Educational only: This is a neutral verification framework, not a fact-asserting review or an endorsement. As of July 2026, STRATA's website returned a bot-verification screen to automated research, so no current fees, ratings, complaint totals, or depository partners are attributed to it here. A public rating or complaint count does not determine whether a company is appropriate for any individual. Customers should speak to a financial or tax advisor before making decisions. Goldco does not offer tax or legal advice. Past performance does not guarantee future results.

Quick Answer: What a Self-Directed IRA Custodian Does and Does Not Do

A self-directed IRA custodian administers the retirement account under the written custodial agreement. Common duties can include opening the account, receiving contributions and transfers, processing approved purchase or sale instructions, maintaining records, issuing statements, preparing certain tax reports, processing distributions, and holding or recording title to account assets. Investor.gov warns that self-directed IRA custodians generally do not evaluate the quality, legitimacy, financial merit, or suitability of an alternative investment or its promoter — custodian acceptance should not be treated as proof that a precious-metals purchase, private placement, real-estate deal, or promoter has been independently checked (Investor.gov: Self-Directed IRAs and the Risk of Fraud).

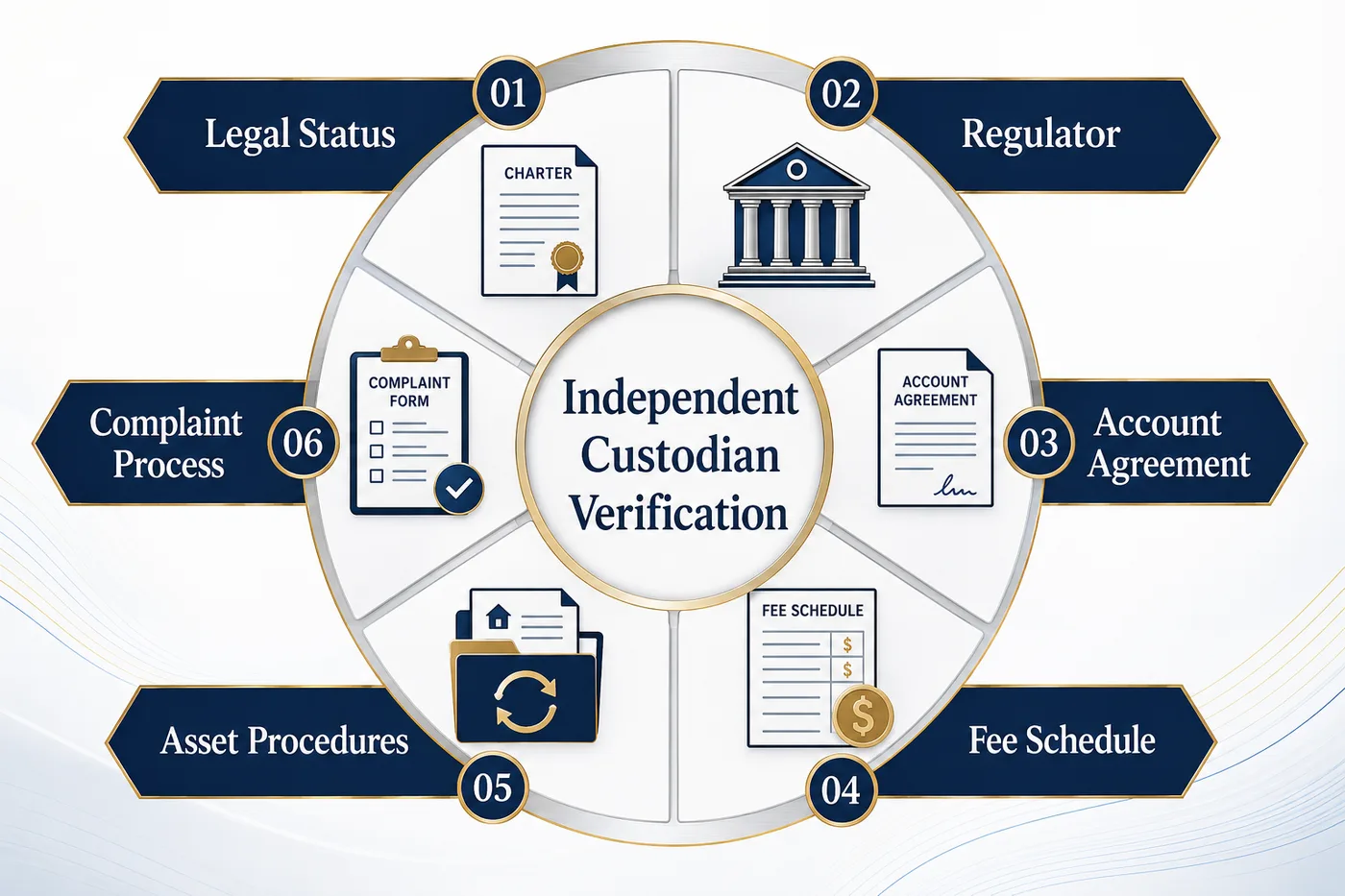

A precious-metals dealer performs a different role — it sells coins or bullion and sets the product price, premium, and buyback terms. A depository or approved trustee performs another role by holding physical metal under the storage and custody arrangement. The account documents should name each entity separately. Before an account is opened, the verification file should include the custodian's exact legal name, the chartering or approving authority, the current account agreement, the current custodian fee schedule, the asset-acceptance policy, transaction-processing instructions, distribution and transfer-out procedures, the complaint and escalation process, any precious-metals depository documents, and written confirmation of insurance and storage terms. Customers should speak to a financial or tax advisor before making decisions involving an IRA, rollover, transfer, distribution, prohibited transaction, product eligibility, or custody arrangement. Goldco does not offer tax or legal advice. The Questions to Ask Before Opening a Gold IRA guide provides a related dealer, custodian, and storage checklist.

