Educational only: This article summarizes IRS rules and Florida statutes in general terms. It is not financial, tax, or legal advice, and tax and legal treatment depend on individual facts. Customers should speak to a financial or tax advisor before making decisions, and consult a Florida attorney or tax professional for Florida-specific circumstances. Goldco does not offer tax or legal advice. Past performance does not guarantee future results.

Quick Answer: Federal Rules First, Florida Considerations Second

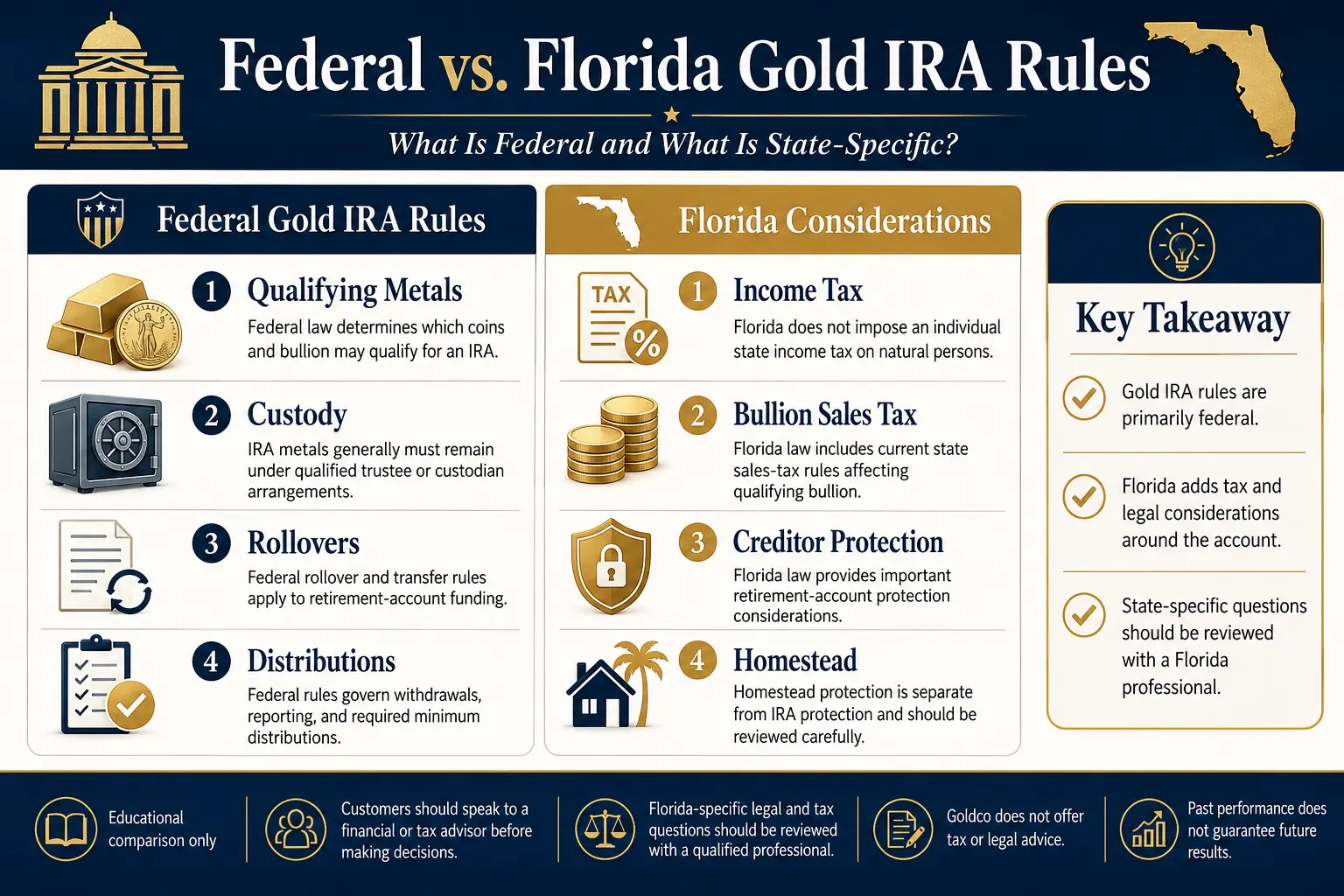

A Florida gold IRA is normally a traditional or Roth self-directed IRA whose custodian permits qualifying precious metals. The account follows the same federal IRA rules that apply in other states. Florida can still affect the larger retirement picture:

- Florida does not impose an individual income tax on natural persons, although federal tax can still apply to traditional IRA distributions and nonqualified Roth distributions.

