Affiliate disclosure: Some of the links in this article are from sponsors. The site owners may be compensated if customers request information from companies mentioned. Reviews may not be neutral or independent — readers should treat this site as a research starting point, not personalised financial advice. Read the full disclosure.

Quick Answer

Under federal bankruptcy law, most traditional and Roth IRAs — including Gold IRAs — are protected up to $1,711,975 per person in bankruptcy filings for the 2025-2028 period, with unlimited protection for rollover IRAs sourced from ERISA-qualified plans if kept separate. Outside bankruptcy (for example, in a civil lawsuit or business judgment), state law controls whether a Gold IRA is reachable, with some states (Florida, Texas, others) granting unlimited protection, some imposing dollar caps, and others protecting only what a court finds "reasonably necessary" for retirement.

Past performance does not guarantee future results.

Not sure which Gold IRA provider fits the bracket? The 2-minute matching quiz on this site narrows the choice based on retirement timing, savings band, and priorities.

The Two Layers of Gold IRA Creditor Protection

Every Gold IRA sits under two distinct legal layers of creditor protection:

- Federal bankruptcy protection (BAPCPA)

- Applies when an IRA owner actually files for personal bankruptcy.

- Sets national rules for how much of the IRA balance is exempt from the bankruptcy estate.

- State-law protection (non-bankruptcy)

- Applies in ordinary civil lawsuits, judgments, and collections where no bankruptcy case exists.

- Determines whether a judgment creditor can garnish or seize IRA assets, or force distributions in state court.

The fact that a Gold IRA is self-directed and holds physical metal does not change which layer applies; from a legal standpoint, it is still an IRA under Internal Revenue Code section 408. What changes is how easy it is for creditors or trustees to value and access the assets, not the core exemption rules.

Federal Protection in Bankruptcy: BAPCPA

The Bankruptcy Abuse Prevention and Consumer Protection Act of 2005 (BAPCPA) created a nationwide exemption for IRA funds in bankruptcy.

Key federal baseline rules:

- Traditional & Roth IRAs (including Gold IRAs): Protected up to an aggregate cap across all IRAs — originally $1,000,000; adjusted for inflation every three years. For bankruptcies filed between April 1, 2025 and March 31, 2028, multiple sources cite a cap of about $1,711,975 per person for combined traditional and Roth IRAs.

- SEP and SIMPLE IRAs: Treated like employer-established plans; generally receive unlimited bankruptcy protection, similar to 401(k)s, because of their ERISA-like status.

- Rollover IRAs from qualified plans: Bankruptcy law provides unlimited exemption for amounts traceable to rollovers from ERISA-qualified plans (401(k), 403(b), governmental 457(b), etc.).

- Inherited IRAs: After Clark v. Rameker (discussed below), inherited IRAs are not protected by the federal bankruptcy exemption at all.

Federal law only applies in bankruptcy cases. In a regular lawsuit with no bankruptcy filing, state law controls.

The Rollover IRA Advantage

For asset protection, the source of IRA funds matters as much as the balance.

Bankruptcy and asset-protection analysis highlights several advantages of rollover IRAs:

- Unlimited bankruptcy exemption for rollover balances: Funds moved from an ERISA plan (401(k), 403(b), etc.) to a rollover IRA can retain unlimited bankruptcy protection, because the money originated in a fully protected plan.

- Need for segregation: Many attorneys recommend that rollovers from qualified plans be kept in separate "rollover IRAs" rather than being mixed with contributory IRAs. If rollover funds and regular IRA contributions are commingled, some courts treat the entire account as subject to the capped exemption rather than unlimited protection.

- ERISA to IRA trade-off: Leaving assets in an ERISA-qualified plan usually offers stronger creditor protection outside bankruptcy than an IRA, because ERISA's "anti-alienation" clause heavily restricts creditor access. Rolling a 401(k) into a Gold IRA can increase investment flexibility but may reduce non-bankruptcy creditor protection, depending on state law.