Strata Trust Company Review: Start With the Exact Legal Entity

The first task is confirming the legal entity named on the account agreement. A brand name, website name, mailing name, and chartered legal name may not always appear in the same format. The account application, custodial agreement, fee schedule, tax forms, wire instructions, complaint policy, and regulator record should identify the same entity or explain the relationship among related entities. As of July 2026, STRATA's public website could not be read through the automated research system because it returned a verification screen, so no current company description, ownership statement, fee page, depository list, or account agreement was quoted as a verified STRATA record (STRATA Trust Company). That access result is not a positive or negative finding about the company — it means current records should be obtained directly and dated before publication or account opening.

The legal-identity file should record the full legal company name, state of charter or formation, main business address, customer-service address, telephone number, website and email domains, name shown on tax forms, name receiving account fees, regulator or chartering authority, and any parent, affiliate, or service-company relationship. A public rating or complaint count does not determine whether a company is appropriate for any individual.

How to Verify a Custodian Through IRS and State Records

Self-directed IRA custodian verification requires the correct public-record path.

Check the IRS Approved Nonbank Trustee Page

The IRS maintains an HTML page for entities approved under Treasury regulations to serve as nonbank trustees or custodians. As of July 2026, the IRS page linked to a list dated April 1, 2026 and stated that the list is updated as entities are added, removed, withdrawn, or finally revoked, and the page was last reviewed or updated on June 28, 2026 (IRS: Approved Nonbank Trustees and Custodians). The IRS page applies to nonbank trustees and custodians — it does not function as a complete list of every bank or state-chartered trust company that may serve as an IRA custodian, so a missing name on the nonbank list should not be treated by itself as proof that an entity lacks authority. The verification file should state whether the company claims to be a bank, a federally insured credit union, a savings and loan association, a state-chartered trust company, an IRS-approved nonbank trustee or custodian, or an administrator working with another custodian. The claimed category determines which regulator record should be checked.