- Since August 1, 2025, sales of qualifying gold, silver, and platinum bullion in Florida are exempt from sales and use tax regardless of the sales price. Separate rules still apply to coins, currency, jewelry, and products that do not meet the bullion definition.

- Florida law provides broad creditor protection for qualifying IRA assets, but the protection has exceptions and should not be treated as absolute.

- Florida's constitutional homestead protection concerns qualifying real property. It is separate from IRA protection and should not be assumed to protect bullion simply because metal is kept at a residence.

Customers should speak to a financial or tax advisor before making decisions involving taxes, creditor protection, rollovers, distributions, or compliance. A Florida attorney or tax professional should review state-specific circumstances. Goldco does not offer tax or legal advice.

Gold IRA Rules in Florida: The Federal IRS Framework

Florida does not issue its own Gold IRA rulebook. The account is an IRA under federal tax law, with Florida law affecting selected state issues around the account. A "self-directed IRA" describes an account in which the custodian allows a wider range of assets and the owner directs transactions — it is not a separate federal tax category. Traditional IRA contributions may be deductible in some circumstances, and traditional distributions are generally taxable except for properly tracked after-tax basis; Roth contributions are not deductible, but qualified Roth distributions may be tax-free. Holding gold does not turn a traditional IRA into a Roth IRA or create a new state tax classification.

