Educational only: This article summarizes IRS rules, the Internal Revenue Code, FINRA/CFTC guidance, and published custodian schedules in general terms. It is not financial, tax, or legal advice. Fee figures are provider-specific, not industry averages. Customers should speak to a financial or tax advisor before making decisions. Goldco does not offer tax or legal advice. Past performance does not guarantee future results.

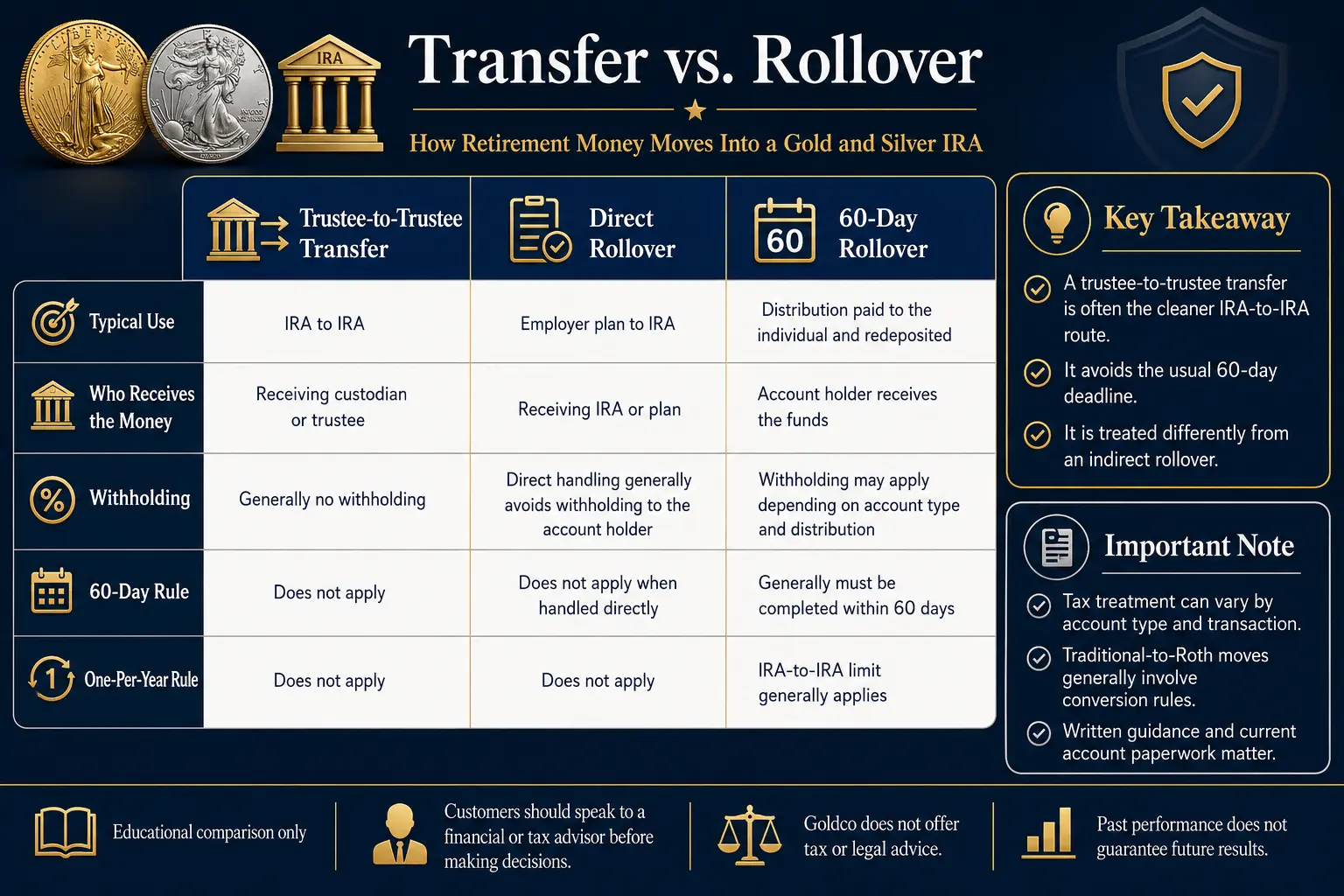

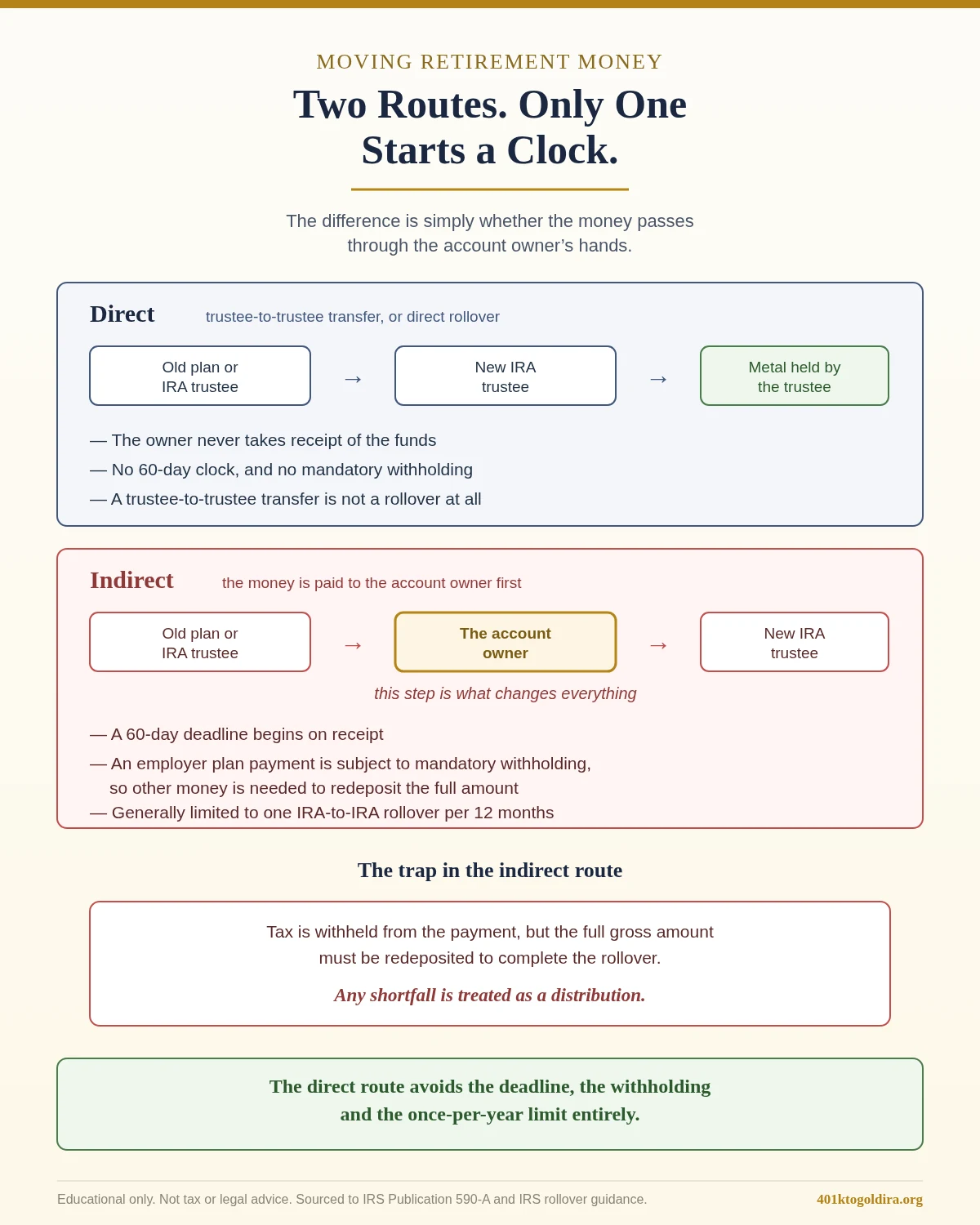

A trustee-to-trustee transfer moves an IRA to gold and silver without the account owner touching the money — so the 60-day deadline, the once-per-12-months limit, and 10% withholding do not apply. An indirect rollover triggers all three.