Check the State Chartering Authority

The Texas Department of Banking states that it is responsible for chartering or licensing and supervising Texas trust companies, and its Bank and Trust Division examines and supervises Texas state-chartered institutions for financial condition, management practices, information-technology risks, and compliance with state and federal law (Texas Department of Banking; Banks & Trust Companies). The department provides an entity-search page that allows searches by entity name, entity type, city, county, and open or closed status; a current STRATA record should be searched under the exact legal name shown in the custodian agreement (Texas DoB: Entity Search). This research did not receive a completed entity-search result for STRATA through the automated interface, so no current Texas charter status, charter date, address, or open-status result is asserted here. A proper verification note should include the observation date, exact search name, regulator, entity type, status, and any charter or registration number displayed.

Why the Two Searches Are Different

The IRS nonbank page answers whether a nonbank entity has received federal approval under the cited Treasury regulation. A state regulator record answers whether a trust company holds a state charter and remains under that regulator's supervision. A company should not be described as "IRS approved" merely because it administers IRAs — the wording should match the actual public record.

Reading the BBB Profile and Complaint Records

A BBB profile can add context, but each section has a different meaning. As of July 2026, the BBB stated that its letter rating reflects the organization's opinion of how a business is likely to interact with customers, based on information the BBB can obtain including complaints and public data, and that customer reviews are not used to calculate the letter-grade rating (Better Business Bureau: Overview of Ratings). The BBB complaint process states that a business is generally asked to respond within 14 calendar days and that complaints are commonly closed within about 30 days, with closure labels including resolved, answered, unresolved, unanswered, and unpursuable — an answered complaint does not necessarily mean the customer accepted the response (Better Business Bureau: Complaint Process).

A Strata Trust BBB review should record the exact legal or trade name, address and telephone number, accreditation status, letter rating, customer-review score, complaint totals by time period, complaint categories, company responses, closure labels, alerts or government-action notices, and the observation date. As of July 2026, this research did not verify a BBB profile that could be confidently tied to the exact legal entity shown in a current STRATA custodial agreement, so no STRATA rating, accreditation status, customer-review score, or complaint total is stated here. Any later record should be checked directly and dated — similar names can create false matches, and profiles can change. A public rating or complaint count does not determine whether a company is appropriate for any individual.

Custodian Fee Schedule: What to Get in Writing

Strata Trust fees should be taken from a current written fee schedule, not an old review, search snippet, dealer summary, or unrelated account type. Because the automated research did not retrieve STRATA's current fee pages as of July 2026, no fee amount is asserted in this article. A complete custodian fee schedule should separate the account-establishment fee, annual account-maintenance fee, asset-holding or asset-count fee, percentage-of-value fee (if any), precious-metals transaction fee, real-estate transaction fee, private-asset processing fee, wire-transfer fee, check or ACH fee, document-review fee, expedited-processing fee, returned-payment fee, paper-statement fee, fair-market-value or valuation fee, in-kind distribution fee, cash distribution fee, required minimum distribution processing fee, transfer-out fee, account-termination fee, storage and insurance charges paid to a depository, and dealer charges or spreads paid outside the custodian.

The schedule should state whether each charge is one-time, annual, per transaction, per asset, percentage-based, or payable to a third party. The first-year total and the normal annual total should be calculated separately, because a low setup fee can be offset by recurring asset, transaction, storage, wire, or termination costs. The account agreement should also explain whether a fee can be changed, how notice is delivered, whether unpaid fees can be deducted from account cash, and what happens when the account lacks enough cash to cover charges. The Gold IRA Comparison Workbook can be adapted to compare custodian, dealer, and depository costs side by side.