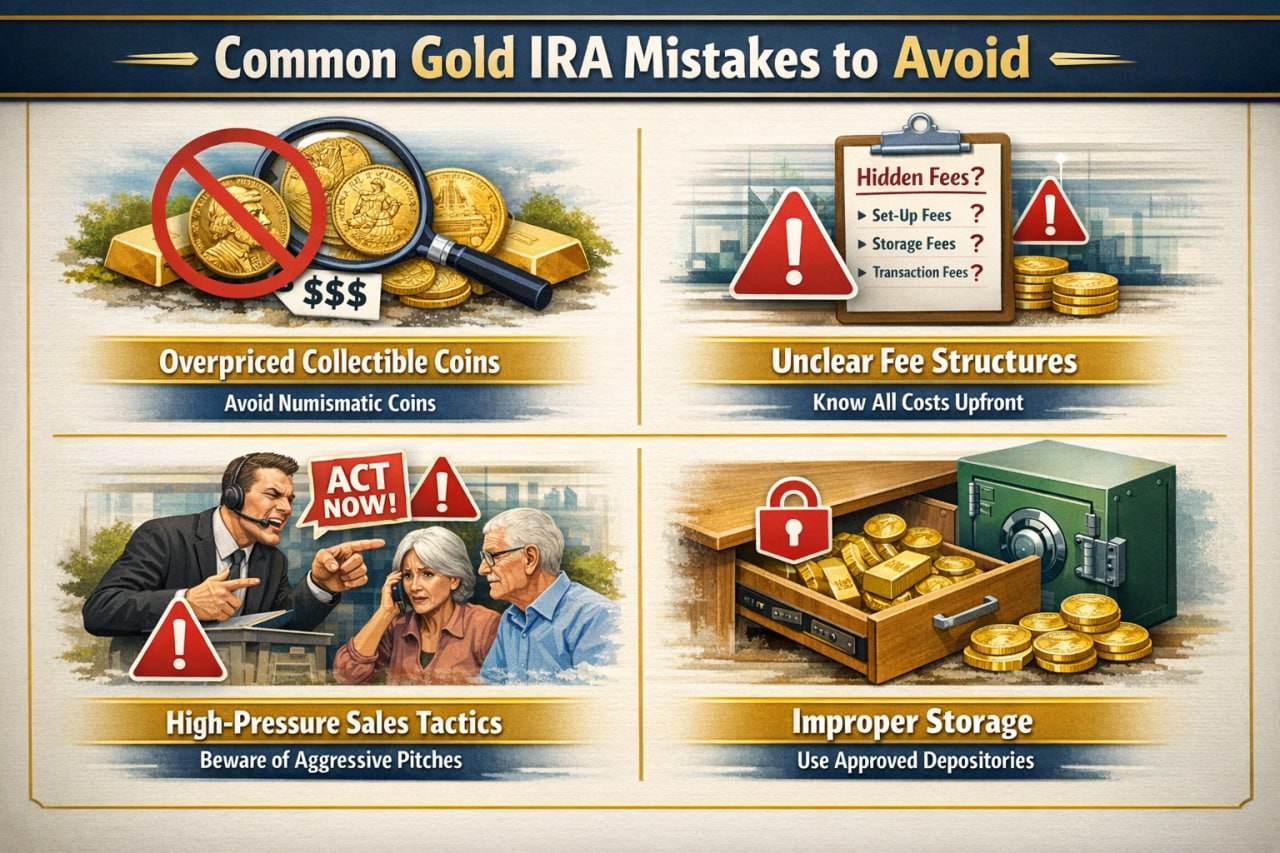

Federal law generally treats metals and coins as collectibles, with an exception for specified coins and qualifying gold, silver, platinum, or palladium bullion that meets the legal requirements and remains in proper trustee possession. A dealer's statement that a product is "IRA eligible" should be confirmed by the custodian before purchase. The IRS states that qualifying bullion must remain in the physical possession of a bank or an IRS-approved nonbank trustee, and the same rule applies when an IRA-owned LLC acquires the metal indirectly — so personal home possession while the metal is still claimed as an IRA asset creates serious tax and compliance risk, and Florida residence does not change that. An eligible retirement distribution can move into a self-directed IRA through a direct rollover or a rollover completed under federal rules; when money is paid to the owner, the normal deadline is 60 days, and direct trustee-to-trustee movements avoid personal receipt. The rollover guide covers the step-by-step process. Customers should speak to a financial or tax advisor before making decisions involving contributions, rollovers, or account funding. Goldco does not offer tax or legal advice.

Florida's No-State-Income-Tax Advantage for Retirees

Florida's tax structure is one reason many retirees consider the state. Florida law states that the state income-tax code is not intended to tax natural persons, and the Florida Constitution limits state income taxation of natural persons. In general terms, Florida does not impose a state individual income tax on IRA distributions received by natural persons, which can reduce the state-level tax burden compared with states that tax retirement income. Federal tax treatment still applies: traditional IRA distributions are generally included in federal taxable income except for any tracked basis; qualified Roth distributions may be federal income-tax-free; and required minimum distributions generally apply to traditional IRAs (current IRS guidance generally starts them at age 73, while original Roth owners take no lifetime RMDs).

Florida's lack of individual income tax does not make a traditional Gold IRA distribution federally tax-free, and it does not remove withholding, reporting, RMD, or early-distribution rules. Residency, domicile, part-year moves, trusts, business entities, and income sourced to another state can create separate questions — a taxpayer moving to Florida should not assume every state tax issue ends on the date of arrival. Customers should speak to a financial or tax advisor before making decisions involving retirement income, residency, withdrawals, or Roth conversions. Goldco does not offer tax or legal advice.

Florida Precious Metals Sales Tax: The Current Rules

Florida precious-metals sales-tax law changed recently, making older articles easy to misread.

Bullion no longer has a $500 purchase threshold

Florida Department of Revenue guidance states that, effective August 1, 2025, sales of gold, silver, and platinum bullion are exempt from Florida sales and use tax regardless of the sales price. The current Florida statute states that a single-transaction sale of gold, silver, or platinum bullion, or a combination of those metals, is exempt. The former minimum purchase threshold should therefore not be presented as the current rule for qualifying bullion.

Coins and currency still have separate rules

Florida law treats coins and currency separately from bullion. Current statutory language includes exemptions for certain legal-tender exchanges and provides that when the taxable amount represented by a coin or currency transaction exceeds $500, the transaction is exempt. Classification can be technical: a product marketed as a "gold coin" may be treated differently from a bar, ingot, plate, legal-tender coin, collectible, jewelry item, or fabricated product. The bullion exemption should not be assumed to cover every precious-metal item. Florida also enacted Section 215.986, recognizing narrowly defined gold and silver forms as state legal tender for debts incurred on or after July 1, 2026 — acceptance is voluntary, federal legal-tender law continues to control, and that state law does not change federal Gold IRA eligibility or custody rules.

