Educational only: This guide summarizes IMF, SSA, Morningstar, and Investor.gov material in general terms and is not financial, tax, or legal advice. Stress-test outputs are illustrative scenario results, not forecasts. Customers should speak to a financial or tax advisor before making decisions. Goldco does not offer tax or legal advice. Past performance does not guarantee future results.

Quick Answer: What Stress-Testing a Retirement Portfolio Means

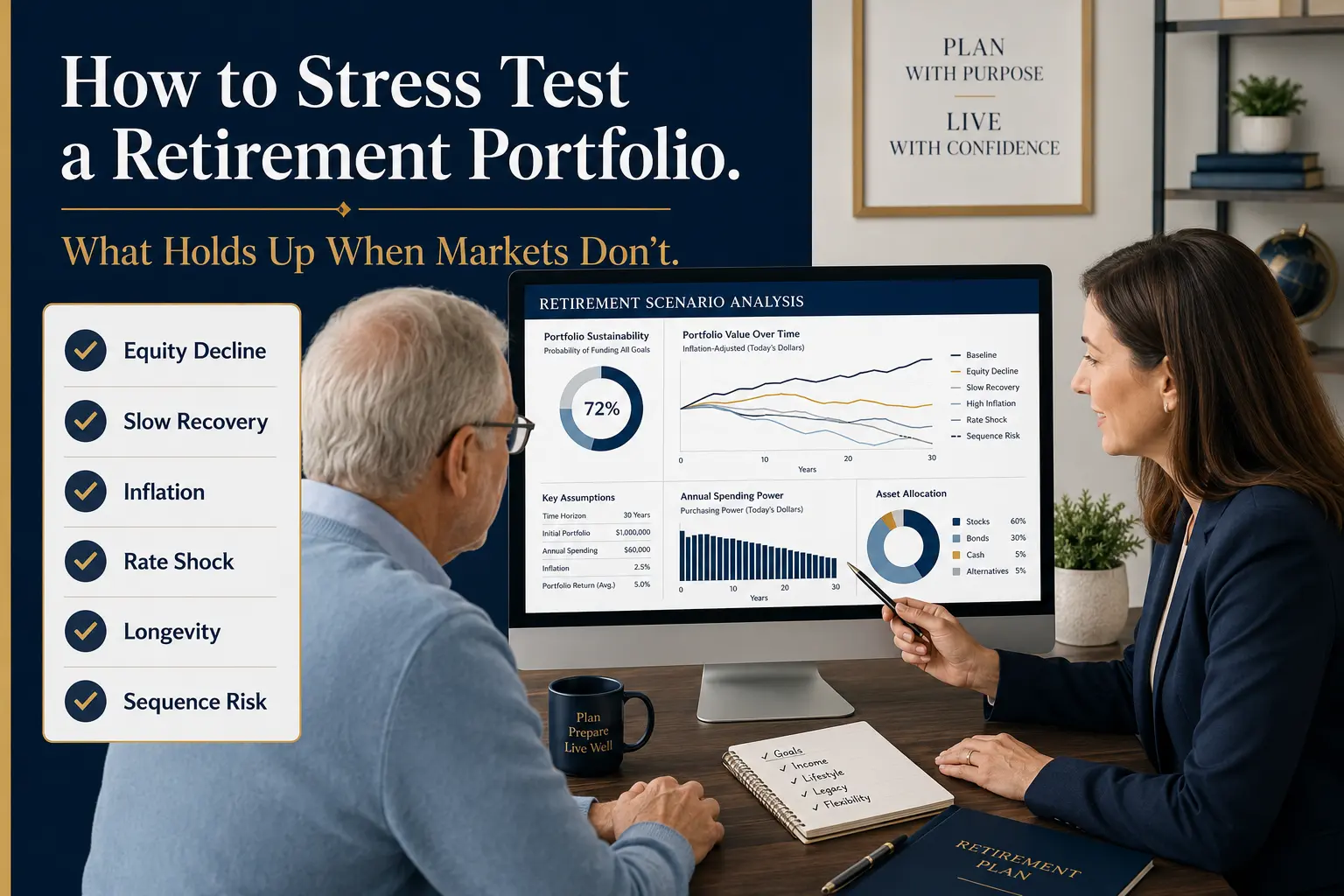

Stress testing is a scenario method used to measure how a financial position may respond under difficult conditions rather than only under a central forecast (International Monetary Fund). For a retirement plan, the core scenarios are a large equity decline, a slow recovery, high inflation, a rate and bond shock, a longevity overshoot, and sequence-of-returns risk early in retirement. Each is applied separately to the portfolio, the withdrawal plan, the cash reserve, and the time horizon, and the plan is judged on drawdown, survival, and the first year a shortfall appears. A stress test does not forecast the next downturn — it finds the weak points while there is still time to change the allocation, the withdrawal rate, the cash buffer, or the spending plan.

