Educational only: This article summarizes Federal Reserve research, BLS, Investor.gov, FINRA, and independent studies in general terms. It is not financial, tax, or legal advice, and it does not forecast markets. Customers should speak to a financial or tax advisor before making decisions. Goldco does not offer tax or legal advice. Past performance does not guarantee future results.

Tariffs can raise prices in some categories, reduce profits for some businesses, support other firms, and increase short-term volatility. They do not produce one uniform result across the economy or stock market. A calm retirement response focuses on diversification, liquidity, rebalancing, and withdrawal planning rather than trying to predict the next trade announcement.

Quick Answer: How Tariffs Can and Cannot Affect a Retirement Portfolio

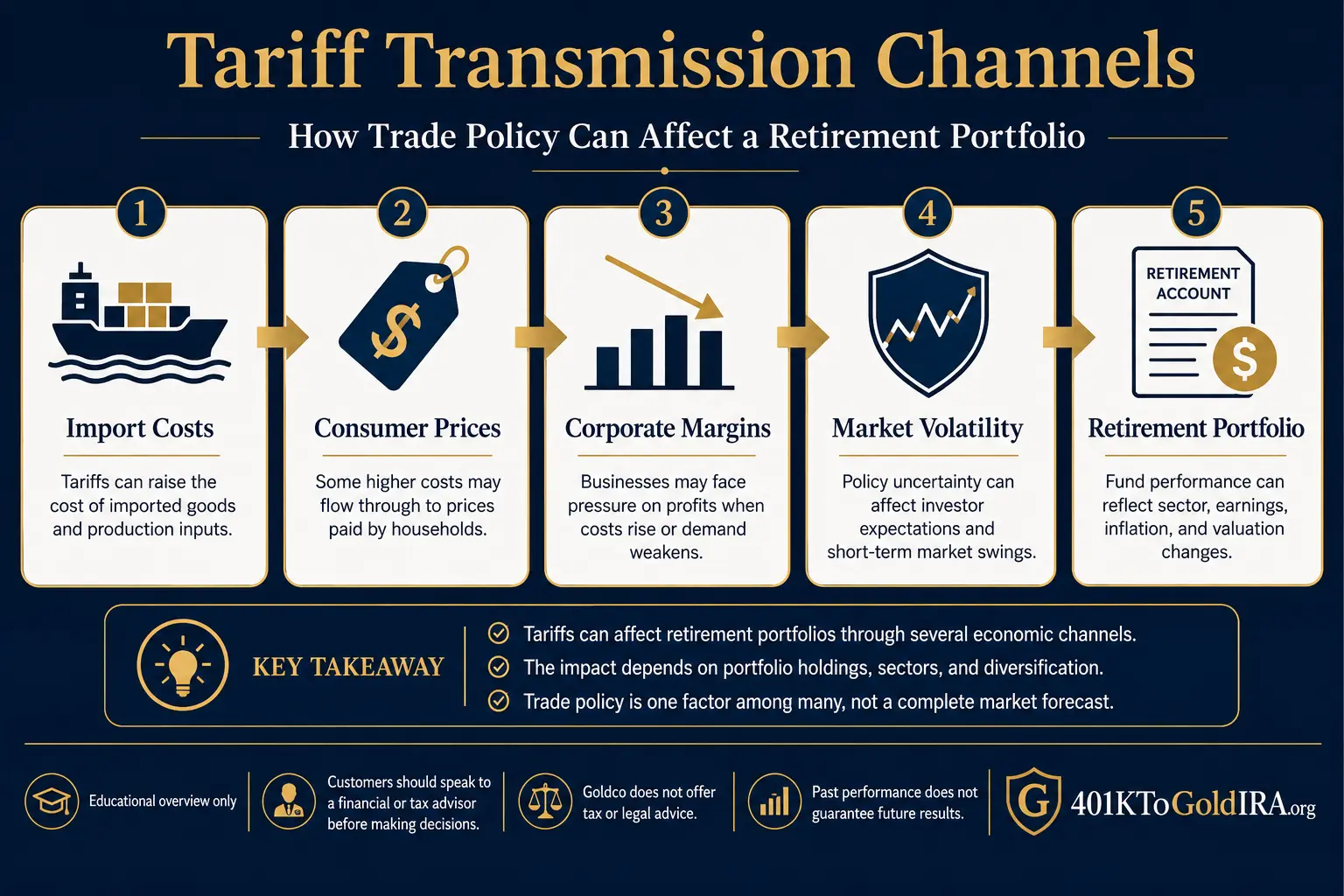

Tariffs are charges applied to imported goods. The importing business generally pays the charge at the border, but the economic cost can be divided among importers, suppliers, customers, workers, and shareholders through changing prices, margins, wages, purchasing patterns, and profits. The Bureau of Labor Statistics explains that tariffs are not entered directly into the Consumer Price Index — they can still affect CPI indirectly when imported-goods costs influence the prices charged by producers and retailers, and tariff effects can spill into other goods and industries. For a retirement account, the main channels are:

- Higher prices can reduce household purchasing power.