A Florida sales-tax exemption concerns the purchase, use, or storage treatment of covered property under state sales-tax law. It does not make a traditional IRA distribution tax-free, remove federal IRA custody requirements, or create a deduction for buying metal. The practical result can depend on the product, delivery location, seller, transaction documents, and whether the purchase occurs inside or outside an IRA. Customers should speak to a financial or tax advisor before making decisions involving Florida sales tax, federal IRA tax, or distributions. Goldco does not offer tax or legal advice.

Florida IRA Creditor Protection

Florida IRA creditor protection is broader than many simple summaries suggest, but it is not a one-line rule. Florida Statutes Section 222.21 generally exempts qualifying funds and accounts from creditor claims when the arrangement meets the listed federal tax provisions, expressly referencing accounts under Internal Revenue Code Sections 408 and 408A (traditional and Roth IRAs). The statute also states that protected assets do not automatically lose protection after the owner's death merely because of a qualifying direct transfer or eligible rollover to an inherited IRA. However, listed exceptions include claims by an alternate payee under a qualified domestic relations order and certain surviving-spouse elective-share claims.

Several limits matter: the account must remain a qualifying retirement arrangement; the type of creditor and legal proceeding can affect the analysis; and divorce, support, tax, federal, bankruptcy, probate, and inherited-account issues can involve separate rules. Florida law also states that an exemption is not effective when it results from a fraudulent transfer or conveyance, so a Gold IRA should not be funded or moved for the purpose of frustrating an existing creditor. For broader comparisons, see Gold IRA creditor protection by state. Customers should speak to a Florida attorney before relying on IRA creditor protection, and to a financial or tax advisor before changing or withdrawing retirement assets. Goldco does not offer tax or legal advice.

Florida Homestead Protection Is Separate From Gold IRA Protection

Florida's constitutional homestead protection is often discussed alongside retirement-account protection, but the two are different. Article X, Section 4 of the Florida Constitution protects qualifying homestead property from forced sale and judgment liens, subject to stated exceptions (taxes and assessments, purchase obligations, improvement or repair obligations, and certain labor performed on the property), and applies acreage limits based on whether the homestead is inside or outside a municipality. The homestead rule primarily concerns qualifying real property. Physical bullion stored in a Florida house should not be assumed to become protected homestead real estate merely because it is located there, and Gold IRA assets do not become homestead property — their possible protection comes from retirement-account law, not from the house in which the owner lives. Florida also provides separate personal-property exemptions whose available amount can depend on whether the debtor claims homestead benefits. Customers should speak to a Florida attorney before relying on homestead, personal-property, or retirement-account exemptions. Goldco does not offer tax or legal advice.

Storage Rules and Florida Depository Options

Federal custody rules control where IRA metals can be held. The account holder should not select a home safe, personal safe-deposit box, or private vault and assume the arrangement preserves IRA status. The custodian must approve the transaction and storage arrangement, and the metals normally move from the dealer to a facility used under the custodian's custody process. The account agreement should identify the IRA trustee or custodian; the depository and physical location; whether storage is segregated or commingled; inventory and statement procedures; insurance and audit information; annual storage charges; and sale, shipment, and in-kind distribution procedures. For the difference between storage methods, see segregated versus commingled storage.

Florida has private precious-metals vault options. For example, Strategic Wealth Preservation states that it offers a Doral, Florida storage location operated by Loomis International USA — that public statement verifies the advertised location and operator only, and does not establish that every IRA custodian accepts the facility or that the IRS has separately endorsed the vault for every IRA arrangement. The correct review begins with the IRA custodian: a Florida location can be convenient, but location alone does not establish federal compliance. Customers should speak to a financial or tax advisor before making decisions involving custody, home possession, storage, or in-kind distributions. Goldco does not offer tax or legal advice.

Questions for a Florida Tax Professional or Attorney

Before opening or changing a Florida gold IRA, a professional review can address questions such as:

- Does Florida domicile apply for the relevant tax year and legal issue?

- How would traditional or Roth distributions be treated under the customer's federal circumstances?

