Affiliate disclosure: Some links on this page may be sponsor links. The site owners may be compensated if customers request information from companies mentioned here. This page is educational only and does not provide financial, tax, or legal advice. Past performance does not guarantee future results. Goldco does not offer tax or legal advice. Customers should speak to a financial or tax advisor before making decisions about rollovers, allocations, withdrawals, or estate planning related to any Gold IRA or retirement account.

Quick Answer: How a Gold IRA May Fit a First Responder's Retirement

For many public-safety professionals, retirement income starts with a defined-benefit pension and may be supplemented by 457(b), 403(b), or IRA savings. A Gold IRA is a self-directed IRA that holds IRS-approved physical gold and other metals; it can sometimes be funded by rolling over part of those savings to add diversification and potential inflation protection alongside the pension.

The key questions are:

- Which accounts are eligible to move into a self-directed Gold IRA?

- How much of total retirement savings should be in any single asset class, including gold?

- How do fees, storage rules, and liquidity compare with existing options?

Educational tools such as the Gold IRA Calculator, the rollover guide, the Best Gold IRA Companies comparison, and the 2-minute quiz can help first responders explore these questions in more detail.

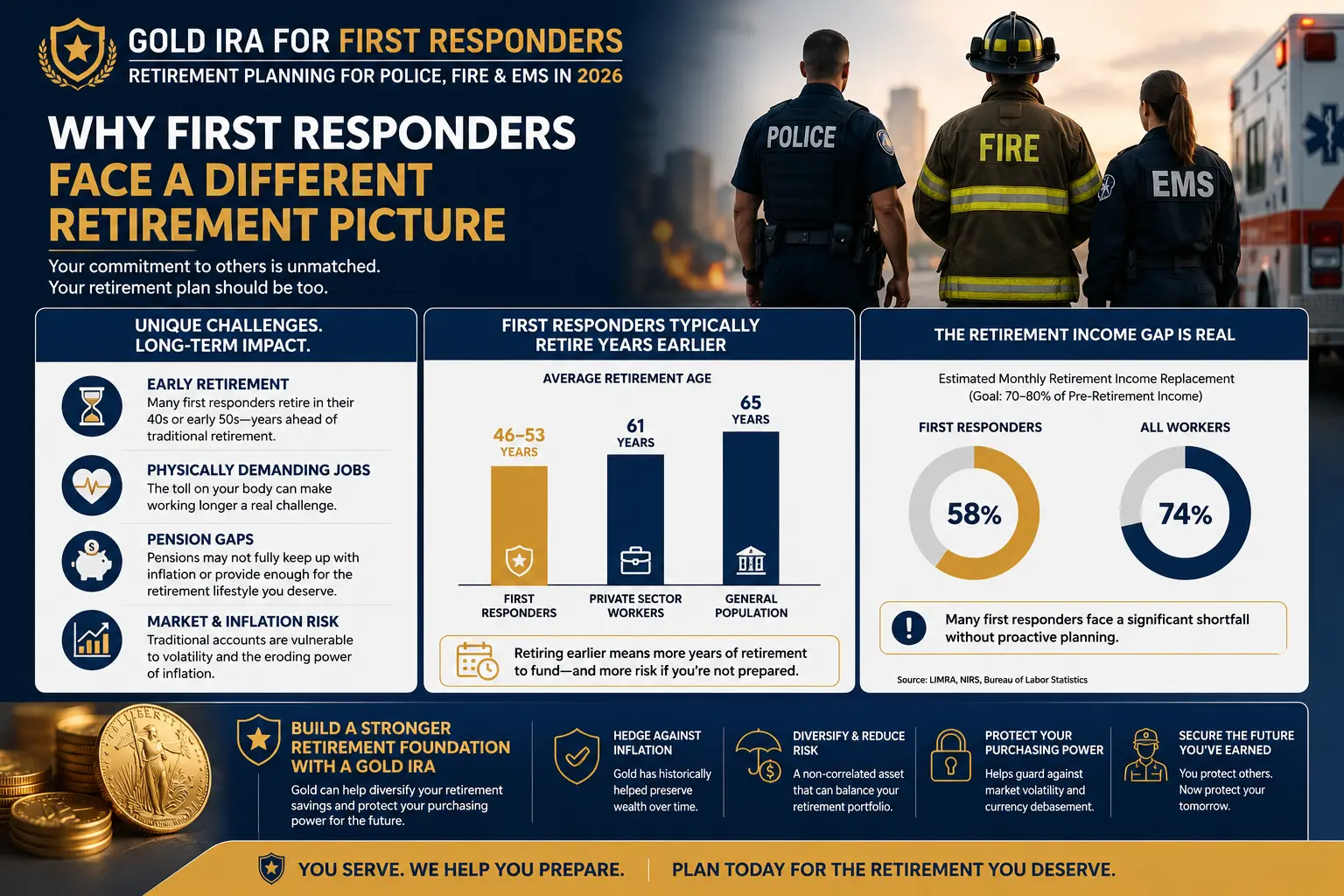

Why First Responders Face a Distinct Retirement Picture

Financial-planning guides consistently note that first responders face a unique retirement landscape. Several patterns stand out:

- Pension reliance and early retirement. Many police officers, firefighters, and EMS personnel participate in defined-benefit pension systems that may allow retirement earlier than traditional private-sector norms, often based on years of service rather than age alone.

- Irregular income and overtime. Overtime and specialty pay can vary year to year, making it harder to plan contributions and long-term savings without a strategy.

- Inflation and COLA risk. Cost-of-living adjustments (COLAs) in public-safety pensions may not fully keep pace with inflation every year, so some advisors encourage adding personal savings and diversified investments to reduce reliance on a single pension stream.

Because of these factors, diversification across pension income, deferred-comp plans, IRAs, and other assets often becomes a central topic in planning discussions.

Common First Responder Retirement Accounts: Pension, 457(b), 403(b), IRA

Educational material for police, fire, and EMS often highlights four main retirement structures.