This trade-off is one reason some high-risk professionals (physicians, business owners, landlords facing liability) hesitate to move large 401(k) balances into IRAs unless they have evaluated creditor-protection consequences.

Clark v. Rameker — Inherited IRAs Lose Federal Protection

The 2014 Supreme Court case Clark v. Rameker fundamentally changed federal protection for inherited IRAs.

The Court held that:

- Inherited IRAs are not "retirement funds" within the meaning of the federal bankruptcy exemption.

- Key differences from an owner's IRA included: beneficiaries cannot add contributions; beneficiaries must often take distributions regardless of age; beneficiaries may cash out the account at any time without early-withdrawal penalties.

Result: Inherited IRAs receive no federal bankruptcy exemption under BAPCPA. In bankruptcy, a debtor's inherited IRA may be fully exposed to creditors.

State law can partially restore protection:

- A small number of states explicitly protect inherited IRAs under their own exemption statutes, regardless of Clark.

- Examples include Florida, Texas, North Carolina, South Carolina, Alaska, Arizona, Idaho, Missouri, and Ohio.

For inherited Gold IRAs, this means that creditor protection depends heavily on which state's law applies, a topic discussed in more depth in the companion article on Inherited Gold IRA Rules.

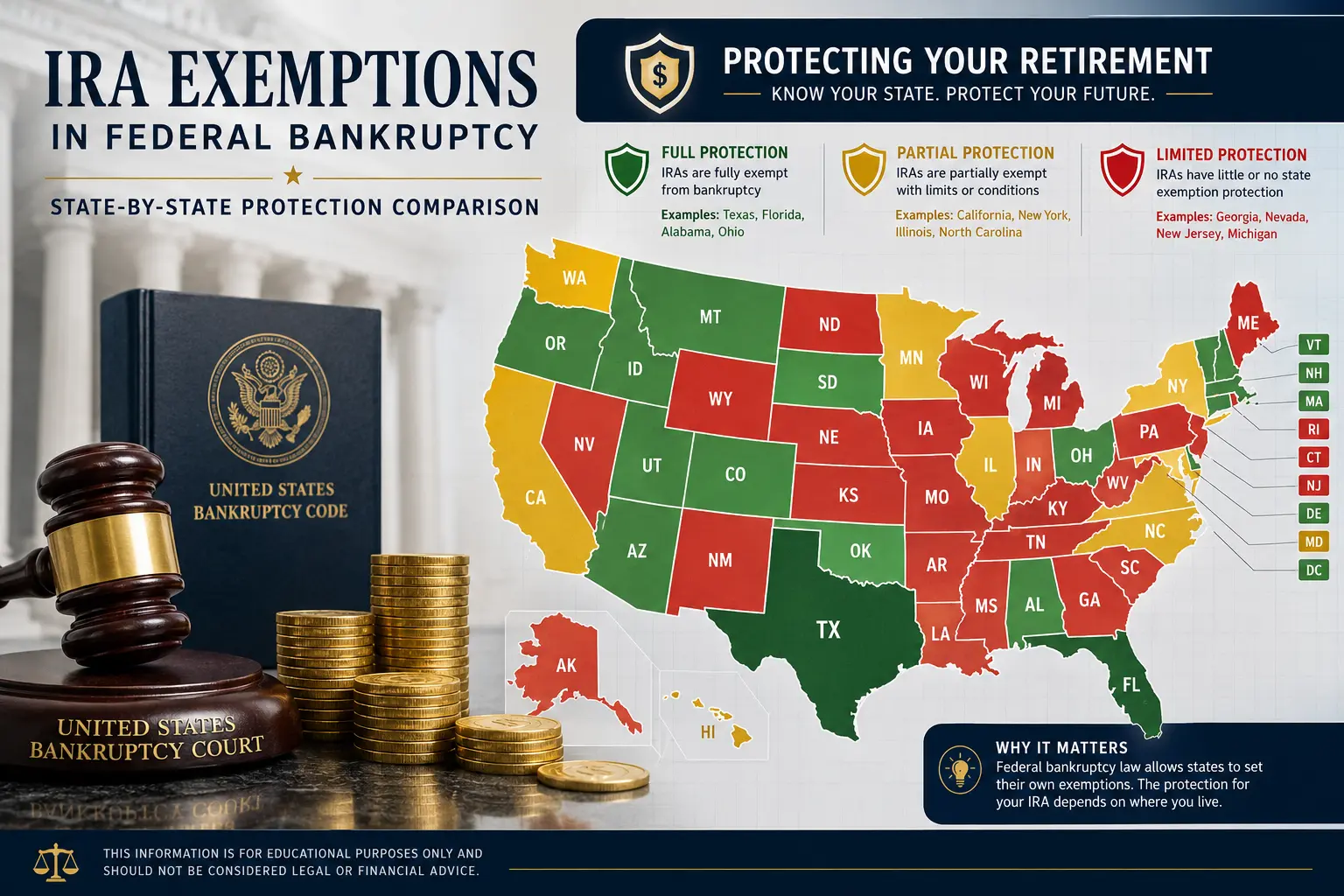

State-by-State Rules for Non-Bankruptcy Creditors

Outside bankruptcy, federal IRA exemptions do not apply; state law determines whether judgment creditors can reach a Gold IRA.

Patterns seen in 2026 state-by-state analyses include:

- Full protection states: Some states exempt all IRA assets (traditional and Roth) from judgment creditors, with no dollar cap. Examples include Florida, Texas, Connecticut, Illinois, Indiana, Iowa, Kansas, New Jersey, New Mexico, Oklahoma, Oregon, Washington, and Pennsylvania.

- Capped protection states: Several states protect IRAs up to a fixed dollar amount per account or in aggregate. Examples: Nevada (~$500,000 per IRA), South Dakota ($1 million), North Dakota ($100,000 per account / $200,000 aggregate), Minnesota (~$69,000 plus needs-based protection).