Source: IRS — Rollovers of Retirement Plan and IRA Distributions. The direct transfer route is why most Gold IRA moves avoid the errors that make a rollover taxable.

Key takeaways

- A transfer (trustee-to-trustee) is usually cleaner than a rollover: the owner never receives the funds, so no 60-day clock and no once-per-year limit.

- An indirect rollover starts the 60-day redeposit deadline, counts against the once-per-12-months IRA-to-IRA limit, and is generally subject to 10% withholding.

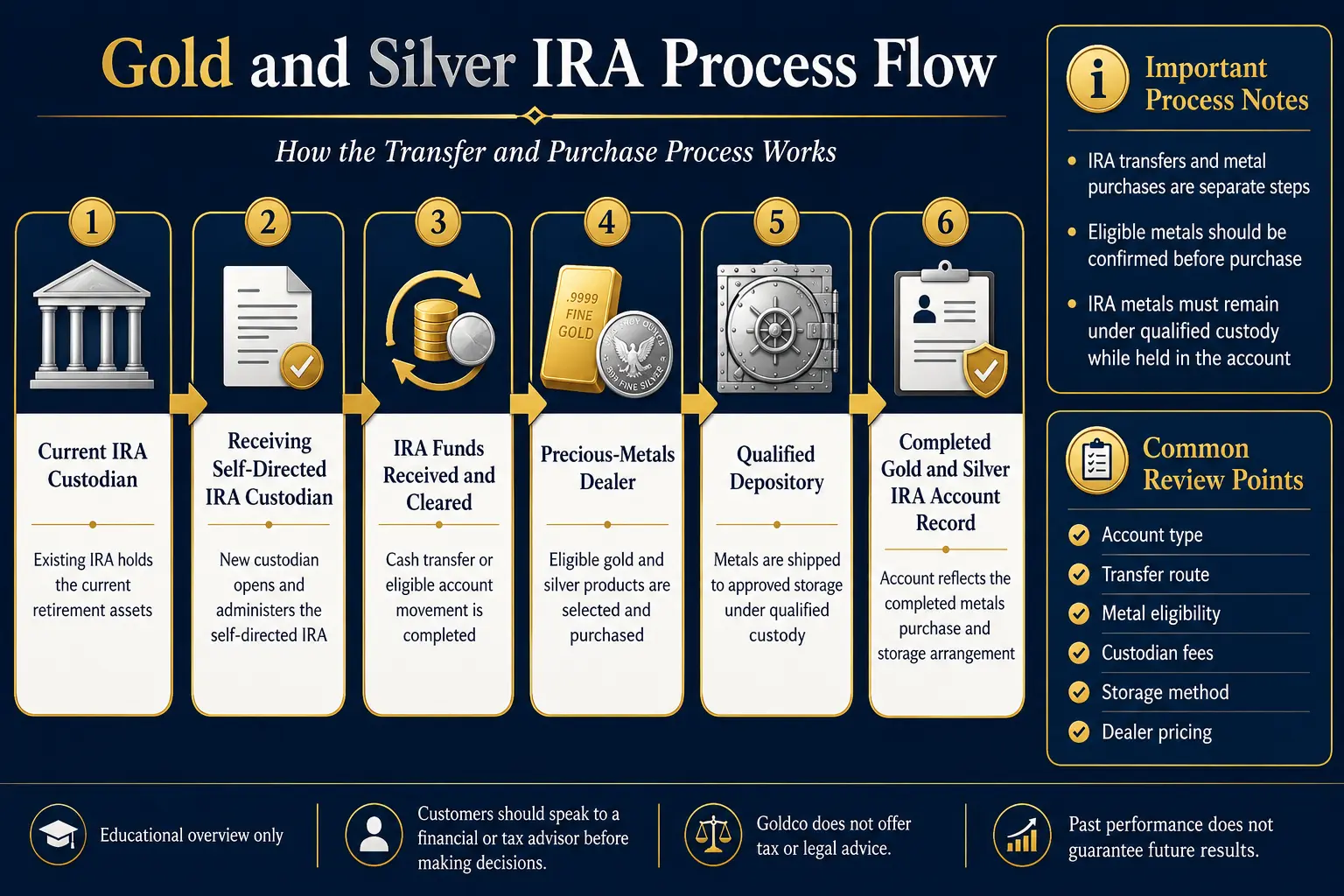

- The move funds a self-directed IRA first; the custodian then processes a metals purchase from a chosen dealer to an approved depository.

- Only eligible coins and bullion qualify, and metals must remain in the physical possession of a bank or approved trustee — not at home.

- "Tax-free IRA transfer" is accurate only when the direct-transfer rules are followed; a mishandled rollover can become a taxable distribution.

A Gold and Silver IRA is still an IRA. It follows the tax rules of the underlying traditional, Roth, SEP, SIMPLE, or inherited account. Physical metals add special rules for eligible products, trustee possession, depository storage, dealer pricing, and distributions. For an IRA-to-IRA move, a trustee-to-trustee transfer is usually the simpler route: the account owner does not receive the money, the 60-day deadline does not apply, and the IRS one-rollover-per-year rule does not apply.

Quick Answer: Transfer vs Rollover and What the Move Means

A gold and silver IRA transfer can use several routes. The correct route depends on the account sending the money.

| Route | Typical use | Owner receives the money? | Main federal timing rule |

|---|---|---|---|

| Trustee-to-trustee transfer | Existing IRA to another IRA | No | No 60-day deadline; no one-per-year limit |

| Direct rollover | Employer plan to an IRA | No (payable to the receiving IRA) | No 60-day deadline for the owner |

| 60-day rollover | Distribution paid to the individual and redeposited | Yes | Deposit generally required within 60 days |

