Educational only: This guide summarizes IRS, Investor.gov, Social Security Administration, FINRA, and independent research in general terms. It is not financial, tax, or legal advice, and it does not forecast markets or returns. Customers should speak to a financial or tax advisor before making decisions. Goldco does not offer tax or legal advice. Past performance does not guarantee future results.

Quick Answer: The Two-Decade Horizon at 45

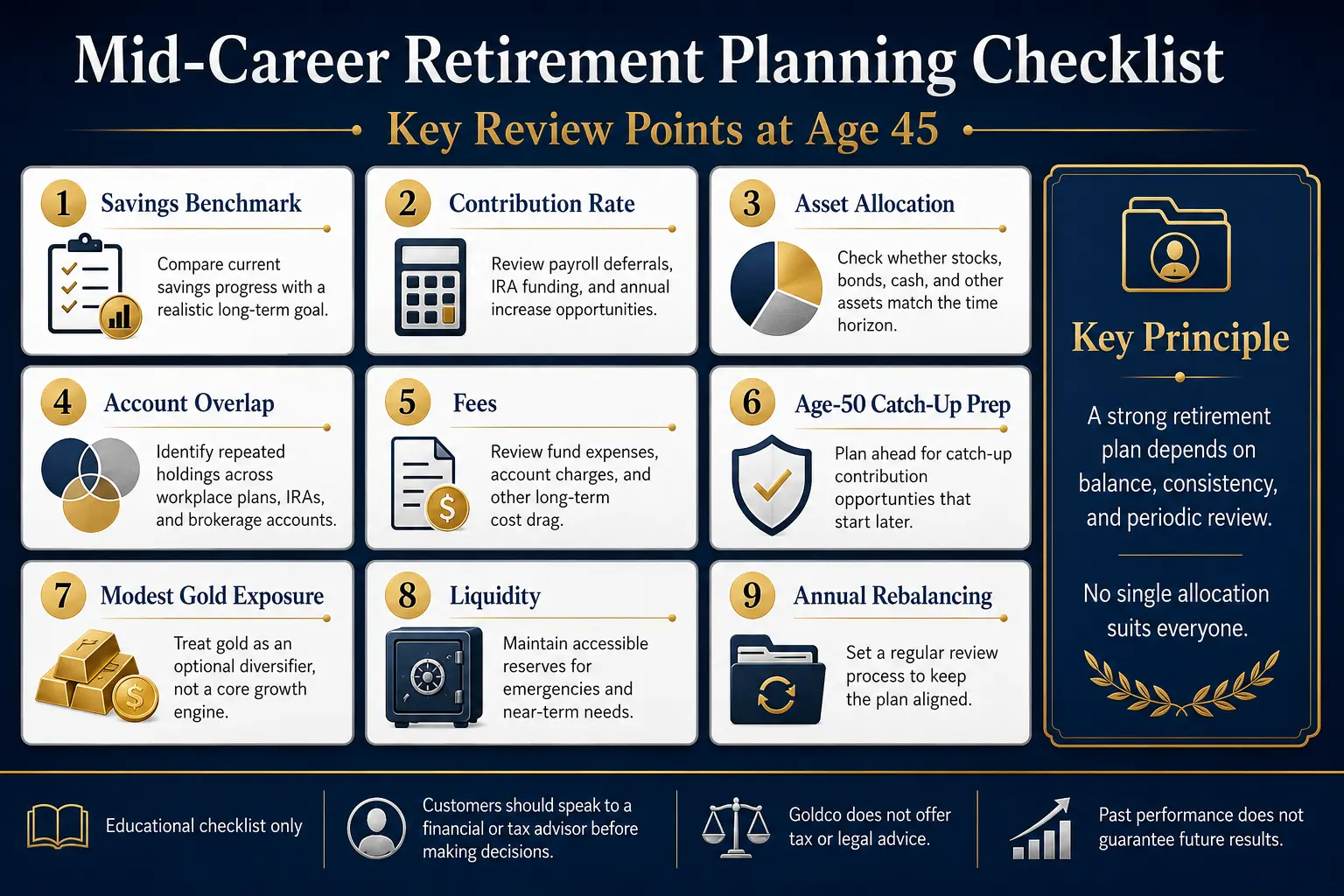

A person planning retirement at 45 still has several major advantages: about two decades remain for investment gains to compound; earnings may still rise during later career years; contribution rates can be increased before retirement; age-50 catch-up contributions are still five years away; the asset mix can be adjusted gradually instead of all at once; and retirement timing, spending goals, and Social Security strategy are not yet fixed. The main planning task is not finding one asset that solves retirement — it is building a system in which savings rate, asset allocation, costs, taxes, and risk work together.

Investor.gov states that asset allocation should reflect both time horizon and risk tolerance. A longer horizon can provide more time to recover from market declines, but the appropriate mix remains personal and depends on the saver's ability and willingness to accept losses (Investor.gov: Asset Allocation and Diversification). At 45, gold can be tested as an optional supporting allocation. It should not be treated as a certain inflation solution or as the main source of long-term compounding. Customers should speak to a financial or tax advisor before making decisions involving contributions, allocation, retirement income, or account changes.

What Popular Mid-Career Retirement Pages Cover—and Often Miss

An editorial review of prominent retirement-planning pages from Fidelity, Schwab, and Vanguard found a common focus on salary-based savings targets, contribution rates, tax-advantaged accounts, retirement-age assumptions, and broad diversification. Fidelity's current mid-career guidance uses a rough benchmark of four times salary by age 45 and six times salary by age 50. Schwab organizes retirement planning by decade, while Vanguard emphasizes goals, account choices, and long-term investing. These pages provide useful foundations, but a practical age-45 plan also needs several details that broad guides may not emphasize:

- The five-year bridge before catch-up eligibility begins.

- Overlap among 401(k), IRA, brokerage, and target-date fund holdings.

- The effect of fees on a 20-year plan.

- The difference between a savings benchmark and an actual retirement-income target.

- The role of optional assets such as gold without displacing core diversification.

- A transition plan for the next checkpoint at age 50 or 55.

A salary multiple can serve as a progress marker, but it is not a personal requirement. Retirement age, pension income, Social Security, housing costs, family obligations, taxes, and desired spending can change the amount needed.