- Needs-based protection states: States such as California, Georgia, and Ohio protect IRA assets only to the extent "reasonably necessary" for the debtor's support in retirement. Courts in these states may allow creditors to reach balances considered "excess."

- States with limited or unclear protection: Some states exclude Roth IRAs or certain IRA types from protection, or use statutes that have produced inconsistent case law. Alabama, Maine, Mississippi, Nebraska, and West Virginia appear in this limited-coverage category in some reviews.

No state exemption blocks IRS tax liens, criminal restitution, or divorce-related domestic-relations orders, which are treated as "exception creditors."

The Strongest Asset Protection States for Gold IRAs

A handful of states are frequently cited as offering the strongest IRA creditor protection, which naturally extends to Gold IRAs held in those states.

Notable examples:

- Florida: Unlimited protection for traditional, Roth, SEP, SIMPLE, rollover, and inherited IRAs both inside and outside bankruptcy when Florida exemptions apply. Florida Stat. § 222.21 explicitly exempts all qualifying IRAs from most creditor claims without dollar limits.

- Texas: Often categorized as a full-protection state for IRAs outside bankruptcy, with broad statutory protection from judgment creditors. Some older bankruptcy commentary mentions a $100,000 cap in certain contexts, but more recent asset-protection overviews characterise Texas as effectively unlimited for IRAs in non-bankruptcy situations.

- Other full-protection states: Connecticut, Illinois, Indiana, Iowa, Kansas, New Jersey, New Mexico, Oklahoma, Oregon, Washington, and Pennsylvania also exempt IRA balances from most judgment creditors without a dollar cap.

For investors whose risk profile makes creditor protection a central concern, residency in one of these states can dramatically improve the overall protection profile of a Gold IRA.

📊 Project a Gold IRA Portfolio — the Gold IRA Calculator on this site compares a gold-diversified portfolio against an all-stock baseline.