| Roth conversion | Pretax IRA to a Roth IRA | Direct or indirect | Untaxed converted amount is generally taxable |

The IRS states that an IRA trustee-to-trustee transfer is not a rollover: it is not restricted by the one-rollover-per-year rule, and no federal income tax is withheld. A 60-day rollover is different — the money is paid to the individual and must generally be placed into an eligible retirement account within 60 days, and an IRA distribution paid to the individual is generally subject to 10% withholding unless a different election is made. The phrase "tax-free IRA transfer" is often used in marketing; more precisely, a properly completed same-type transfer can preserve tax-deferred or Roth status, but a traditional-to-Roth move is generally a taxable conversion to the extent it contains untaxed money. Customers should speak to a financial or tax advisor before making decisions involving a transfer, rollover, Roth conversion, distribution, or tax treatment. Goldco does not offer tax or legal advice.

Transfer IRA to Gold and Silver Through a Trustee-to-Trustee Transfer

A trustee-to-trustee transfer moves IRA funds or eligible IRA assets directly from the current financial institution to the receiving IRA trustee or custodian. The receiving institution may receive a wire, a check payable to the receiving trustee or custodian for the benefit of the IRA, or eligible assets transferred in kind when both institutions can support them. The IRS states that a check made payable to the receiving plan or IRA can qualify as a direct movement rather than a payment to the account owner, and no taxes are withheld.

Why the direct transfer is usually cleaner: the owner does not take possession of the retirement money, the 60-day clock does not start, the one-rollover-per-year rule does not apply, withholding generally does not reduce the transfer, and it is not treated as an ordinary IRA distribution. The IRS explains that direct transfers from one IRA trustee to another are not rollovers and are not limited in number by the one-per-year rule.