Why a Stress Test Beats an Average-Return Estimate

An average return hides the risks that actually end retirements. Two portfolios with the same long-run average can end very differently depending on when losses arrive, how long a recovery takes, and whether inflation erodes spending power along the way. A stress test replaces the single-number assumption with a set of adverse-but-plausible paths, so a plan that looks comfortable on an average basis can be checked against the conditions that break it. The method is the same one financial supervisors use on banking systems: apply a difficult scenario, then measure whether the position still stands (International Monetary Fund). For a household, the value is the same — a weak point found in a spreadsheet is far cheaper to fix than one found in the tenth year of retirement.

Define the Scenarios

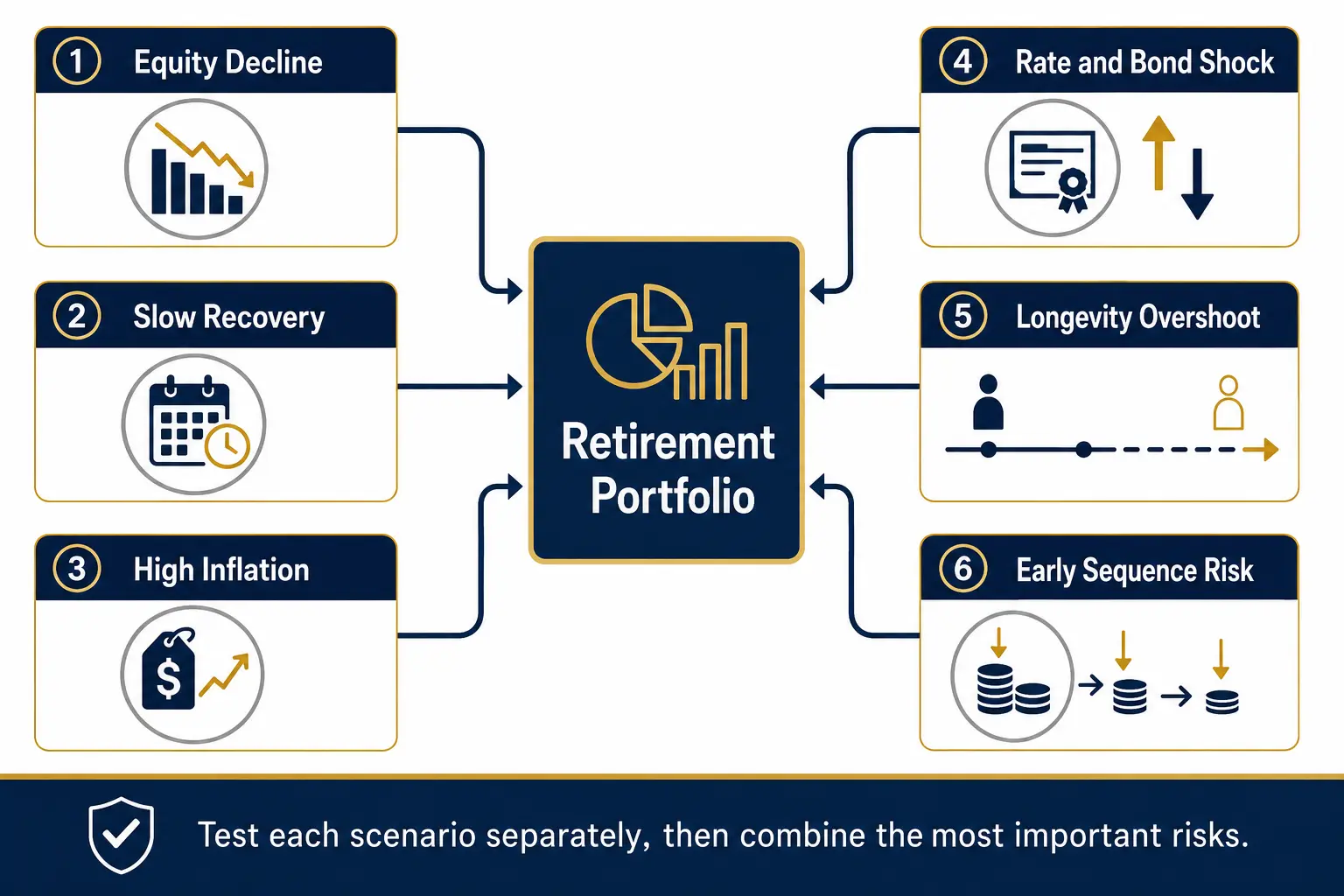

A useful stress test starts with a short list of adverse conditions, each tested on its own before the most relevant ones are combined:

- Equity decline. A large drop in stock values early in the plan, testing how much of the portfolio is exposed to a single asset class.

- Slow recovery. A market that stays down for several years rather than rebounding quickly, extending the period of withdrawals at depressed values.

- High inflation. A sustained rise in prices that raises the spending target faster than the portfolio grows. Treasury Inflation-Protected Securities are one tool sometimes tested against this risk, because their principal adjusts with inflation (TreasuryDirect).

- Rate and bond shock. Rising interest rates that reduce the market value of existing bonds, testing the assumption that bonds are always a stabilizer.

- Longevity overshoot. A retirement that lasts longer than the base case. Average remaining life expectancy at age 65 is about 18.1 years for men and 20.7 years for women under 2023 mortality rates, but a plan may need to fund well beyond the average (Social Security Administration).

- Early sequence risk. Poor returns concentrated in the first years of retirement, when withdrawals do the most damage.