Defined-benefit pension

Most first responders participate in a public-safety pension that promises a formula-based monthly benefit tied to service years and final average salary. This pension may be the largest single source of retirement income, especially for those who retire from the same agency after a full career.

457(b) deferred compensation

Governmental 457(b) plans are common for police and fire employees and often serve as tax-advantaged savings alongside pensions. Contributions are made via salary deferral; earnings generally grow tax-deferred until withdrawn, and these plans may allow penalty-free withdrawals in some circumstances after separation, even before age 59½. Plan menus usually include mutual funds, target-date funds, annuity products, and sometimes brokerage windows, but rarely direct physical gold. Contribution limits for 2026 typically allow substantial deferrals, with additional catch-up contributions near retirement age.

403(b) and other employer plans

Some first responders, especially those attached to hospitals or nonprofit entities, may have access to 403(b) plans or similar defined-contribution accounts. These function similarly to 401(k) plans, with pre-tax or Roth contributions and employer matching in some cases.

Individual Retirement Accounts (IRAs)

Advisors frequently suggest that first responders consider IRA contributions to supplement pension and deferred-comp savings. Traditional IRAs offer tax-deferred growth and potential deductions; Roth IRAs offer tax-free qualified withdrawals under specific conditions. A Gold IRA is a specialized self-directed IRA, not a separate account type; it follows IRA rules but allows certain precious metals as plan assets.

How a Gold IRA Rollover Could Add Diversification to a Pension-Heavy Plan

Educational Gold IRA articles often position physical gold as one possible diversification tool alongside pensions and conventional investments. For first responders, a Gold IRA might play several roles:

- Diversification away from a single pension stream. Adding some exposure to metals can broaden the range of assets supporting retirement, rather than relying solely on one employer pension and stock-bond portfolios.

- Complement to "paper gold" in 457(b) or 403(b) plans. Some 457(b) plans offer gold-related mutual funds or ETFs, but typically do not allow physical bullion; a self-directed Gold IRA can hold IRS-approved coins and bars as an additional layer.

- Potential long-term hedge against inflation and market volatility. Gold is widely discussed as a potential hedge, though research shows its effectiveness varying across time periods and markets.