Depository Relationships and How Metals Are Stored

A gold IRA custodian does not normally keep retail coins or bars in an office drawer. The custody path should identify the dealer, custodian, trustee or depository, account title, storage type, insurance, and distribution process. The IRS states that metals and coins are generally treated as collectibles, subject to limited exceptions for specified coins and qualifying gold, silver, platinum, or palladium bullion; qualifying bullion must meet the applicable fineness rules and remain in the physical possession of a bank or approved nonbank trustee (IRS: Investments in Collectibles).

The storage file should identify the custodian's legal name, the metals dealer's legal name, the depository or approved trustee, the storage location, the account or subaccount title, the product description and quantity, allocated/segregated/commingled treatment, the insurance provider and coverage terms, inventory and audit procedures, shipment instructions, distribution and liquidation procedures, and fees payable to each party. As of July 2026, this research did not verify a current STRATA depository list or storage agreement from a readable company page, so no specific depository relationship is asserted. A depository relationship should be confirmed through the custodian's written account documents and the depository's own agreement — a dealer's statement should not replace that documentation. The Segregated vs Commingled Storage guide explains the storage labels and questions that can be compared. Customers should speak to a financial or tax advisor before making decisions involving precious metals, IRA eligibility, custody, storage, distributions, or tax reporting. Goldco does not offer tax or legal advice.

What a Custodian Does Not Verify

A custodian can perform administrative duties without endorsing the underlying transaction. Investor.gov warns that self-directed IRA custodians generally do not investigate the accuracy of a promoter's financial claims, the value of an asset, the legitimacy of an investment, or whether the investment is appropriate for the account owner. That distinction matters when an account holds precious metals, private-company interests, real estate, promissory notes, tax liens, cryptocurrency, private funds, or other hard-to-value assets. The custodian's willingness to process a transaction should not be described as due diligence on the seller, promoter, dealer markup, asset title, future liquidity, or resale value. For precious metals, the dealer quote should be checked separately for spot reference, premium, total price, shipping, and buyback terms; for private assets, organizational documents, financial statements, valuation methods, management background, conflicts, and exit terms require separate review.

Red Flags Across Self-Directed IRA Custodians

Red flags are reasons to pause and request documents. They are not automatic findings about STRATA or any other custodian.

- The charter or approval category is unclear. The company should identify whether it operates as a bank, state-chartered trust company, approved nonbank custodian, or administrator working with another custodian.

- The account agreement names a different entity. A related entity may have a valid role, but the relationship should be explained in writing before funds move.

- Fees are spread across several documents. Custodian, dealer, storage, wire, transaction, and termination charges should be combined into one total-cost worksheet.

- Custodian acceptance is presented as asset approval. Investor.gov states that administrative acceptance is not an evaluation of the investment or promoter.

- Depository terms are missing. The storage location, account title, insurance, inventory method, audit process, and distribution procedure should be documented.

- Complaint channels are vague. The custodian should provide internal escalation procedures and the applicable regulator complaint channel. The Texas Department of Banking states that its Consumer Assistance Activities investigates complaints involving institutions supervised by the department (Texas DoB: File a Complaint).

- Transaction processing is not explained. The account agreement should state required documents, normal processing times, funding rules, valuation requirements, and conditions that can delay or reject a transaction.

- Transfer-out or closure fees are not disclosed. Exit costs and document requirements should be known before the account is opened.

How This Custodian Fits a Broader Comparison

A Strata Trust Company review should compare verified fields rather than assign a verdict. The comparison worksheet should include the exact legal entity, chartering or approving authority, entity-search result and date, account types supported, asset types accepted, setup fee, annual maintenance fee, transaction fees, asset-holding fees, wire and distribution fees, transfer-out and closure fees, precious-metals procedure, depository options, storage and insurance terms, service turnaround standards, online access and statement process, complaint and escalation channels, and the current BBB profile when verified. Blank fields should remain labeled "not verified" — they should not be filled with estimates from another custodian. The Gold IRA Companies Comparison provides broader provider research, while the Gold IRA Quiz can organize account questions. Neither tool replaces the custodian agreement, regulator record, or professional advice.