Cash transfer vs in-kind metals transfer

Most existing brokerage IRAs hold cash, stocks, bonds, mutual funds, or ETFs. If the receiving self-directed custodian cannot hold those assets, the current institution may need to liquidate them before sending cash — that liquidation occurs inside the sending IRA, so the owner should confirm trading costs, settlement timing, and whether to submit the transfer request before or after liquidation. Some custodians support direct in-kind transfers of metals already held in an IRA (STRATA Trust's April 2026 precious-metals transfer form lets a customer list IRA-held metals for in-kind transfer, including mint, quantity, and depositories — a provider-specific process, not proof every custodian accepts every metal). Existing personally owned coins cannot simply be placed into an IRA as a transfer; the IRA must acquire eligible metals through the account process.

The 60-Day Rollover and the One-Per-Year Rule

A 60-day rollover begins when an IRA or eligible retirement-plan distribution is paid to the individual, and the eligible amount generally must reach another eligible retirement account within 60 days. This route creates more moving parts than a transfer.

Withholding can create a shortfall

An IRA distribution paid to an individual is generally subject to 10% withholding unless the recipient elects out. If withholding occurs, the full distribution can be rolled over only when other funds replace the withheld amount within 60 days. Employer-plan distributions paid to the individual are generally subject to mandatory 20% federal withholding when they are eligible rollover distributions — a direct rollover to an IRA avoids that.

The one-rollover-per-year rule

An individual generally can make only one 60-day IRA-to-IRA rollover during any 12-month period, regardless of how many traditional, Roth, SEP, or SIMPLE IRAs are owned — the IRS aggregates those IRAs. The limit does not apply to trustee-to-trustee transfers, Roth conversions, plan-to-IRA rollovers, IRA-to-plan rollovers, or plan-to-plan rollovers. A failed second IRA-to-IRA rollover can create taxable income, possible early-distribution tax, an excess contribution, and an annual 6% tax while the excess remains. The IRS can waive the 60-day requirement in certain circumstances (automatic waiver, self-certification, or private letter ruling), but self-certification is not an IRS determination and the IRS can reach a different conclusion on examination — and the IRS cannot waive the separate one-per-year rule. The rollover guide covers these mechanics in more detail.

Required minimum distributions and distributions of excess contributions are not eligible for rollover. An older owner who must take an RMD should arrange that amount separately before transferring the remaining IRA. Customers should speak to a financial or tax advisor before using an indirect rollover, replacing withheld funds, addressing an RMD, or seeking a late-rollover waiver. Goldco does not offer tax or legal advice.

Which Gold and Silver Qualify for an IRA?

The IRS generally treats metals and coins as collectibles, and an IRA acquisition of a collectible is generally treated as a distribution unless an exception applies. Federal exceptions include certain gold, silver, and platinum coins described in federal coinage law; coins issued under the laws of a state; and gold, silver, platinum, or palladium bullion that meets the statutory fineness standard and remains in the physical possession of a bank or approved nonbank trustee (Internal Revenue Code Section 408(m)(3)).

The Entrust Group's published guide lists minimum standards of 99.5% gold, 99.9% silver, 99.95% platinum, and 99.95% palladium. Those figures are a named custodian's published interpretation of the federal bullion requirements — the receiving custodian should confirm the exact product before purchase, because statutory coin exceptions and custodian acceptance policies can differ from the general bullion percentages. Importantly, IRA eligibility addresses whether a product can be held, not whether the retail price, premium, or spread is reasonable: FINRA and the CFTC advise comparing the actual metal weight with spot, obtaining all fees in writing, and requesting the dealer's immediate buyback price. A custodian can accept a metal while remaining neutral about dealer pricing and suitability. First-time buyers can start with the beginner's guide.