- Could another state claim tax based on prior residency, source income, or a part-year move?

- Does the exact coin, bar, or other product qualify for Florida's current sales-tax treatment?

- Is the product bullion, legal-tender coin, collectible currency, jewelry, or another category?

- Does the proposed IRA custodian meet federal requirements, and which depository will hold the metals?

- How do Florida creditor-protection rules apply to the account, beneficiary, and claim type?

- Could a transfer be challenged under fraudulent-transfer law?

- How do Florida homestead and retirement-account protections interact with the broader estate plan?

- What federal tax would apply to a cash or in-kind distribution, and which records should be retained?

A separate due-diligence list is available in the 21 questions to ask before opening a Gold IRA, and the educational quiz can help organize research before a company conversation.

Frequently Asked Questions

Are Gold IRA rules different in Florida?

The main IRA, rollover, metal-eligibility, custody, distribution, and federal tax rules are federal. Florida adds state considerations involving individual income tax, sales tax, creditor protection, homestead law, and domicile.

Does Florida tax Gold IRA withdrawals?

Florida does not impose an individual income tax on natural persons. Federal income tax can still apply to traditional IRA withdrawals and to Roth withdrawals that are not qualified. A tax professional should confirm residency and transaction-specific treatment.

Is there still a $500 Florida sales-tax threshold for bullion?

No. Effective August 1, 2025, sales of qualifying gold, silver, and platinum bullion are exempt regardless of sales price. A separate $500 provision remains relevant to certain taxable coin and currency transactions.

Can Gold IRA metals be stored at a Florida home?

Federal rules generally require qualifying IRA bullion to remain in the physical possession of a bank or IRS-approved nonbank trustee. Florida residence does not create an exception for personal home possession.

Are Florida Gold IRAs protected from creditors?

Florida law generally protects qualifying traditional and Roth IRA assets from creditor claims under Florida Statutes Section 222.21, but exceptions and other legal regimes can apply. The account, claim, timing, and proceeding should be reviewed by a Florida attorney.

Does Florida homestead protection cover gold stored in a house?

Florida homestead protection primarily concerns qualifying real property and certain constitutionally stated personal property. Physical metal should not be assumed to receive homestead treatment merely because it is stored at the residence.

Update Log

- 2026: Initial publication. Sourced to IRS (Pub 590-A/590-B, custody and collectibles rules), Florida Statutes (Ch. 212 sales tax, 220 income tax, 222 creditor/personal-property exemptions, 215.986 legal tender), the Florida Department of Revenue TIP 25A01-03 (August 1, 2025 bullion exemption), and the Florida Constitution. State rules change — confirm current figures with a Florida professional before acting.

Sources

- Internal Revenue Service. Individual Retirement Arrangements (IRAs).

- Internal Revenue Service. Publication 590-A (Contributions to IRAs).

- Internal Revenue Service. Publication 590-B (Distributions from IRAs).

- Internal Revenue Service. Retirement Plans FAQs Regarding IRAs.

- Internal Revenue Service. Investments in Collectibles in IRA Accounts.

- Internal Revenue Service. Approved Nonbank Trustees and Custodians.

- Internal Revenue Service. Rollovers of Retirement Plan and IRA Distributions.

- Internal Revenue Service. Required Minimum Distributions FAQs.

- Florida Legislature — Florida Statutes. Florida Statutes ch. 299.

- Florida Legislature — Florida Statutes. Index.

- Florida Department of Revenue. Sales & Use Tax on Coins & Bullion (TIP 25A01-03).

- Florida Legislature — Florida Statutes. Florida Statutes ch. 299.

- Florida Legislature — Florida Statutes. Florida Statutes ch. 299.

- Florida Administrative Code. ChapterHome.

- Florida Legislature — Florida Statutes. Florida Statutes ch. 299.

- Florida Legislature — Florida Statutes. Florida Statutes ch. 299.

- Florida Legislature — Florida Statutes. Florida Statutes ch. 299.

- Florida Legislature — Florida Statutes. Florida Statutes ch. 299.

Article reviewed and edited by Daniel M. — editor, 401kToGoldIRA.org. Sourced to IRS.gov, Florida Statutes, and the Florida Department of Revenue; educational only, not tax or legal advice.