- Higher input costs can pressure company profit margins.

- Policy uncertainty can delay hiring and capital spending.

- Market expectations can reprice stocks, bonds, currencies, and sectors.

- Retaliatory measures can affect exporters and global companies.

- Volatility near retirement can create sequence-of-returns risk when withdrawals are underway.

A 401(k) itself is not a single investment. Participant-directed plans offer options with different risk and return characteristics, and the account holder selects among the allowed choices. A broadly diversified target-date fund may react differently from a concentrated U.S. stock fund, employer-stock position, international fund, bond fund, or sector fund — so the first step is to identify what the account actually owns. Customers should speak to a financial or tax advisor before making decisions involving asset allocation, retirement income, account changes, or taxes. Goldco does not offer tax or legal advice.

Channel 1: The Price Channel

The first channel is the cost of imported goods and imported production inputs. A tariff can raise the landed cost of a finished product, such as an appliance or electronic device, and the cost of parts, machinery, metals, chemicals, and other inputs used by domestic companies. The final consumer-price effect depends on whether the foreign supplier lowers its price, the importer absorbs part of the tariff, the business raises retail prices, the business switches suppliers, customers buy fewer units or substitute, and how domestic competitors respond. A tariff rate cannot be treated as an automatic equal-percentage increase in the retail price.

What current Federal Reserve research found

A Federal Reserve Board study published in April 2026 found statistically significant price increases in consumer-goods categories with greater exposure to tariffs imposed in 2025, estimating that those tariffs raised core-goods Personal Consumption Expenditures prices by 3.1% through February 2026 and added about 0.8% to the broader core PCE price level, with effects building gradually rather than all at once. A separate Fed Board paper on household spending found partial pass-through and estimated that, at the average tariff-exposure increase in its sample, prices rose by roughly 1% to 2% while spending fell by about 4%. Those estimates apply to a specific tariff period, dataset, and method — they are not a permanent formula for future trade policy. The general conclusion: tariffs can contribute to price increases, but the size and timing vary.

Tariff-related inflation pressure can appear in everyday imported consumer goods, vehicles and parts, home-maintenance materials, medical devices, business costs that later affect service prices, and portfolio withdrawals needed to cover higher expenses — and a retiree with a fixed pension or fixed withdrawal may feel more pressure than a worker whose wages can adjust. Tariffs are only one inflation source; energy, housing, wages, demand, supply, and monetary conditions also matter. The retirement purchasing-power guide explains broader inflation tools.

Channel 2: Corporate Earnings and Equity Markets

Stocks represent ownership interests in companies, and stock prices can respond when investors change their expectations for future revenue, costs, profits, interest rates, and risk. Tariffs can affect earnings through higher costs for imported inputs, lower sales when retail prices rise, supply-chain changes, retaliatory tariffs on exports, currency movements, delayed capital spending, competitive gains for firms with less import exposure, and pricing power that lets some firms pass costs on. The result can differ even among companies in the same industry.

Market expectations can move before reported earnings

A San Francisco Fed event study of the major U.S. tariff announcement of April 2, 2025 found broad repricing across sectors, credit markets, currencies, and countries, concluding that market participants interpreted the announcement as likely to reduce corporate profits over a longer period in both the U.S. and other countries. That study analyzed one announcement and the market's immediate interpretation — it does not prove that every tariff announcement produces the same result or that initial price moves remain permanent. Markets can later reverse when policies change, exemptions expand, negotiations progress, earnings exceed expectations, or investors reassess the effects.

The Richmond and Atlanta Federal Reserve Banks' CFO Survey reported in June 2025 that 40% of respondents viewed tariffs and trade policy as a pressing concern; concerned firms reported stronger expected input-cost growth and weaker expected real revenue growth, and more than four in ten financial executives reported postponing, reducing, delaying, or canceling some planned investment during the first half of 2025. Many affected firms planned to pass some costs to customers. A firm that absorbs costs can face lower margins; a firm that raises prices can face lower demand; some firms avoid both through sourcing changes or stronger pricing power.