Retirement Planning at 45 With Gold Starts With Growth and Compounding

Twenty Years Is Still a Long Investment Period

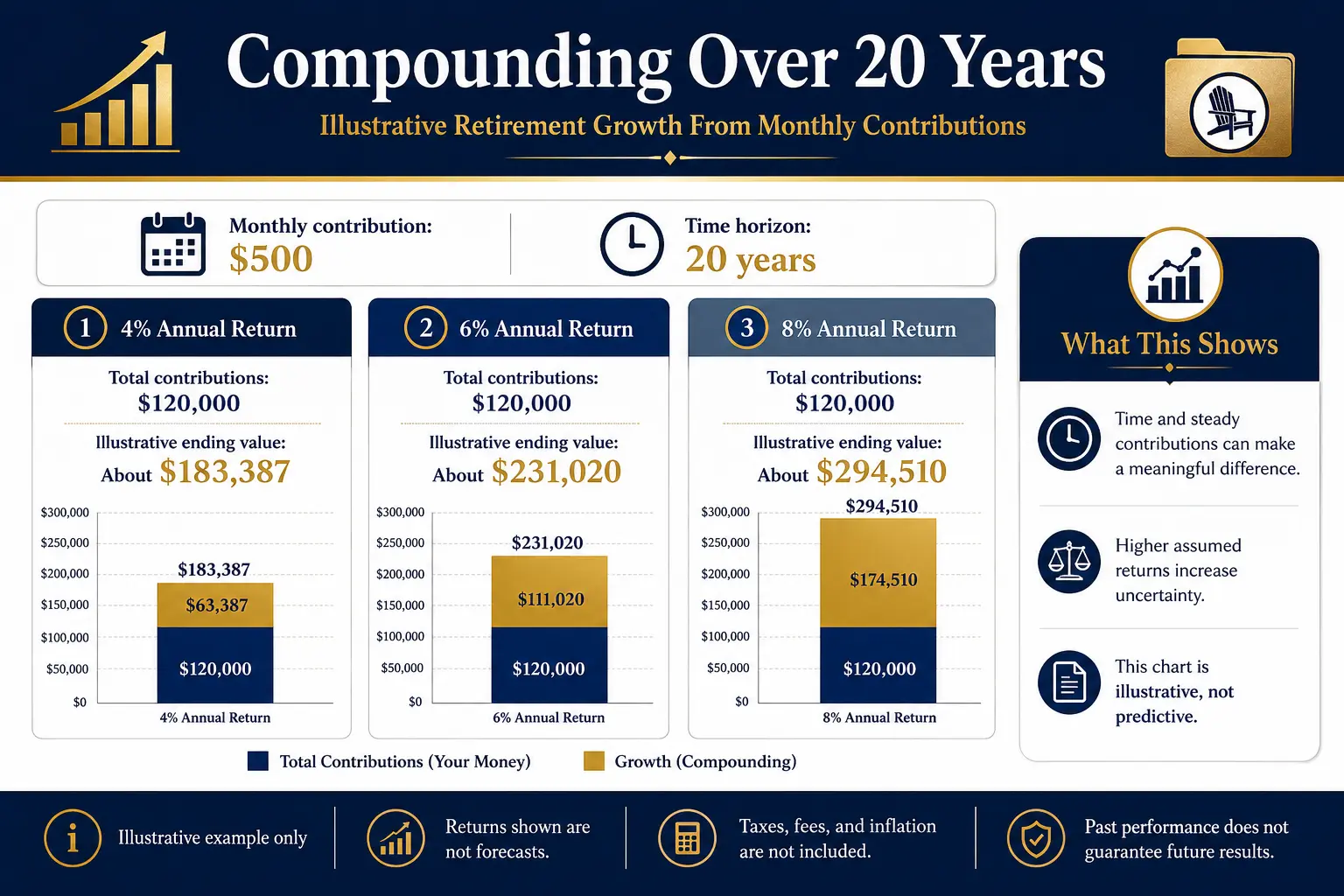

Compound growth occurs when returns are earned on both the original principal and earlier gains. Investor.gov provides a compound-interest calculator that allows an initial amount, monthly contribution, time period, estimated rate, and variance range to be tested. A 20-year horizon can make contribution consistency more important than a single early account balance. The table below is a mathematical illustration. It assumes $500 deposited at the end of each month for 20 years, with monthly compounding. It excludes taxes, fees, and inflation and does not predict market returns.

| Illustrative annual return | Total contributions | Ending value after 20 years |

|---|---|---|

| 4% | $120,000 | About $183,387 |

| 6% | $120,000 | About $231,020 |

| 8% | $120,000 | About $294,510 |

The gap between the scenarios shows the combined effect of time and returns. It does not mean a higher return can be selected without accepting greater uncertainty or risk.

Savings Rate Can Be More Controllable Than Market Returns

Market returns cannot be scheduled. Contributions, payroll deferrals, and automatic annual increases are more controllable. Fidelity's general guideline is to save about 15% of pretax income each year, including employer contributions, while working toward its broader age-based benchmarks. Fidelity states that these guidelines depend on assumptions about retirement age, savings history, and future income needs. A mid-career plan can test several contribution paths: the current percentage with no increase; a one-percentage-point annual increase; a larger increase after a debt is repaid; directing part of future raises or bonuses to retirement accounts; or adding IRA contributions when workplace-plan contributions are already strong. The purpose is not to force one savings rate — it is to show how the next 20 years change when contributions rise gradually.

A Benchmark Is a Diagnostic Tool, Not a Verdict

Fidelity's current roadmap suggests about four times salary by age 45, six times by age 50, eight times by age 60, and ten times by age 67. Those figures are provider guidelines based on stated assumptions, not government standards. A household below a benchmark can still improve the plan through higher contributions, a later retirement date, lower planned spending, pension income, housing changes, or other adjustments. A household above a benchmark can still face risk if the portfolio is concentrated, expensive, or disconnected from expected spending.