Run the Test: Applying Scenarios to Allocation, Withdrawals, and Cash

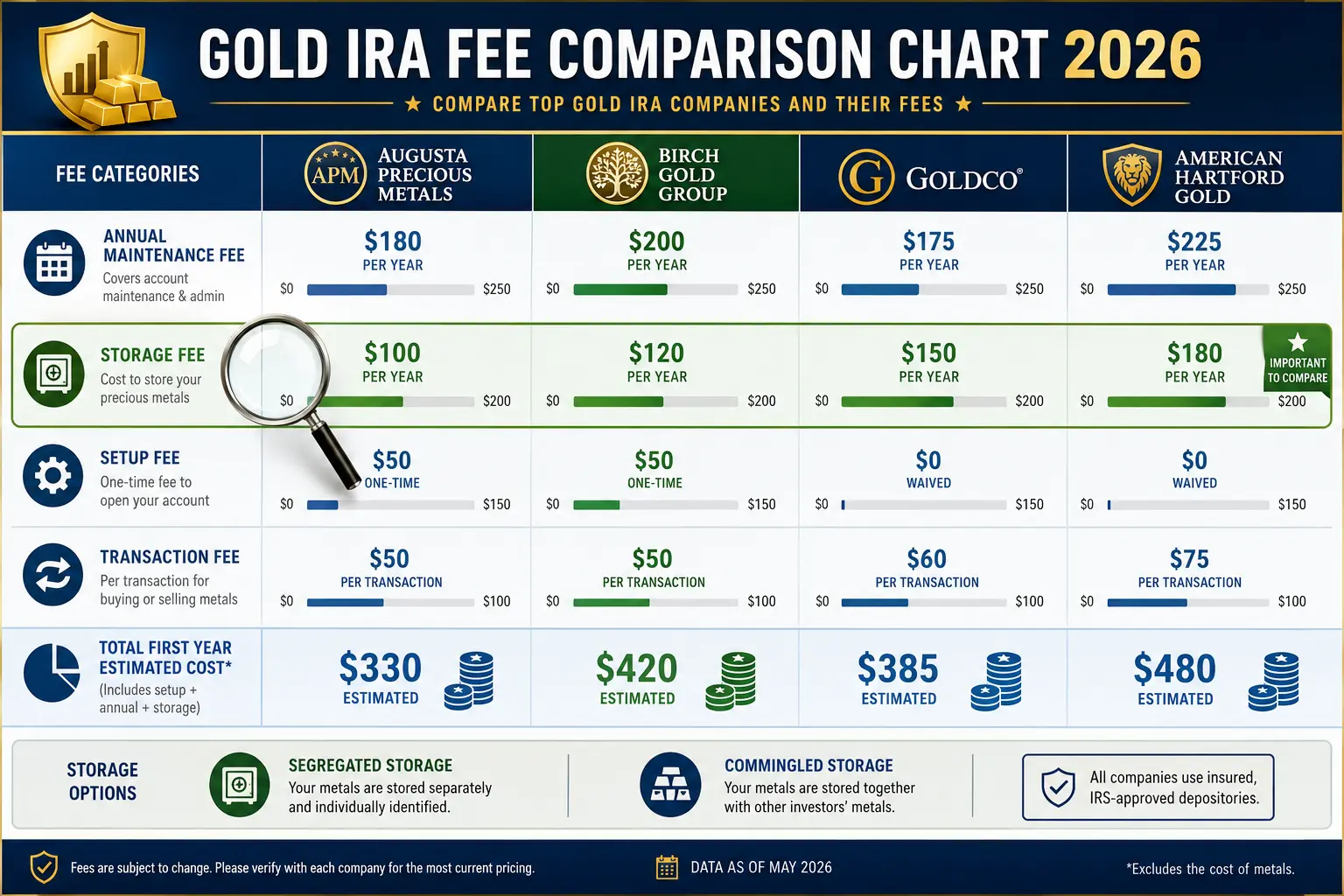

Running the test means applying each scenario to three moving parts at once: the asset allocation, the withdrawal plan, and the cash reserve. Investor.gov notes that diversification spreads exposure across investments and asset classes and can reduce damage in a decline, though it cannot prevent losses when markets fall broadly (Investor.gov). A stress test checks whether the current mix actually diversifies under stress, or whether several holdings fall together. On the spending side, the withdrawal rate is the lever most within a household's control. Morningstar's 2024 research estimated a 3.7% starting rate for a 30-year horizon under fixed inflation-adjusted withdrawals and a 90% modeled success rate, with a lower rate for longer horizons — a stress test can start from a figure like that and then reduce it to see how much cushion the plan has (Morningstar). The cash reserve is the third input: a bucket of near-term spending held in cash or short high-quality bonds can keep a scenario from forcing sales at depressed prices, and a 2026 Associated Press summary of Morningstar guidance described a cushion of roughly one to two years of expected portfolio withdrawals as a common starting point (Associated Press).

