IRA metals be stored at home?

Personal possession while the metal remains claimed as an IRA asset creates serious tax risk. The IRS says qualifying bullion must be in the physical possession of a bank or approved nonbank trustee, including bullion bought indirectly through an IRA-owned LLC. The Tax Court treated personally controlled American Eagle coins in McNulty as taxable distributions.

Can Gold IRA metal be accessed during an emergency?

The metal can generally be sold inside the IRA or distributed in kind, but the process may require several institutions and can create taxes, additional taxes, shipping charges, and reporting. Published processing times vary by custodian and transaction.

Does a Gold IRA eliminate taxes?

No. A traditional Gold IRA generally defers tax until distribution, while qualified Roth IRA distributions may be tax-free. Early or nonqualified distributions can have different results.

Are all gold coins allowed in an IRA?

No. Federal law permits specified coins and qualifying bullion while treating many other metals and coins as collectibles. Custodians can also limit the products supported on their platforms.

Is segregated storage required?

Federal tax law requires qualified custody, but it does not make segregated storage mandatory for every precious-metals IRA. Segregated and commingled storage are contractual arrangements that affect item identification, return of specific pieces, and cost.

Update Log

- 2026: Initial publication. Sourced to IRS (Pub 590-A/590-B, collectibles and custody rules), Internal Revenue Code Section 408, the U.S. Tax Court decision in McNulty v. Commissioner (157 T.C. No. 10), FINRA/CFTC investor guidance, and published custodian/depository processes. Confirm current rules with the IRS or a professional before acting.

Sources

- Internal Revenue Service. Individual Retirement Arrangements (IRAs).

- Internal Revenue Service. Traditional and Roth IRAs.

- Internal Revenue Service. Publication 590-A (Contributions to IRAs).

- Internal Revenue Service. Publication 590-B (Distributions from IRAs).

- Internal Revenue Service. Retirement Plans FAQs Regarding IRAs.

- Internal Revenue Service. Investments in Collectibles in IRA Accounts.

- Cornell Law School (LII). 26 U.S. Code § 408 (IRAs).

- KPMG. McNulty v. Commissioner — Tax Analysis (2021).

- Internal Revenue Service. Approved Nonbank Trustees and Custodians.

- Internal Revenue Service. Rollovers of Retirement Plan and IRA Distributions.

- Internal Revenue Service. Retirement plans faqs regarding iras distributions withdrawals.

- Internal Revenue Service. Publication 550 (Investment Income and Expenses).

- Internal Revenue Service. Tc409.

- FINRA. 10 Things to Ask Before Buying Physical Gold, Silver or Other Metals.

- Commodity Futures Trading Commission. Gold Is No Safe Investment.

- Investor.gov (SEC). Asset Allocation Basics.

- Consumer Financial Protection Bureau. Cfpb mem emergency savings financial security report 2022 3.

- STRATA Trust. How to liquidate my precious metals.

- STRATA Trust. How to take a cash distribution from strata my strata ira.

- GoldStar Trust. Precious metals iras investment disclosure.

- GoldStar Trust. Education.

- The Entrust Group. Precious metals.

- The Entrust Group. How to purchase precious metals.

- Delaware Depository. Storage transfer.

Article reviewed and edited by Daniel M. — editor, 401kToGoldIRA.org. Sourced to IRS.gov, the U.S. Tax Court, FINRA, and the CFTC; educational only, not tax or legal advice.