Channel 3: Tariffs, Market Volatility, and Sequence-of-Returns Risk

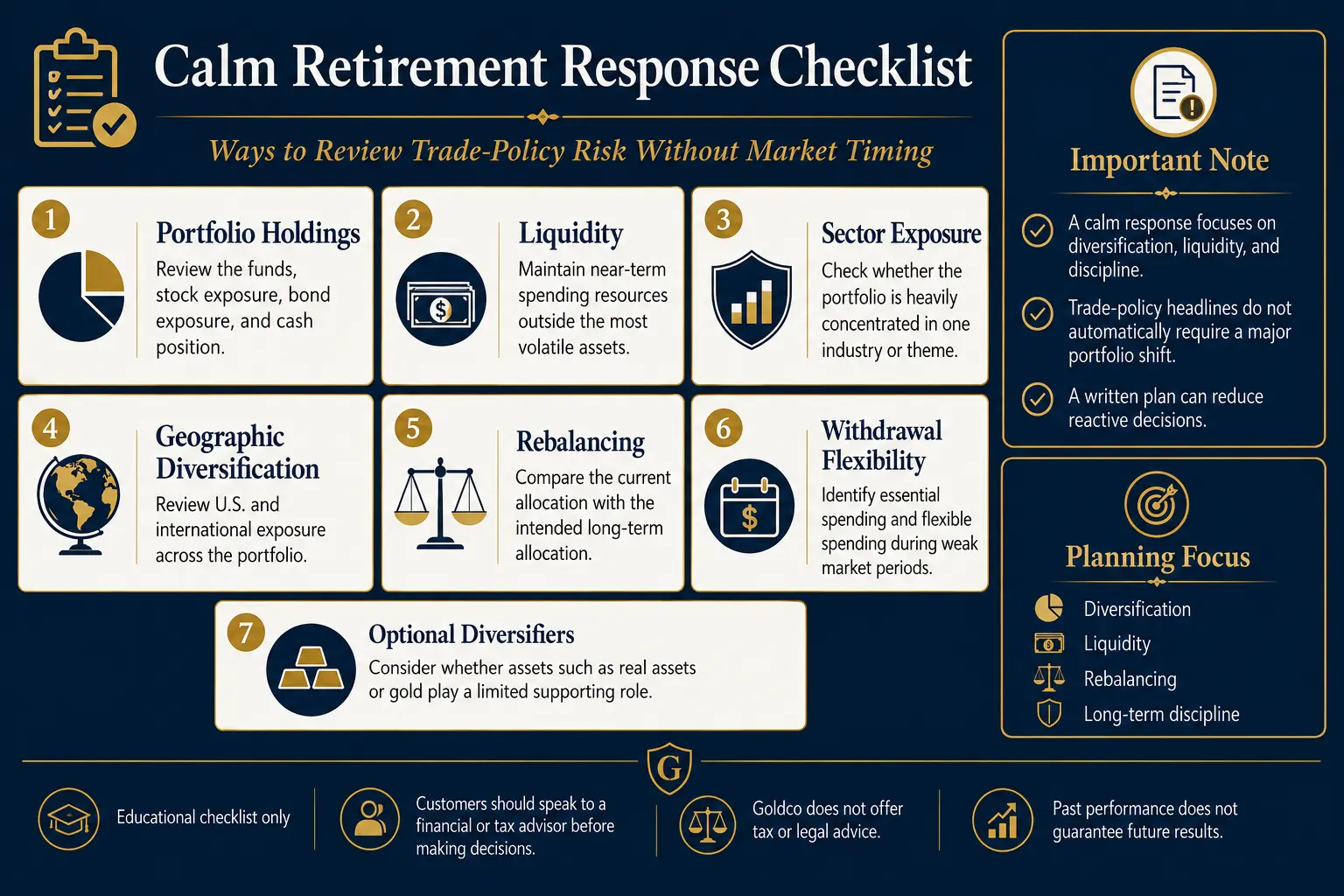

Tariff announcements can create uncertainty because investors must estimate rates, exemptions, duration, retaliation, court challenges, business responses, and economic effects — which can raise volatility even when the long-term outcome remains unclear. Volatility matters most for retirement accounts when money is being withdrawn. Sequence-of-returns risk refers to the danger that poor market returns occur early in retirement while withdrawals are reducing the balance. Fidelity explains that negative returns during the first retirement years, combined with withdrawals, can drain a portfolio more severely than similar losses later, and warns that reacting emotionally to short-term news can make long-term discipline more difficult. The point is not that a tariff announcement will create an early-retirement loss — it is that a withdrawal plan should already be able to handle market weakness from many possible causes.