Setting Up the Self-Directed IRA: Three Separate Roles

A self-directed IRA for gold and silver normally involves three independent operational roles:

- The IRA custodian or trustee establishes and administers the IRA, accepts transfer or rollover funds, processes written investment directions, maintains records, and reports transactions. The custodian usually does not choose the dealer or negotiate the price.

- The precious-metals dealer quotes and sells the gold or silver and should provide a detailed invoice identifying product, quantity, price, and destination. FINRA and the CFTC recommend asking for the current spot price, actual metal weight, retail price, premium, spread, buyback price, fees, and salesperson compensation — in writing before funds move.

- The depository receives, inspects, inventories, stores, and later ships the IRA-owned metals under the custodian's process. The metals must remain under qualified custody while held inside the IRA; personal possession can be treated as a distribution.

Entrust's published process requires an account, funding, dealer selection, depository selection, a buy-direction letter, dealer invoice, and depository election — the custodian wires funds to the dealer, the dealer ships to the depository, and the depository audit is reconciled with the invoice before the metals are recorded. For storage differences, see segregated versus commingled storage.

Costs to Confirm in Writing Before Transferring

No universal Gold and Silver IRA fee can be verified — costs depend on the custodian, depository, dealer, metal, account value, transaction method, and exit route. A written cost review should include account establishment; annual administration or recordkeeping; percentage-based charges; commingled or segregated storage; insurance; wire or check fees; the dealer premium above spot; the dealer buyback spread; shipping; purchase/sale/exchange processing; cash or in-kind distribution; and account termination.

Provider-specific examples: as of July 2026, STRATA's public precious-metals fee page lists a $125 annual account fee, $100 annual commingled storage, and $175 annual segregated storage (subject to depository exceptions). Entrust's January 2026 schedule lists a $50 establishment fee, $219 annually for one non-cash asset under $50,000, plus 0.17% of value above $50,000, and $0 for a precious-metals purchase/sale/exchange while depository storage and shipping can still apply. These are provider-specific observations, not market averages, and they do not include the dealer's metal premium or future buyback spread. Model flat vs value-based structures on the fee calculator.