The Weakest Asset Protection States

On the other end of the spectrum, some states provide only needs-based or partial protection, especially for Roth or inherited IRAs.

Examples:

- California: Uses a needs-based test for IRAs: only the portion "reasonably necessary" for support in retirement is exempt from creditors, and recent legislation has extended this analysis even to some qualified plans.

- Georgia and Ohio: Typically protect IRAs only to the extent necessary for the debtor's support, with courts evaluating income, age, and other assets.

- States with limited Roth or mixed coverage: Commentary notes that Alabama, Maine, Mississippi, Nebraska, and West Virginia either exclude Roth IRAs or provide only limited statutory coverage, creating uncertainty for Gold IRA owners in those jurisdictions.

In these weaker states, some investors focus more on maintaining ERISA-protected 401(k) balances or using trusts and other asset-protection tools rather than concentrating wealth in IRAs.

State-by-State Reference Table (High-Level)

The table below summarises general patterns of IRA creditor protection by state, based on multiple nationwide surveys. It is not a substitute for legal research; individual statutes, court decisions, and facts can change outcomes.

Legend:

- Unlimited: Statute broadly exempts IRAs from most judgment creditors with no dollar cap.

- Capped: Protection up to a statutory dollar limit.

- Needs-based: Protection only for amounts "reasonably necessary" for support.

- Partial / Varies: Mixed or unclear rules; may exclude some IRA types or rely on nuanced case law.

| State | Protection Level (Non-Bankruptcy) | Notes (High-Level) |

|---|---|---|

| Alabama | Partial / Varies | Limited coverage; Roth treatment uncertain |

| Alaska | Unlimited (incl. inherited) | Strong statute; inherited IRAs protected |

| Arizona | Unlimited (incl. inherited) | Broad IRA exemption; inherited IRAs covered |

| Arkansas | Partial / Varies | Some protection; details depend on statute and case law |

| California | Needs-based | Only amounts "reasonably necessary" for support protected |

| Colorado | Partial / Capped | Protection generally strong but may have caps/conditions |

| Connecticut | Unlimited | Full protection for traditional and Roth IRAs |

| Delaware | Partial / Capped | Exemption exists; details vary |

| Florida | Unlimited (incl. inherited) | Strongest category; all IRA types fully exempt by statute |

| Georgia | Needs-based | Support-based exemption; limited comfort for large balances |

| Hawaii | Partial / Capped | Protection with conditions and limits |

| Idaho | Unlimited (incl. inherited) | Statute extends to inherited IRAs |

| Illinois | Unlimited | Full protection, no dollar cap |

| Indiana | Unlimited | Full protection, no dollar cap |

| Iowa | Unlimited | Full protection, no dollar cap |

| Kansas | Unlimited | Full protection, no dollar cap |

| Kentucky | Partial / Capped | Significant but not fully unlimited protection |

| Louisiana | Partial / Varies | Mixed rules; trust and marital-property issues matter |

| Maine | Partial / Limited | Limited IRA exemption; Roth treatment uncertain |

| Maryland | Partial / Capped | Statutory protection with conditions |

| Massachusetts | Partial / Capped | Exemption exists; amount limited |

| Michigan | Partial (one IRA outside bankruptcy) | One IRA exempt from judgment creditors; broader in bankruptcy |

| Minnesota | Capped + Needs-based | ~$69,000 plus additional if necessary for support |

| Mississippi | Partial / Limited | Statute narrower; Roth treatment unclear |

| Missouri | Unlimited (incl. inherited) | Broad statute; inherited IRAs protected |

| Montana | Partial / Capped | Exemption present; cap applies |

| Nebraska | Partial / Limited | Limited IRA coverage; careful review needed |

| Nevada | Capped | Roughly $500,000 per IRA account |

| New Hampshire | Partial / Capped | Protection with limits |

| New Jersey | Unlimited | Full protection, no dollar cap |

| New Mexico | Unlimited | Full protection, no dollar cap |

| New York | Partial / Capped | Retirement funds generally protected, but specific caps apply |