General planning tools include maintaining a reserve for near-term spending, holding a mix of stocks/bonds/cash, avoiding unnecessary sales from a falling category, rebalancing rather than making an all-or-nothing shift, adjusting flexible withdrawals during poor periods, and matching lower-volatility assets to near-term income. No single method fits every retiree — pension income, Social Security, health costs, RMDs, tax status, and portfolio size all matter. Customers should speak to a financial or tax advisor before changing a withdrawal plan, retirement allocation, or income strategy. Goldco does not offer tax or legal advice.

Sector and Geographic Exposure

Trade-policy effects depend partly on what industries and countries sit inside the funds. Import-heavy businesses that rely on imported components may face higher production costs (Fed research notes tariffs can raise the prices of both consumer and investment goods, with the modeled effect on investment goods potentially larger because imported capital equipment is an important input). Domestic competitors may gain pricing room or market share, though that benefit can be limited if they also use imported inputs or demand slows. Exporters and multinationals can be affected by retaliatory measures, currency movements, and foreign demand. Bonds face competing forces — higher prices can raise inflation and rate pressure, while weaker growth can support lower rates, and credit risk can change — so a simple "tariffs are bad for bonds" rule is unreliable. International funds spread exposure across countries but do not remove trade risk; geographic diversification remains useful because countries, currencies, and industries do not respond identically.

Diversification Responses, Not Market Timing

Diversification planning does not require predicting which tariff policy will remain in place. Investor.gov explains that diversification spreads investments so one loss may be partly offset by other holdings, while noting it cannot ensure a portfolio avoids losses during a broad market decline. A retirement portfolio can be reviewed across U.S. and international stocks; large, medium, and smaller companies; growth and value styles; import-heavy and domestically focused businesses; government and corporate bonds; short-, intermediate-, and long-term maturities; cash; and optional real assets. The objective is not to own every possible asset — it is to avoid letting one company, sector, country, or policy outcome control the whole retirement result.

A 401(k) can appear diversified while carrying hidden concentration: a large employer-stock position, several funds owning the same major companies, a target-date fund plus duplicate stock funds, heavy single-sector exposure, a large U.S.-only allocation, or a bond allocation in one maturity range. Plan documents and fund fact sheets show holdings, asset classes, benchmark, expenses, and geographic exposure. Investor.gov describes rebalancing as restoring a portfolio to its intended allocation after drift — many professionals review on a regular schedule (often every six or twelve months) rather than responding to every news event. A tariff-related market move can be a reason to check the allocation; it does not automatically create a reason to abandon the long-term plan.

Where Tangible Assets Like Gold May Fit

Discussions often present gold as a direct defense against trade policy. Public research does not establish gold as a dependable tariff hedge. Gold prices can respond to economic-policy uncertainty, inflation expectations, real interest rates, U.S. dollar movements, central-bank demand, investor risk sentiment, jewelry and investment demand, and market liquidity — and these forces can move in opposite directions. A study in Resources Policy examined economic-policy uncertainty and gold prices in eight countries; its nonlinear analysis found evidence that uncertainty affected gold prices in some parts of the return distribution, while a standard linear causality test found no causal association. A separate academic analysis found gold's response to uncertainty depended on the level of uncertainty and the state of the gold market, concluding its hedge or safe-haven role could not be assumed to hold at all times.

This mixed evidence does not support a claim that gold rises whenever tariffs increase or markets become uncertain — gold can also fall when real interest rates rise, the dollar strengthens, investors need liquidity, or other forces dominate. A limited allocation may serve as one diversifier in some portfolios; it should not replace stocks, bonds, cash reserves, or a retirement-income plan. The gold allocation backtest can help compare historical scenarios, and how much gold to own in retirement discusses allocation without presenting one percentage as suitable for everyone. Customers should speak to a financial or tax advisor before changing an allocation or using a Gold IRA. Goldco does not offer tax or legal advice.