Questions to Ask Before Opening an Account

- What is the custodian's full legal name, and is the entity a bank, state-chartered trust company, approved nonbank custodian, or administrator?

- Which regulator or chartering authority supervises the entity, and what public record confirms current status (and charter/registration number)?

- What legal entity appears on tax forms, and which agreement controls the account?

- Which asset types are accepted, and which are not?

- What is the full first-year cost and the normal annual cost?

- Are fees flat, asset-based, transaction-based, or value-based, and which third-party charges are excluded?

- What cash balance is required for fees, and how are fee changes announced?

- What documents are required for a metals purchase?

- Which depositories are available, and who selects the depository?

- How is the storage account titled, and which insurance terms apply?

- How are holdings inventoried and audited, and how are fair-market values reported?

- How are distributions and required minimum distributions processed?

- What are the transfer-out and closure procedures?

- Which internal complaint channel and which regulator complaint portal apply?

- What service turnaround times are stated, which duties are excluded from the custodian's role, and will every material answer be supplied in writing?

Frequently Asked Questions

Is STRATA Trust Company a precious-metals dealer?

This review evaluates STRATA in the custodian role, not as a dealer. A custodian administers the IRA, while a precious-metals dealer sells the product and sets the purchase and buyback prices. The current custodial agreement should identify the exact STRATA legal entity and duties.

Is STRATA Trust Company on the IRS approved nonbank trustee list?

No claim is made here about STRATA's presence on the current list. The IRS page applies to approved nonbank trustees and custodians. A bank or state-chartered trust company should also be checked through its chartering regulator.

What are STRATA Trust fees?

No current STRATA fee amount is asserted because the company's current fee pages were not accessible through the July 2026 automated research. The dated fee schedule and custodial agreement should be obtained directly.

Does a self-directed IRA custodian verify a metals dealer?

Not generally. Investor.gov warns that self-directed IRA custodians usually do not evaluate the legitimacy, quality, or financial merit of the investment or promoter.

How should a depository relationship be verified?

The custodian agreement and depository documents should identify the storage location, account title, storage method, insurance, fees, inventory procedures, audits, shipment process, and distribution terms.

Does a BBB rating determine whether a custodian is appropriate?

No. The BBB states that its rating is one information source and that customer reviews are not used in the letter-grade calculation. A public rating or complaint count does not determine whether a company is appropriate for any individual.

Conclusion

A useful Strata Trust Company review should not depend on a single rating, fee number, dealer statement, or search result. The stronger method confirms the legal entity, checks the correct regulator, distinguishes a state charter from IRS nonbank approval, reads the custodial agreement, combines every fee, verifies the depository process, and keeps dealer due diligence separate from custodian administration. Current company pages were not readable through the automated July 2026 research, so no STRATA fees, ratings, complaint totals, depository partners, or service terms are asserted here. Records and account terms can change — each source should be re-checked directly. A public rating or complaint count does not determine whether a company is appropriate for any individual.

Sources

- STRATA Trust Company. Official Website.

- Internal Revenue Service. Approved Nonbank Trustees and Custodians.

- Internal Revenue Service. Investments in Collectibles in Individually Directed Qualified Plan Accounts.

- Internal Revenue Service. Retirement Plans FAQs Regarding IRAs.

- Investor.gov. Self-Directed IRAs and the Risk of Fraud.

- Better Business Bureau. Overview of BBB Ratings.

- Better Business Bureau. Complaint Process.

- Texas Department of Banking. Homepage.

- Texas Department of Banking. Banks & Trust Companies.

- Texas Department of Banking. Trust Companies.

- Texas Department of Banking. Entity Search.

- Texas Department of Banking. File a Complaint.

Article reviewed and edited by Daniel M. — editor, 401kToGoldIRA.org. A neutral verification framework sourced to the IRS, Investor.gov, the Texas Department of Banking, and the BBB; educational only, not an endorsement, verdict, or tax or legal advice.