| North Carolina | Unlimited (incl. inherited) | Strong statute, inherited IRAs covered |

| North Dakota | Capped | $100,000 per IRA, $200,000 aggregate |

| Ohio | Needs-based; inherited IRAs protected | Reasonably-necessary standard; statute also covers inherited IRAs |

| Oklahoma | Unlimited | Full protection, no dollar cap |

| Oregon | Unlimited | Full protection, no dollar cap |

| Pennsylvania | Unlimited | Retirement accounts broadly exempt from judgment creditors |

| Rhode Island | Partial / Capped | Protection exists, amount limited |

| South Carolina | Unlimited (incl. inherited) | Statute extends to inherited IRAs |

| South Dakota | Capped (~$1M) | Strong but capped exemption |

| Tennessee | Partial / Capped | Dollar cap and other conditions |

| Texas | Unlimited (incl. inherited) | Full protection; strong inherited IRA statute |

| Utah | Partial / Capped | Protection with statutory limits |

| Vermont | Partial / Capped | Exemption exists, capped and conditioned |

| Virginia | Partial / Capped | Protection subject to limits and timing rules |

| Washington | Unlimited | Full protection, no dollar cap |

| West Virginia | Partial / Limited | Statute narrower; some IRA types may be excluded |

| Wisconsin | Partial / Capped | Protection exists with limits |

| Wyoming | Partial / Strong | Broad exemption but not always explicitly unlimited |

Because state statutes and case law change, this table should be treated as a starting point for conversation with counsel, not a final answer.

ERISA vs IRA Protection

A recurring theme in asset-protection guidance is that ERISA-qualified plans (like most employer 401(k)s) often provide stronger creditor protection than IRAs.

Key contrasts:

- ERISA plans (401(k), many 403(b), some 457(b)): Protected by ERISA's anti-alienation clause, which generally blocks most creditors from seizing assets both inside and outside bankruptcy, with exceptions for IRS, QDROs, and criminal matters. In bankruptcy, ERISA plans usually have unlimited protection.

- IRAs (including Gold IRAs): Protected in bankruptcy by BAPCPA up to the federal cap (plus unlimited for rollover funds if segregated). Outside bankruptcy, protection depends entirely on state law, which can range from unlimited to almost none.

For some investors, this trade-off means that keeping part of a retirement balance in a 401(k) rather than rolling everything into a Gold IRA can be an asset-protection decision as much as an investment decision.

Divorce and Gold IRAs

Divorce is a special category of creditor risk because many exemptions explicitly do not protect against domestic-relations claims.

Key points:

- Qualified plans (401(k)s): Divided via Qualified Domestic Relations Orders (QDROs), which allow courts to assign part of a retirement plan to a former spouse or dependent for support. ERISA protection does not block QDROs.

- IRAs (including Gold IRAs): Technically, QDROs do not apply, but divorce courts routinely order transfers or divisions of IRA assets as part of equitable distribution or community-property division. Exemption statutes almost always exclude divorce judgments and family-support obligations from protection.

So while a Gold IRA may be well-protected from business creditors in Florida or Texas, it can still be divided in divorce under state family-law rules.

Self-Directed Gold IRA Specific Considerations

From a legal standpoint, a Gold IRA is still an IRA, so the same creditor-protection statutes apply. However, there are some practical nuances:

- Physical metal vs securities: Creditor-protection statutes usually do not distinguish between bullion and mutual funds; the law focuses on the IRA wrapper, not the underlying asset. That said, trustees and courts may face valuation and liquidation questions when IRA assets consist of coins and bars, especially in smaller, illiquid formats.

- Self-directed IRA LLCs: Some Gold IRAs use an IRA-owned LLC structure. Asset-protection commentators stress that this does not usually add creditor protection against the IRA owner's personal creditors; it is mainly about investment control, not exemption law. If LLC formalities are not followed, courts can pierce the veil, leaving underlying assets exposed.