Rollover guides explain that investors can sometimes move funds from 401(k)s, 403(b)s, and governmental 457(b)s into self-directed IRAs that invest in physical metals, as long as IRS rollover rules and plan provisions are followed. Goldco does not offer tax or legal advice. Customers should speak to a financial or tax advisor before deciding whether any pension-adjacent or deferred-comp assets should be rolled into a Gold IRA, and what allocation level might be appropriate.

Model a hypothetical allocation first

The calculator and quiz walk through scenarios and questions before any real rollover is considered.

Try the Gold IRA Calculator → Take the Free Quiz →Eligibility: Which First Responder Accounts Can Roll to a Self-Directed IRA

Not all retirement accounts can move into a Gold IRA, and eligibility rules can differ for police, fire, EMS, and other public-sector plans. Common patterns in educational sources include:

- Governmental 457(b) plans. These often allow rollovers to IRAs, 401(k)s, 403(b)s, or other governmental 457(b)s when employment ends or specific conditions are met. A first responder with such a plan may be able to roll funds into a self-directed IRA that holds precious metals, subject to plan terms.

- 401(k) and 403(b) plans. Many employer plans allow rollovers to IRAs at separation, and sometimes in-service rollovers, enabling transfers into self-directed Gold IRAs. Eligibility depends on the plan document and employer policy.

- Defined-benefit pensions. Traditional public-safety pensions generally do not roll into IRAs; rather, they pay monthly benefits based on formulas, sometimes with options for partial lump sums. Any Gold IRA funding from pensions would typically come from separate savings, not from the pension benefit itself.

- Existing IRAs. Existing traditional IRAs can be transferred to self-directed IRAs under custodian-to-custodian transfer rules, allowing conversion from mutual-fund IRAs to Gold IRAs without changing IRA type.

It is important to distinguish between direct trustee-to-trustee rollovers and 60-day indirect rollovers, because indirect rollovers can trigger taxes and penalties if timing is not handled correctly. The rollover guide offers more detail on these mechanics. Goldco does not offer tax or legal advice. Customers should speak to a financial or tax advisor before initiating any rollover or transfer from 457(b), 403(b), IRA, or pension-linked accounts into a Gold IRA.

Fees, Storage, and Liquidity Trade-Offs for Public Safety Savers

Self-directed precious-metals IRAs involve higher and more complex fee structures than many standard retirement accounts. Important trade-offs include:

- Fee layers. Gold IRAs typically charge setup or account-opening fees, annual custodian fees, depository storage fees, and dealer spreads with possible buyback fees.

- Spreads and markups. Dealers often charge markups above spot for coins and bars, and may offer different buyback prices later.

- Minimums. Many companies set minimum initial investments, often in the tens of thousands of dollars, which can make these accounts more practical for larger retirement balances.

- Liquidity. Gold must be sold or taken in kind from the IRA before cash is available; this can be slower and involve more steps than selling a mutual fund in a conventional plan.

First responders considering Gold IRAs often compare these costs to fees in existing pensions, 457(b) plans, and mutual-fund IRAs, using tools such as the fee calculator, the markups and spreads guide, the fees guide, and the comparison workbook.

Creditor-Protection and State-Law Considerations for First Responders

Creditor protection and state-law differences matter for many public-safety professionals, especially those concerned about liability and asset protection. Estate and retirement sources explain that:

- IRAs often receive some level of protection from creditors in bankruptcy, but the extent of protection can vary by state and by whether the IRA is traditional, Roth, or inherited.

- Employer retirement plans such as governmental 457(b)s and certain pensions may be governed by different statutes, sometimes offering strong protection under state law.

- Trusts, titling choices, and beneficiary designations interact with these rules and can influence how assets are treated after death or in legal proceedings.

Gold IRA assets fall under IRA and self-directed account rules, so any creditor-protection analysis should consider both federal bankruptcy law and state-specific protections. The creditor protection by state content is designed to help investors ask informed questions about how Gold IRAs fit into state-law frameworks. Goldco does not offer tax or legal advice. Customers should speak to a financial or tax advisor — and often an attorney familiar with public-safety benefits and state law — before relying on any Gold IRA structure for creditor or asset-protection planning.