Read the Results: Drawdown, Survival, and the Shortfall Year

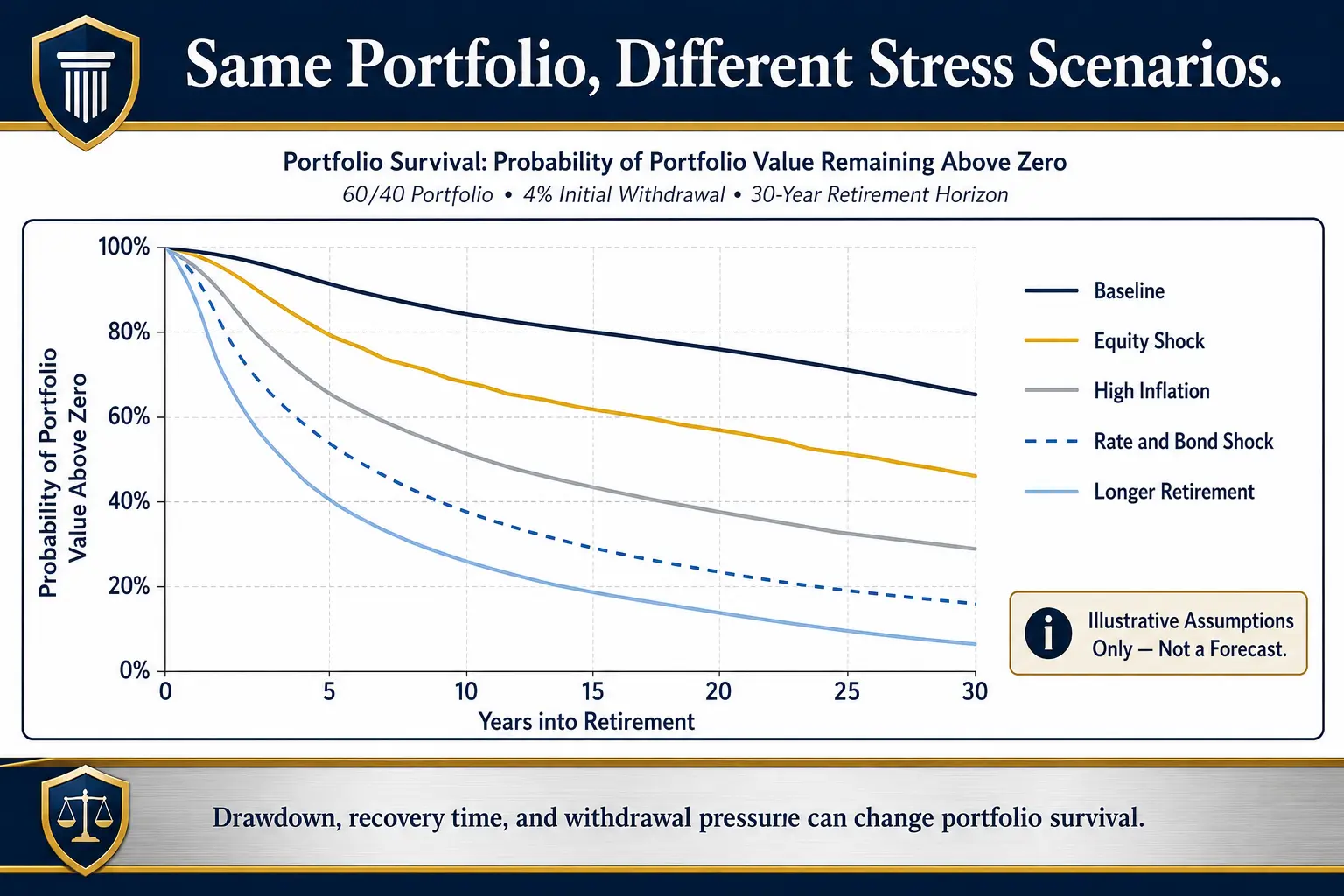

A stress test produces three readings worth focusing on. Drawdown is the deepest peak-to-trough fall in each scenario — it shows how much value the plan must be able to tolerate without a forced change. Portfolio survival is the probability the balance stays above zero across the full horizon; the same portfolio can show a high survival rate in the baseline and a much lower one under an equity shock or a longer retirement. The shortfall year is the first year a scenario runs the balance to zero or below the level needed to fund essential spending — an early shortfall year is the clearest signal that a plan needs adjustment. Reading these together matters more than any single number: a plan with an acceptable baseline but a severe drop under early sequence risk has a specific, fixable weakness, not a general one.

Fix What Fails

When a scenario fails, the repair usually comes from one of a handful of levers, chosen to match the specific weakness. A plan that breaks under an equity shock or early sequence risk often needs a more diversified allocation or a larger near-term cash reserve so stocks are not sold at the bottom. A plan that fails under a longevity overshoot may need a lower starting withdrawal rate, a later retirement date, or more lifetime income. A plan that fails under high inflation may need inflation-linked holdings or more spending flexibility. And a plan that fails under a rate and bond shock may need attention to bond duration and credit quality rather than treating all bonds as identical stabilizers. Diversification and low-correlation assets sit inside this step as one lever among several. Precious metals can be tested here: the World Gold Council, an industry body, argues that gold can add diversification and liquidity, though its research does not establish one allocation that fits every retiree, and metals carry price, cost, and liquidity considerations of their own (World Gold Council). The relevant test is whether a modest position improves survival across the scenarios that failed — not whether metals are the answer. The gold allocation backtest and gold vs. S&P 500 calculator can support that comparison. Customers should speak to a financial or tax advisor before making decisions about allocation, withdrawals, or IRA assets. Goldco does not offer tax or legal advice.

