Educational only: This is a neutral verification framework, not a fact-asserting review or an endorsement. It reports company-published and independent records dated to July 2026, separates company claims from independent records, and leaves unverified fields blank. A public rating or complaint count does not determine whether a company is appropriate for any individual. Customers should speak to a financial or tax advisor before making decisions. Goldco does not offer tax or legal advice. Past performance does not guarantee future results.

As of July 2026, Forge Trust's website identified Forge Trust Co. as a self-directed custodian, and the South Dakota Division of Banking's current trust-company records also listed Forge Trust Co. as a public trust company. Those records can change and should be re-checked directly (Forge Trust; South Dakota Division of Banking).

Quick Answer: What a Self-Directed IRA Custodian Does and Does Not Do

A self-directed IRA custodian administers the retirement account. Common duties can include opening the account, receiving transfers or rollovers, processing investment instructions, holding or recording assets, maintaining account records, issuing statements, processing distributions, collecting annual valuations, and completing required tax reporting under the account agreement (Forge Trust: How It Works). A custodian is not the precious-metals dealer — the dealer quotes and sells the metal, a depository or qualified trustee physically holds eligible bullion for the IRA, and the custodian records and administers the transaction under the retirement account.

A custodian also does not automatically investigate the quality, legitimacy, price, or suitability of an alternative asset or promoter. Investor.gov warns that self-directed IRA custodians generally have limited duties and may not evaluate the investment or promoter merely because the asset is accepted for account administration (Investor.gov: Self-Directed IRAs and the Risk of Fraud). Forge Trust states that it does not provide due diligence or tax, legal, or investment advice and does not sell, evaluate, recommend, or endorse investments, dealers, platforms, sponsors, or service providers — that company statement appeared on its site as of July 2026 and should be re-checked directly (Forge Trust). The practical lesson is simple: custodian acceptance is an administrative step, not an endorsement. The asset sponsor, dealer, valuation, pricing, legal structure, storage arrangement, and related parties still require independent review. Customers should speak to a financial or tax advisor before making decisions involving an IRA, rollover, asset purchase, distribution, valuation, prohibited transaction, or custody arrangement. Goldco does not offer tax or legal advice. The Questions to Ask Before Opening a Gold IRA guide provides a related checklist.