Balanced Diversification at Mid-Career

Start With the Full Household Portfolio

Diversification mid career should be measured across every account, not one statement at a time. The review should include workplace plans, traditional and Roth IRAs, taxable brokerage accounts, cash reserves, employer stock, pensions, real estate intended to support retirement, and existing physical metals or commodity exposure. Several diversified-looking funds may hold many of the same large companies, and a target-date fund combined with extra stock and bond funds can also create unintended overlap. Investor.gov states that diversification spreads money among and within asset categories, while asset allocation divides investments among categories such as stocks, bonds, and cash; diversification can reduce concentration risk but cannot prevent all losses.

Keep the Time Horizon Connected to the Asset Mix

A 20-year horizon can support meaningful growth exposure, but age alone does not determine the allocation. Risk capacity depends on job stability, emergency reserves, debt obligations, pension or Social Security expectations, family expenses, health, ability to delay retirement, and emotional response to market declines. Investor.gov explains that target-date funds commonly hold more stocks earlier and shift toward more bonds as the target date approaches, and warns that funds with the same target year can follow different glide paths and hold different mixes. A saver already holding a target-date fund should check whether adding gold, stock funds, or bond funds changes the intended glide path.

Separate Growth, Stability, and Liquidity

A clear retirement allocation gives each asset a job. Diversified stocks can support long-term growth but can decline sharply. Bonds can provide income and reduce some volatility, but they carry interest-rate, credit, and inflation risks. Cash can cover emergencies and near-term needs but may lose purchasing power. Gold can serve as an optional diversifier but has price volatility and no direct yield. The allocation should be judged by how the parts work together, not by whether one asset performed well recently.

Where a Modest Gold Allocation May Fit

Gold Is a Diversifier, Not a Core Growth Engine

Gold does not pay a direct yield. Its financial return depends on price changes after purchase, holding, storage, account, and selling costs. The World Gold Council also notes that the absence of yield can make gold less attractive when investors require steady income or when competing assets offer higher coupons or dividends. Physical precious metals can also involve dealer premiums, spreads, storage, insurance, and administrative charges. FINRA recommends comparing spot value, retail price, all fees, and the amount available from an immediate resale. For a 20-year horizon retirement plan, gold may support diversification. It should not be expected to compound like a productive business that reinvests earnings or pays dividends.

The Evidence Supports Caution

World Gold Council research argues that gold can improve diversification and historical risk-adjusted results in hypothetical portfolios. Its 2026 market primer states that its analysis supports a 5% strategic allocation, with a studied range of 2% to 10% depending on objectives. The World Gold Council represents the gold industry, and the ranges come from historical and model-based analysis rather than a universal retirement rule. Independent research is more cautious: the NBER paper The Golden Dilemma concluded that gold may hedge inflation over extremely long horizons but is unreliable over practical investment periods, and a CFA Institute analysis covering 1979 through 2024 found that gold's relationship with inflation was unstable, with some periods of stronger protection and other periods with little relationship. The combined evidence supports a modest, scenario-based approach rather than a fixed rule.

Test Several Allocations Instead of Choosing One Number

A gold allocation age 45 review can compare several scenarios: no dedicated gold allocation; a small allocation; a moderate allocation within the range studied by a named source; or a larger allocation that reveals the effect of concentration. These scenarios are not recommendations. The comparison should show the effect on stock and bond exposure, expected portfolio volatility, the lack of direct income from gold, dealer and account costs, liquidity, rebalancing rules, tax and custody issues, and the amount of retirement growth being displaced. The how much gold should be owned in retirement guide provides a broader allocation framework, and the Gold IRA calculator can help organize account and cost assumptions. Customers should speak to a financial or tax advisor before making decisions involving retirement allocation, contributions, rollovers, or withdrawals.