Questions a First Responder Should Ask Before Opening a Gold IRA

Gold IRA education pieces and provider due-diligence guides list many questions that apply to first responders and other investors alike.

Plan and rollover questions

- What retirement accounts (457(b), 403(b), IRA) are eligible for rollover, and under what conditions (separation from service, in-service rollovers, or age milestones)?

- Will any rollover impact pension eligibility or service calculations, or is it limited to defined-contribution balances?

Provider and custodian questions

- Is the custodian experienced with self-directed IRAs and IRS-approved precious metals?

- What are all setup, annual, transaction, storage, and buyback fees?

- Which depositories are used, and how is insurance and segregation handled?

- What minimum investment is required, and what ongoing balance thresholds apply?

The 21 questions to ask before opening a Gold IRA complements third-party checklists and helps investors prepare for these conversations.

Allocation and risk questions

- How large should any Gold IRA allocation be relative to pension benefits and other investments, and does that align with long-term risk tolerance?

- How will metals interact with existing "paper gold" exposure in 457(b) or 403(b) plans, if present?

- How will liquidity needs and emergency-fund goals be met outside the Gold IRA?

Customers should speak to a financial or tax advisor before deciding on allocation percentages, rollover amounts, or provider choices, especially when public-safety pensions and multiple plans are involved. Goldco does not offer tax or legal advice.

Frequently Asked Questions

Are Gold IRAs commonly used in first responder retirement planning?

Educational material for first responders focuses primarily on pensions, 457(b) plans, 403(b)s, and IRAs, with diversification beyond the pension suggested through additional savings. Gold IRAs appear in general retirement and diversification discussions rather than as a standard public-safety benefit, and may be considered by some as a specialized tool for holding precious metals within a self-directed IRA.

Can a 457(b) plan be rolled into a Gold IRA?

Governmental 457(b) accounts often allow rollovers to IRAs when certain conditions are met, and a self-directed IRA can then hold IRS-approved physical gold under Gold IRA rules. Non-governmental 457 plans and some employer arrangements may have different restrictions, so plan documents and administrator guidance must be reviewed in each case.

Does a Gold IRA replace a public safety pension?

No. Public-safety pensions are defined-benefit plans that pay formula-based monthly income, while Gold IRAs are individual accounts holding assets that can rise or fall in value. A Gold IRA, if used, usually serves as an additional diversification tool alongside a pension and other savings, not as a replacement.

Are Gold IRAs more expensive than typical deferred-comp plans?

Self-directed precious-metals IRAs carry extra fees for custody, depository storage, and dealer spreads, and often involve higher minimum balances. Deferred-comp plans such as 457(b)s or 403(b)s often offer lower-cost mutual funds or annuities instead, so fee comparisons are an important planning step.

Should first responders rely on gold to solve inflation or pension concerns?

Financial-planning resources for first responders emphasize a mix of strategies: understanding pension formulas, using deferred-comp and IRAs, managing irregular income, and building emergency funds. Gold can be one element in a diversified plan, but no single asset fully addresses inflation, pension structure, or broader financial risks.

Goldco does not offer tax or legal advice. Customers should speak to a financial or tax advisor before making any Gold IRA, rollover, or allocation decision based on general information or FAQs.

Article reviewed and edited by Daniel M. — editor, 401kToGoldIRA.org.

Further Reading

How Much Gold Should Investors Own in Retirement?A framework for matching allocation to goals, liquidity, and risk tolerance.

How Much Gold Should Investors Own in Retirement?A framework for matching allocation to goals, liquidity, and risk tolerance. Gold IRA Rollover Survival GuideRollover eligibility, transfers, and the 60-day rule explained step by step.

Gold IRA Rollover Survival GuideRollover eligibility, transfers, and the 60-day rule explained step by step. 21 Questions to Ask Before Opening a Gold IRAThe written due-diligence list before any provider conversation.

21 Questions to Ask Before Opening a Gold IRAThe written due-diligence list before any provider conversation.