A Calm, Non-Reactive Plan

A practical plan can follow eight steps:

- Identify the real holdings. List every 401(k), IRA, brokerage, pension, and cash account, recording the stock, bond, cash, sector, employer-stock, and international percentages.

- Separate near-term spending from long-term growth, so money needed soon does not depend entirely on selling volatile assets after an announcement.

- Test inflation pressure. Estimate how higher prices for food, transportation, home repairs, and healthcare supplies could affect the budget (see the purchasing-power guide).

- Review company and sector concentration — whether the portfolio depends heavily on one employer, industry, country, or group of large companies.

- Compare the current allocation with the intended allocation, rebalancing to restore the planned risk level without forecasting the next announcement.

- Review withdrawal flexibility — which spending is essential and which can be adjusted temporarily during a weak market.

- Evaluate optional diversifiers carefully. Gold, commodities, or real estate should be reviewed for liquidity, fees, volatility, tax treatment, and their role in the complete portfolio. The Gold IRA calculator and quiz can help organize assumptions and questions.

- Set a review schedule that defines when rebalancing or allocation changes will be considered, reducing the pressure to react to each headline.

Frequently Asked Questions

Do tariffs directly change a 401(k)?

No. Tariffs do not directly change the federal tax structure of a 401(k). They can affect the value and performance of the stocks, bonds, and funds held inside the account.

Do tariffs always raise consumer prices?

No. Tariffs can raise import costs and contribute to higher prices, but the outcome depends on supplier pricing, business margins, customer demand, substitution, exemptions, and pass-through. BLS states that tariffs are not directly included in CPI but can affect measured prices indirectly.

Which stocks benefit from tariffs?

No universal group can be identified in advance. Some domestic competitors may benefit from reduced import competition, while companies with imported inputs, export exposure, or weaker pricing power may face pressure.

Should a retirement account move to cash during tariff volatility?

A broad move to cash is a market-timing decision and can create missed-recovery and purchasing-power risks. Allocation decisions should reflect time horizon, withdrawal needs, and risk tolerance rather than one policy headline.

What is sequence-of-returns risk?

It is the risk that poor returns occur early in retirement while withdrawals are being taken, causing greater long-term damage than similar losses later.

Is gold a tariff hedge?

No reliable evidence establishes gold as a consistent tariff hedge. Research finds that gold can respond to economic-policy uncertainty in some market conditions but not in a stable or predictable way across all periods.

Update Log

- 2026: Initial publication. Sourced to Federal Reserve Board and regional Fed research on 2025 tariffs (consumer prices, household spending, market reactions, CFO survey), BLS CPI methods, Investor.gov, FINRA, Fidelity, and independent studies on gold and policy uncertainty. Tariff policy and estimates change — figures apply to specific study periods and are not forecasts.

Sources

- U.S. Bureau of Labor Statistics. Concepts.

- Internal Revenue Service. Retirement topics participant directed accounts.

- Federal Reserve Board. Detecting tariff effects on consumer prices in real time part II 20260.

- Federal Reserve Board. Paying more and buying less 2025 tariffs and us household spending.

- Federal Reserve Bank of San Francisco. Effects of tariffs on inflation and production costs.

- Federal Reserve Bank of San Francisco. Market reactions to tariff announcements.

- Federal Reserve Bank of Richmond. The cfosurvey 20250625.

- Federal Reserve Bank of Richmond. 20250625 data and results.

- Investor.gov (SEC). Diversify your investments.

- Investor.gov (SEC). Beginner's Guide to Asset Allocation.

- FINRA. Asset Allocation and Diversification.

Article reviewed and edited by Daniel M. — editor, 401kToGoldIRA.org. Sourced to Federal Reserve research, BLS, Investor.gov, FINRA, and independent studies; educational only, not tax or legal advice, and not a market forecast.

Further Reading

How to Protect Retirement Purchasing PowerThe broader inflation toolkit: COLA, TIPS, I Bonds, diversification.

How to Protect Retirement Purchasing PowerThe broader inflation toolkit: COLA, TIPS, I Bonds, diversification. Gold Allocation BacktestHow 0-25% gold historically affected a 60/40 portfolio — sourced.

Gold Allocation BacktestHow 0-25% gold historically affected a 60/40 portfolio — sourced. How Much Gold Should Investors Own in Retirement?A framework for matching allocation to goals, liquidity, and risk.

How Much Gold Should Investors Own in Retirement?A framework for matching allocation to goals, liquidity, and risk.