A Worked Illustrative Example

The following is illustrative only, not a forecast. Consider a $1,000,000 portfolio, a 4% initial withdrawal ($40,000), a 2.5% annual spending increase, and a 30-year horizon. In a baseline scenario of steady mid-single-digit returns, the plan shows a high probability of lasting the full horizon. Under an equity shock — a sharp early decline — survival falls because withdrawals continue while the balance is depressed. Under high inflation, the spending target rises faster than the portfolio, and the balance is drained sooner. Under a rate and bond shock, the stabilizing sleeve loses value at the same time stocks are weak. Under a longer retirement of 35 to 40 years, even a healthy baseline can run short. Each scenario uses the same starting portfolio and withdrawal plan; only the stress differs, and the gap between the baseline and the stressed paths is the plan's true vulnerability. The lesson mirrors sequence-of-returns math: the order and timing of difficult conditions, not the average return, decide whether the money lasts. A temporary spending reduction, a larger cash buffer, or a lower starting withdrawal rate can each move a failing scenario back toward survival.

A Repeatable Annual Stress-Test Checklist

- Restate the base case: current balance, allocation, withdrawal rate, and planning horizon.

- Apply each scenario separately — equity decline, slow recovery, high inflation, rate and bond shock, longevity overshoot, early sequence risk.

- Record drawdown, survival probability, and the shortfall year for each.

- Combine the two or three most relevant risks for the household into a compound scenario.

- Identify which lever fixes each failure — allocation, withdrawal rate, cash buffer, spending flexibility, lifetime income, or diversification.

- Re-test after applying a fix to confirm it actually improves survival.

- Review the cash reserve against near-term spending and refill rules.

- Repeat annually and after any major change in health, markets, inflation, or retirement date.

Frequently Asked Questions

What is a retirement portfolio stress test?

A retirement portfolio stress test applies difficult but plausible scenarios to a portfolio, withdrawal plan, cash reserve, and time horizon. The goal is to measure drawdown, survival, and the first shortfall year rather than predict one exact future.

Which scenarios should a stress test include?

Common scenarios include a large equity decline, a slow or extended recovery, high inflation, a rate and bond shock, a longevity overshoot, and sequence-of-returns risk early in retirement. Each is tested separately, then the most relevant risks can be combined.

How does sequence-of-returns risk affect a retirement portfolio?

A large decline early in retirement can do more damage than a similar decline later, because withdrawals remove shares while prices are low, leaving fewer assets to recover. Testing an early-loss sequence shows whether a plan can survive a poor start.

What is a safe withdrawal rate for stress testing?

Withdrawal-rate research provides frameworks, not guarantees. Morningstar's 2024 research estimated a 3.7% starting rate for a 30-year horizon under fixed inflation-adjusted spending and a 90% modeled success rate. A stress test can lower that assumption to see how the plan responds.

Do precious metals improve stress-test results?

Metals may add diversification as one low-correlation lever tested inside a stress test, but they carry price, cost, and liquidity considerations and no universal allocation is established. A stress test evaluates whether a modest position improves survival, not whether metals are the answer.

Conclusion

A stress test turns a retirement plan from a single hopeful number into a set of tested outcomes. By applying an equity decline, a slow recovery, high inflation, a rate and bond shock, a longevity overshoot, and early sequence risk — then reading drawdown, survival, and the shortfall year — a household can find the weak points while there is still time to fix them with allocation, withdrawal-rate, cash-buffer, and diversification levers. Precious metals belong in that process as one option to test, never as the whole answer. The plan should be re-tested at least annually and after major changes, because the value of a stress test is in the adjustments it prompts before difficult conditions actually arrive.

Sources

- International Monetary Fund. A Guide to IMF Stress Testing: Methods and Models.

- Social Security Administration. Actuarial Life Table (Period Life Table, 2023).

- Morningstar. What's a Safe Retirement Spending Rate for 2025?.

- Associated Press (Morningstar guidance). Cash cushion and sequence-of-returns risk.

- Investor.gov. Diversify Your Investments.

- TreasuryDirect. Treasury Inflation-Protected Securities (TIPS).

- World Gold Council. The Relevance of Gold as a Strategic Asset (2026).

Article reviewed and edited by Daniel M. — editor, 401kToGoldIRA.org. A neutral scenario-analysis method sourced to the IMF, SSA, Morningstar, Investor.gov, TreasuryDirect, and the World Gold Council; educational only, not financial, tax, or legal advice.