Forge Trust Reviews: Start With the Legal and Regulatory Identity

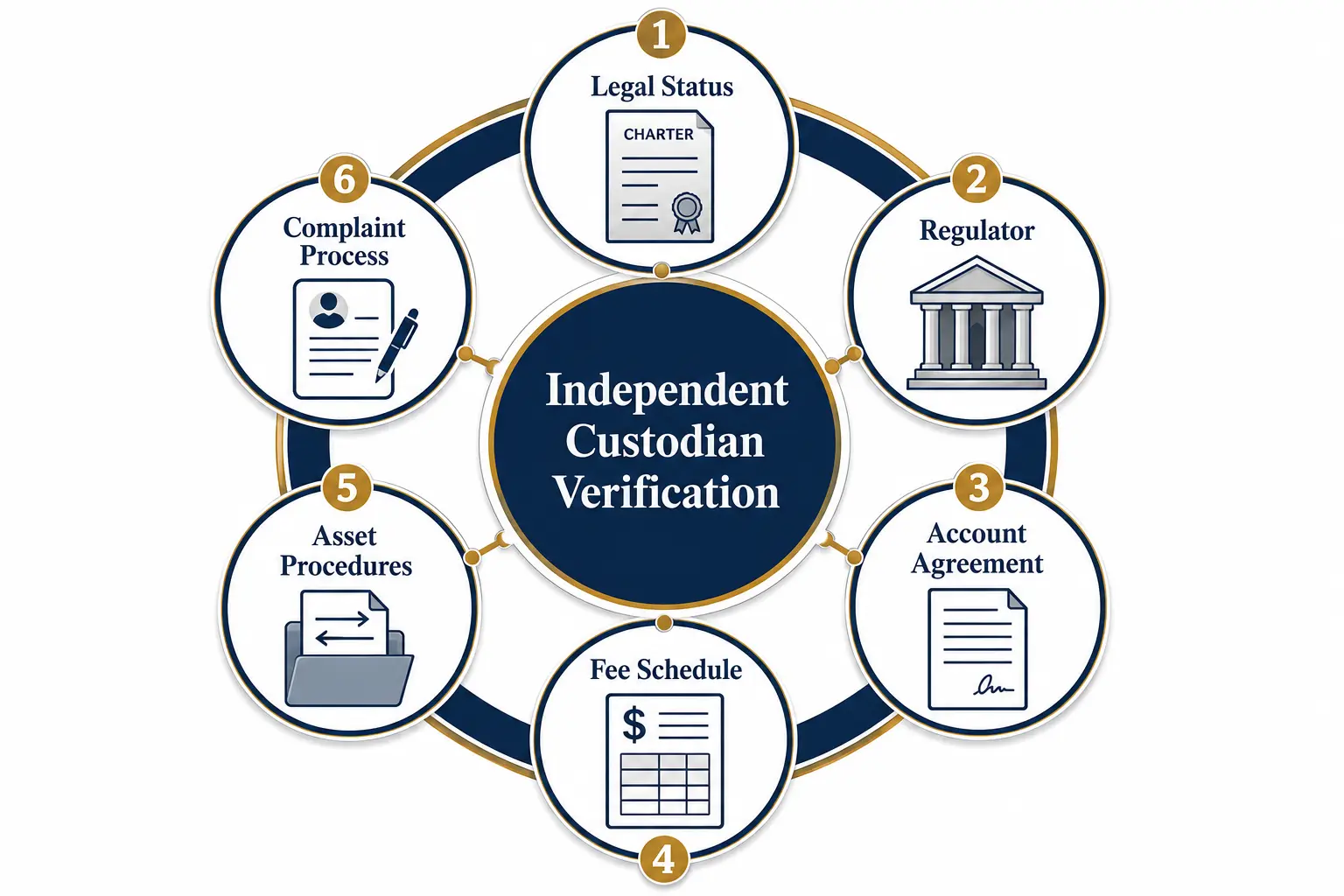

A Forge Trust review should begin with the exact legal name shown on the account agreement, payment instructions, tax forms, state charter records, and customer portal. As of July 2026, the official site used the name Forge Trust Co. and stated that the company was formerly IRA Services Trust Co. The same page described Forge Trust as a non-depository trust company chartered by South Dakota and regulated by the South Dakota Division of Banking (Forge Trust: About).