- Prohibited transactions risk: A prohibited transaction (for example, self-dealing with IRA metals) can disqualify the IRA, converting assets into taxable property and potentially eliminating creditor protection. For self-directed Gold IRAs, compliance with IRS rules is part of preserving both tax and protection benefits.

Asset Protection Strategies for Gold IRA Owners

Asset-protection attorneys often recommend high-level strategies rather than quick fixes.

Common themes (to be implemented only with professional advice):

- Understand federal caps and rollover advantages: Maintain separate rollover IRAs for assets traced to ERISA plans to preserve unlimited bankruptcy protection. Track contribution sources carefully.

- Use state-law strengths: In full-protection states, investors may be comfortable holding larger Gold IRA balances. In needs-based or limited-protection states, some may prefer to allocate more to ERISA-protected plans or other tools.

- Avoid last-minute transfers: Moving assets shortly before litigation or bankruptcy can be treated as fraudulent transfer, undermining both protection and credibility.

- Coordinate estate planning: Align beneficiary designations, trusts, and titling with protection goals, especially after Clark v. Rameker for inherited IRAs. The article on Inherited Gold IRA Rules covers this angle in more depth.

- Consider broader asset-protection structures: In some cases, attorneys employ domestic or offshore asset-protection trusts, insurance, and corporate structures alongside IRAs. These tools are complex and jurisdiction-specific.

Customers should speak to a financial or tax advisor — and a qualified asset-protection or bankruptcy attorney — before making decisions. The Gold IRA Rollover Survival Guide on this site discusses how rollover decisions intersect with these issues.

What Happens to a Gold IRA in Active Bankruptcy

When an IRA owner actually files for personal bankruptcy, the process typically looks like this:

- Determine exemption scheme: The debtor chooses between federal and state exemptions where allowed; some states have "opted out" of federal exemptions and require use of state exemptions.

- Apply IRA exemptions: Under BAPCPA, traditional and Roth IRAs are exempt up to $1,711,975 (2025-2028), with unlimited protection for traceable rollover funds in separate accounts. In states that extend additional IRA protection, the combined shield can be stronger.

- Treatment of Gold IRAs: The trustee includes Gold IRA assets in the bankruptcy schedules, but exempt portions are not available to unsecured creditors. If part of the Gold IRA is non-exempt, the trustee may liquidate metals through the custodian to raise cash for the estate.

- Inherited IRAs: An inherited Gold IRA generally receives no federal bankruptcy protection under Clark v. Rameker; the trustee may treat it as fully available to creditors unless state law provides a special inherited-IRA exemption.

- Exception creditors: Even when exempt, IRAs can still be reached for IRS tax liens, family-support obligations, and criminal restitution, which sit outside ordinary exemption rules.

In all cases, the presence of gold or silver does not change the basic exemption math; it simply affects how assets are liquidated or distributed.

Cross-State Issues — Moving Between States

Many Gold IRA owners move between states during retirement. This can change creditor protection:

- Bankruptcy domicile rules: Federal bankruptcy law uses a look-back period (often 730 days) to determine which state's exemptions apply, based on where the debtor has recently lived. A move shortly before filing does not automatically allow access to a new state's stronger exemptions.

- Non-bankruptcy lawsuits: For state-court judgments, current residency and asset location matter. A move from a needs-based state to a full-protection state can improve future protection, but may not cure past exposures.

Because these cross-border issues are technical, investors often revisit asset-protection plans when changing primary residence, especially when moving to or from states like Florida, Texas, or California.

Bottom Line

Gold IRA creditor protection is not one simple rule; it is a matrix of federal bankruptcy caps, rollover tracing rules, state-law exemptions, and case law like Clark v. Rameker. For some investors in states like Florida and Texas, a Gold IRA can be nearly as well-protected from most creditors as a 401(k), while for others in needs-based or limited-protection states, large Gold IRA balances may be more exposed than expected.