Gold IRA at 45: Account Rules Matter

A Gold IRA is a self-directed IRA holding qualifying precious metals under applicable tax and custody rules. The IRS states that retirement accounts generally cannot hold collectibles, with limited exceptions for certain coins and precious metals meeting specific requirements. Product eligibility and qualified custody must be confirmed before purchase. The decision should include the custodian, depository, storage method, dealer pricing, annual charges, liquidation process, and the assets being sold to fund the purchase. Goldco does not offer tax or legal advice.

Contribution and Catch-Up Planning at 45

Current 2026 Contribution Limits

For 2026, the basic employee elective-deferral limit for most 401(k), 403(b), governmental 457 plans, and the federal Thrift Savings Plan is $24,500. The general IRA contribution limit is $7,500, subject to compensation and eligibility rules. A 45-year-old is not yet eligible for age-50 catch-up contributions. That leaves about five years to build a higher regular contribution rate before catch-up limits become available. At age 50 or older, the 2026 catch-up limit for most applicable workplace plans is $8,000, and the total IRA limit is $8,600. Employees ages 60 through 63 have a higher 2026 workplace-plan catch-up limit of $11,250 when the plan and rules apply.

Beginning in 2026, the IRS states that catch-up contributions generally must be Roth contributions for certain participants whose prior-year wages from the plan sponsor exceeded $150,000, when the plan has the relevant Roth feature. Plan documents and payroll records should be checked before relying on the rule. Annual limits can change; current IRS guidance should be reviewed each year.

Catch-Up Contributions Are a Tool, Not the Main Plan

Catch-up planning 45 should not wait until age 50. A stronger five-year runway can include:

- Capturing the full employer match when available.

- Reviewing plan fees and investment options.

- Increasing payroll contributions gradually.

- Coordinating traditional and Roth tax treatment.

- Using an IRA when eligible and appropriate.

- Building enough liquidity to avoid retirement-account withdrawals.

- Reducing high-cost debt that competes with savings.

Tax treatment depends on income, filing status, workplace coverage, plan design, and future tax law. Customers should speak to a financial or tax advisor before making decisions involving contribution amounts, Roth treatment, deductions, rollovers, or account selection. Goldco does not offer tax or legal advice.

Revisiting the Plan Periodically

A 20-year plan should be reviewed without reacting to every market move. Investor.gov notes that many financial professionals use calendar-based rebalancing intervals such as every six or twelve months, and that a review should consider changes in financial goals, time horizon, and risk tolerance. A practical annual review can cover the current retirement balance and contribution rate, progress toward a personal income goal, stock/bond/cash/gold percentages, fees across every account, beneficiary information, emergency reserves and debt, target retirement age, expected Social Security and pension income, insurance and family responsibilities, and rebalancing needs. A separate review may be useful after a job change, marriage, divorce, inheritance, major health event, or large income change.

The next age-based checkpoint can be planned in advance. The retirement planning at 55 with precious metals guide addresses the shorter horizon and greater need for income and withdrawal planning. The 4% rule and Gold IRA guide examines how metals interact with retirement spending assumptions. The Gold IRA quiz can help organize research questions before a company discussion.

Frequently Asked Questions

How much retirement savings should exist at age 45?

Fidelity's current guideline suggests about four times annual salary by age 45. That is a planning benchmark based on provider assumptions, not a government requirement or personal verdict. Retirement age, expected spending, pensions, Social Security, housing, and taxes can change the appropriate target.

Is age 45 too early for a Gold IRA?

Age 45 is not automatically too early or too late. The relevant questions are whether gold fits the full allocation, whether the account costs are reasonable, whether the metals qualify, and whether the custodian and storage arrangement follow IRS rules.

How much gold should a 45-year-old hold?

No single percentage suits every saver. World Gold Council research has studied allocations from 2% to 10% and has highlighted 5% in some hypothetical portfolios, but that is industry-sponsored modeling rather than a personal rule. Independent research finds that gold's inflation and diversification record changes by period.

Can catch-up contributions be made at age 45?