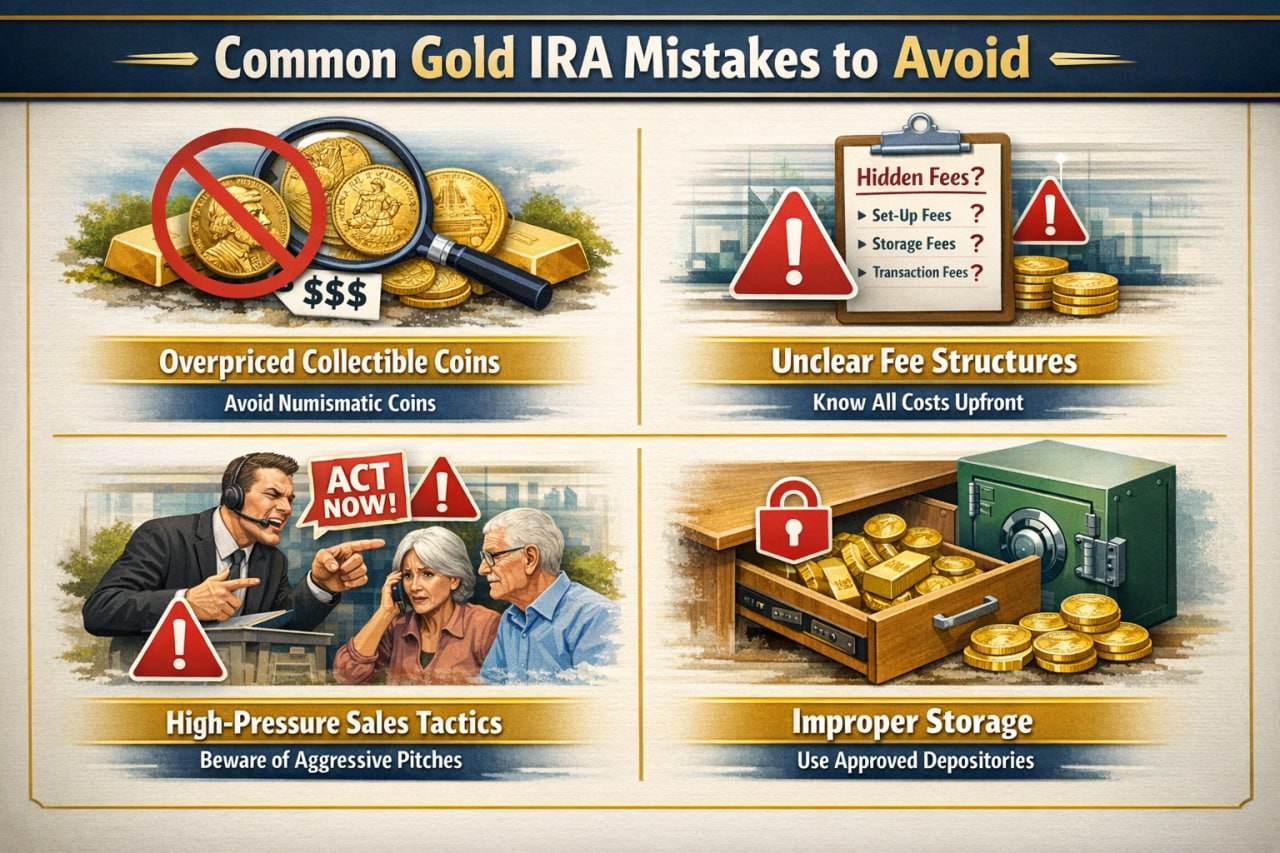

Common Transfer Mistakes

- Treating "transfer" and "rollover" as identical. A trustee-to-trustee transfer is not a rollover for the one-per-year rule; a 60-day rollover is a distribution received and redeposited. The paperwork and tax risk differ.

- Opening the wrong tax type. A traditional IRA transfer normally goes to another traditional IRA to preserve pretax status; moving untaxed money into a Roth is generally a taxable conversion.

- Letting the check be payable to the individual. A check payable to the receiving custodian preserves direct handling; one payable to the individual can begin the 60-day process and withholding.

- Missing the one-rollover-per-year limit. It applies across all of an individual's IRAs, not per account. Transfers are exempt.

- Rolling over an RMD. An RMD is not eligible for rollover — handle it separately before the balance moves.

- Buying collectibles or unsupported products. A dealer description does not replace custodian approval; confirm the exact coin or bar against the federal exceptions.

- Personal or home storage. IRA metals must remain under qualified possession; personal possession generally creates a distribution.

- Comparing only custodian fees. The dealer premium and buyback spread can matter more than a modest setup fee.

- Transferring the entire IRA without a liquidity plan. Physical metals may require dealer liquidation or in-kind distribution before cash is available.

A Gold and Silver IRA should be framed as one possible diversification tool, not a fix for an incomplete retirement plan.

Step-by-Step Transfer Checklist

- Define the purpose and amount. Document the expected role, amount, holding period, and effect on the rest of the portfolio.

- Identify the sending account. Confirm whether it is traditional, Roth, SEP, SIMPLE, inherited, or an employer plan. A SIMPLE IRA can have special transfer restrictions during the first two years of participation.

- Choose a self-directed IRA custodian that accepts physical gold and silver, supports the existing account type, works with the intended depository, and provides a current fee schedule.

- Open the matching receiving IRA so the registration and tax character match the intended transaction. Review any Roth conversion separately.

- Request a trustee-to-trustee transfer using the receiving custodian's form; direct the sending institution to remit funds to the receiving custodian for the benefit of the IRA.

- Arrange liquidation if the sending custodian requires cash; confirm settlement timing and whether any assets should remain.