Because the same account decisions that drive tax results — such as rolling a 401(k) into a Gold IRA, or consolidating multiple IRAs — also change the asset-protection profile, it makes sense to coordinate investment, tax, and legal advice rather than viewing them separately. Past performance does not guarantee future results, and gold and other precious metals can be volatile; creditor-protection law can also change, so periodic reviews with qualified professionals are essential.

Goldco does not offer tax or legal advice; customers should work with qualified professionals on creditor-protection questions.

FAQ

Are Gold IRAs protected from creditors?

Gold IRAs are protected to the same extent as other IRAs: federally up to the BAPCPA cap in bankruptcy (plus unlimited protection for properly segregated rollover funds) and under state law outside bankruptcy, which can range from unlimited to minimal.

How much IRA protection does federal law provide in bankruptcy?

As of April 1, 2025, federal bankruptcy law exempts up to about $1,711,975 across all traditional and Roth IRAs per person, with unlimited protection for rollover IRA balances traceable to ERISA-qualified plans if kept separate.

Are inherited Gold IRAs protected in bankruptcy?

Generally no. After Clark v. Rameker, inherited IRAs — including inherited Gold IRAs — do not qualify as "retirement funds" for federal bankruptcy exemption and may be fully exposed in bankruptcy unless state law provides a specific inherited-IRA exemption.

Which states offer unlimited protection for IRAs?

2026 surveys identify Florida, Texas, Connecticut, Illinois, Indiana, Iowa, Kansas, New Jersey, New Mexico, Oklahoma, Oregon, Washington, and Pennsylvania as providing full, uncapped protection for IRAs from most judgment creditors outside bankruptcy, and some also protect inherited IRAs.

How does California treat Gold IRAs in creditor situations?

California applies a needs-based test, protecting only IRA amounts "reasonably necessary" for the debtor's support at retirement; courts may allow creditors to reach balances deemed excess.

Do ERISA-qualified plans have better protection than Gold IRAs?

Yes in many cases. ERISA plans like 401(k)s generally enjoy stronger federal anti-alienation protection, shielding them from most creditors both inside and outside bankruptcy, while IRA protection outside bankruptcy depends on state law.

Does the physical metal in a Gold IRA change creditor protection?

No. Creditor-protection rules focus on the IRA wrapper, not the underlying asset. A Gold IRA is treated the same as any other self-directed IRA; physical metal mainly affects valuation and liquidation mechanics, not the exemption framework.

Can creditors reach a Gold IRA in divorce?

Yes. Domestic-relations orders and divorce judgments are exception creditors, and most exemption statutes do not shield IRAs from division in divorce. Courts can award part of a Gold IRA to a former spouse despite creditor-protection statutes.

Are Roth Gold IRAs treated differently from traditional Gold IRAs?

For creditor protection, most states treat Roth and traditional IRAs similarly, though a few states limit or exclude Roth IRAs from protection.

Does moving to Florida or Texas immediately improve Gold IRA protection?

Relocating to a full-protection state can strengthen future non-bankruptcy protection, but bankruptcy law uses a domicile look-back period, and prior claims or fraudulent-transfer concerns can complicate matters; legal advice is crucial before relying on a move.

How does this interact with inherited Gold IRA rules and RMDs?

Inherited Gold IRAs must still follow SECURE Act distribution rules, including the 10-year rule for many non-spouse beneficiaries, while creditor-protection rules determine whether those assets are exposed in lawsuits or bankruptcy; the article on Inherited Gold IRA Rules covers the distribution side in detail.

What professionals should Gold IRA owners consult about creditor protection?

Given the complexity, best practice is for Gold IRA owners to consult both a tax/financial advisor and a qualified asset-protection or bankruptcy attorney in the relevant state before making major rollover, consolidation, or relocation decisions.

Article reviewed and edited by Daniel — independent precious-metals retirement researcher.