No age-50 catch-up contribution applies at 45. Under 2026 rules, the general workplace-plan and IRA limits apply until the saver becomes eligible under the age rules.

Can twenty years still make a major difference?

Twenty years allows recurring contributions and investment returns to compound. The result depends on contribution level, market returns, fees, taxes, inflation, and withdrawals. Investor.gov provides calculators for testing different assumptions rather than relying on one forecast.

Should gold replace stocks at age 45?

Gold should not automatically replace diversified stocks. Gold pays no direct yield and can be volatile, while stocks can provide ownership in operating companies and long-term growth exposure. A portfolio decision should consider the role, amount, cost, and effect on the full allocation.

Conclusion

Retirement planning at 45 still has time on its side. Two decades can support meaningful compounding, higher contribution rates, balanced diversification, and gradual risk adjustments. The strongest plan begins with the retirement-income goal, contribution path, full household allocation, and costs. Gold may fit as a modest diversifier; it should not be treated as a core growth engine, a certain inflation hedge, or a substitute for liquidity and income planning. Industry research has found benefits in selected hypothetical portfolios, while independent research shows that gold's results are period-dependent. At age 45, the most important question is not whether gold is present — it is whether every asset has a clear role and whether the plan is strong enough to be reviewed, measured, and adjusted over the next 20 years. Customers should speak to a financial or tax advisor before making decisions involving retirement allocation, contributions, rollovers, withdrawals, or taxes. Goldco does not offer tax or legal advice.

Sources

- Social Security Administration. Full Retirement Age for People Born in 1960 or Later.

- Investor.gov. Asset Allocation and Diversification.

- Investor.gov. Beginners' Guide to Asset Allocation, Diversification, and Rebalancing.

- Investor.gov. Compound Interest Calculator.

- Investor.gov. Target Date Funds.

- Investor.gov. Target Date Funds — Investor Bulletin.

- Investor.gov. Is It Time to Rebalance an Investment Portfolio?

- Fidelity. Retirement Planning: What to Consider in the 40s.

- Fidelity. Four Retirement Savings Guidelines.

- Charles Schwab. Retirement Planning by the Decade: A Savings Guide.

- Vanguard. Planning for Retirement.

- Internal Revenue Service. 401(k) Limit Increases to $24,500 for 2026; IRA Limit Increases to $7,500.

- Internal Revenue Service. Retirement Topics — IRA Contribution Limits.

- Internal Revenue Service. Retirement Topics — Catch-Up Contributions.

- Internal Revenue Service. Retirement Plan Investments FAQs.

- Internal Revenue Service. Investments in Collectibles in Individually Directed Qualified Plan Accounts.

- FINRA. 10 Things to Ask Before Buying Physical Gold, Silver or Other Metals.

- World Gold Council. Gold Market Primer: Market Size and Structure.

- World Gold Council. Gold as a Strategic Asset: Portfolio Impact and Risk/Reward.

- World Gold Council. Rates Pose Risks but Also Unlock Opportunities for Gold.

- National Bureau of Economic Research. The Golden Dilemma.

- CFA Institute. Gold and Inflation: An Unstable Relationship.

Article reviewed and edited by Daniel M. — editor, 401kToGoldIRA.org. Sourced to the IRS, Investor.gov, the Social Security Administration, FINRA, and independent research; educational only, not tax or legal advice, and not a forecast of returns.

Further Reading

How Much Gold Should Investors Own in Retirement?A framework for matching allocation to goals, liquidity, and risk.

How Much Gold Should Investors Own in Retirement?A framework for matching allocation to goals, liquidity, and risk. Retirement Planning at 55 With Precious MetalsThe shorter horizon: income, withdrawals, and catch-up contributions.

Retirement Planning at 55 With Precious MetalsThe shorter horizon: income, withdrawals, and catch-up contributions. The 4 Percent Rule and Gold IRAsHow physical metals interact with retirement withdrawal planning.

The 4 Percent Rule and Gold IRAsHow physical metals interact with retirement withdrawal planning.