- Confirm cleared funds. A mailed check can be subject to a hold (STRATA's current form states checks may be held up to seven business days; a wire is faster — a provider-specific procedure).

- Select the dealer, metals, and depository. Confirm exact products with the custodian and obtain the invoice, spot comparison, premium, commissions, and same-day buyback price in writing.

- Submit the investment direction. The custodian releases funds using the direction, dealer invoice, and depository information; the dealer ships to the depository.

- Verify the completed transaction. Review the custodian statement and depository confirmation — product descriptions, quantities, storage method, cash balance, fees, and beneficiary information.

The best Gold IRA companies page supports provider research, and the quiz can organize questions before the transfer begins. Customers should speak to a financial or tax advisor before completing any transfer, rollover, conversion, liquidation, or metal purchase. Goldco does not offer tax or legal advice.

Frequently Asked Questions

Is an IRA transfer to gold and silver taxable?

A properly completed trustee-to-trustee transfer between compatible IRA types generally does not create a taxable distribution. A traditional IRA to Roth IRA move is generally a taxable conversion to the extent it contains untaxed money.

Does the 60-day rule apply to a direct IRA transfer?

No. The IRS states that a trustee-to-trustee transfer is not subject to the 60-day requirement because the account owner does not receive the funds.

Does the one-rollover-per-year rule apply to transfers?

No. The rule applies to 60-day IRA-to-IRA rollovers. It does not apply to trustee-to-trustee transfers, Roth conversions, or plan-to-IRA rollovers.

What gold and silver can an IRA hold?

Federal law permits certain statutory coins and qualifying bullion under the collectibles exception. Entrust publishes minimum standards of 99.5% for gold and 99.9% for silver, but the custodian should approve each exact product before purchase.

Can existing personal gold or silver be added to an IRA?

Personal metals cannot simply be contributed as an IRA transfer. The IRA must acquire eligible metals through the custodian-controlled purchase process, and personal property must remain separate.

Can IRA metals be stored at home?

Federal guidance states that qualifying bullion must remain in the physical possession of a bank or approved nonbank trustee while held inside the IRA. Personal possession can be treated as a distribution.

Update Log

- 2026: Initial publication. Sourced to IRS rollover/transfer guidance, Topics 413/451/609, Publication 590-A/590-B, Announcement 2014-32 (one-per-year rule), Internal Revenue Code Section 408, FINRA/CFTC guidance, and published STRATA Trust and Entrust Group schedules. Rules and provider figures change — reverify before acting.

Sources

- Internal Revenue Service. Rollovers of Retirement Plan and IRA Distributions.

- Internal Revenue Service. Tc451.

- Internal Revenue Service. Tc413.

- Internal Revenue Service. Verifying rollover contributions to plans.

- Internal Revenue Service. Publication 590-A (Contributions to IRAs).

- Internal Revenue Service. Publication 590-B (Distributions from IRAs).

- Internal Revenue Service. Retirement plans faqs relating to waivers of the 60 day rollover requi.

- Internal Revenue Service. A 14 32.

- Internal Revenue Service. Retirement Plans FAQs Regarding IRAs.

- Internal Revenue Service. Investments in Collectibles in IRA Accounts.

- U.S. Government Publishing Office. 26 U.S.C. § 408 (govinfo).

- Internal Revenue Service. Simple ira withdrawal and transfer rules.

- FINRA. 10 Things to Ask Before Buying Physical Gold, Silver or Other Metals.

- The Entrust Group. Precious Metals FAQs 2017.

- The Entrust Group. Master Account Fee Schedule Jan 26.

- STRATA Trust. 2026 IRA Transfer Request Precious Metals.

- STRATA Trust. Strata fees.

Article reviewed and edited by Daniel M. — editor, 401kToGoldIRA.org. Sourced to IRS.gov, the Internal Revenue Code, FINRA, the CFTC, and published custodian schedules; educational only, not tax or legal advice.