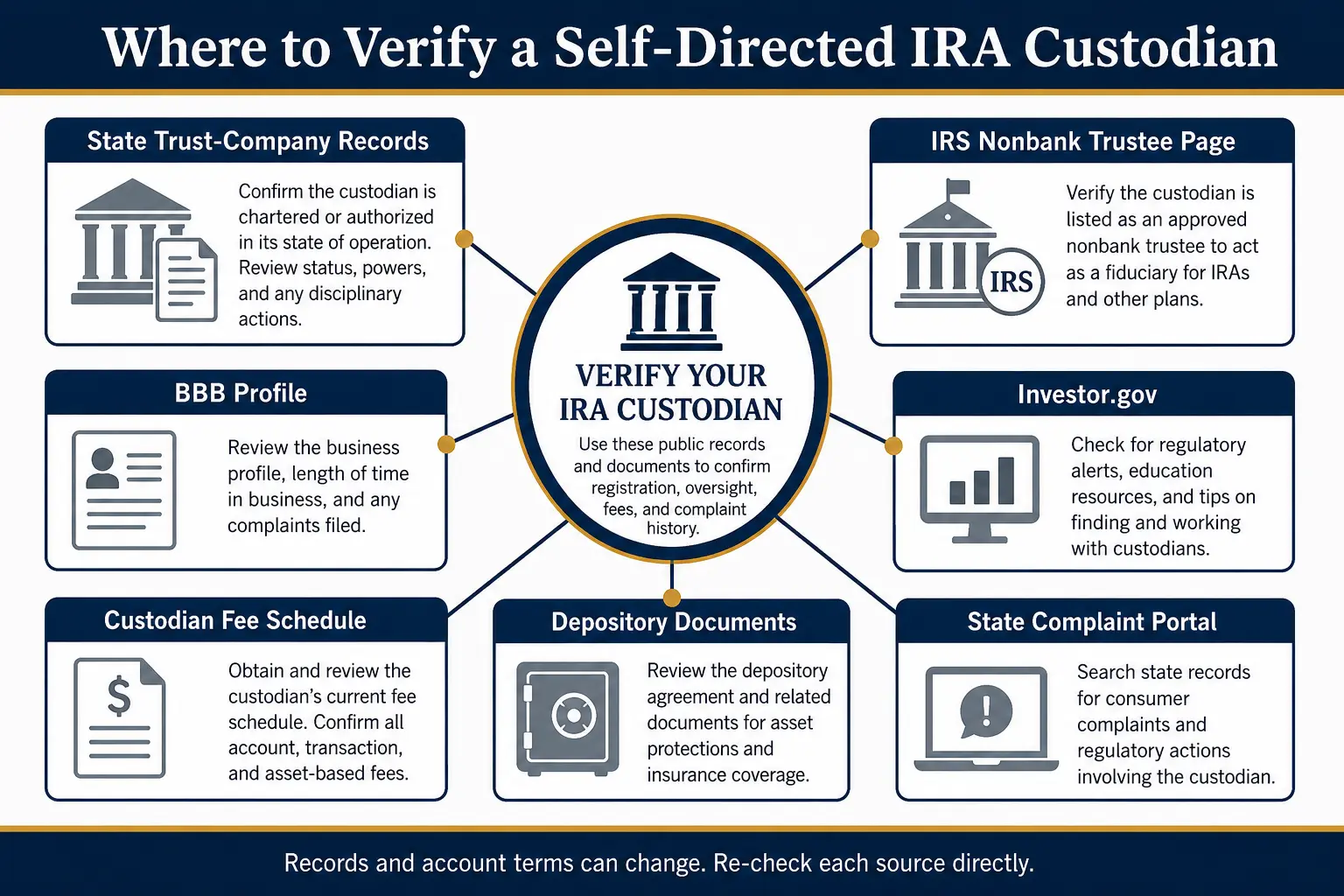

The South Dakota Division of Banking maintains a Trust Companies page and links to its current list of companies licensed to do business in the state; the July 2026 list accessed through that page included Forge Trust Co. as a public trust company. The regulator's page also explains that the Division supervises state-chartered trust companies and provides a complaint process for regulated institutions (South Dakota Division of Banking: Trusts; SD Division of Banking: Consumers). That state record verifies charter status at the observation date — it does not establish that every account type, asset, service level, fee, dealer, depository, or transaction is appropriate for an individual.

Forge Trust also stated as of July 2026 that it is part of Forge Global and that Forge Global is wholly owned by The Charles Schwab Corporation. That ownership statement came from the company's own page and can change, so it should be re-checked directly before publication or account opening. The legal-identity file should contain the exact custodian name, the state charter or license record, the custodian's physical and mailing addresses, the account agreement, the fee schedule, the name shown on checks and wire instructions, the customer-service and fraud-reporting contacts, the legal name of any dealer/asset sponsor/administrator/depository, and the observation date for every public record. A public rating or complaint count does not determine whether a company is appropriate for any individual.

How to Verify a Custodian With the IRS and State Regulator

The IRS maintains an Approved Nonbank Trustees and Custodians page for entities approved under Treasury Regulation Section 1.408-2(e). As of July 2026, the IRS page linked to a list dated April 1, 2026 and stated that the list would be updated as entities were added, removed, corrected, or changed (IRS: Approved Nonbank Trustees and Custodians). That IRS list is one verification path and should not be used without understanding the entity's legal status: a bank, state-chartered trust company, federally insured credit union, savings institution, or IRS-approved nonbank trustee can serve in different legal categories. The IRS page specifically addresses approved nonbank trustees and custodians, while a state-chartered trust company should also be checked with its state regulator.

For Forge Trust, the official company page and South Dakota regulator records identify a state-chartered public trust company, so the South Dakota charter record is a key verification source; the IRS nonbank page remains useful for understanding the separate approval route used by entities that rely on IRS nonbank-trustee approval. A complete self-directed IRA custodian verification should record the custodian's exact legal name, whether the entity is a bank/credit union/state-chartered trust company/approved nonbank trustee, the regulator or approval authority, the license or charter status on the observation date, the address shown by the regulator, any name change or former name, the account agreement that names the custodian, and the complaint channel for the correct regulator. No single logo or marketing claim should replace those checks.

Reading the BBB Profile and Complaint Records

A BBB profile can add context, but the rating, accreditation status, customer-review score, and complaint records should be read separately. As of July 2026, the BBB stated that its letter rating represents the organization's opinion of how a business is likely to interact with customers, that ratings use information it can obtain (including complaints and public data), that customer reviews are not included in the letter-grade calculation, and that its ratings are not assurances of reliability or performance (Better Business Bureau: Overview of Ratings). The BBB complaint-process page stated as of July 2026 that businesses are generally asked to respond within 14 days and complaints are generally closed within about 30 days, with closure descriptions including resolved, answered, unresolved, unanswered, and unpursuable — an answered complaint does not necessarily mean the customer accepted the response (Better Business Bureau: Complaint Process).

A Forge Trust BBB review should record the exact entity name and address, accreditation status, letter rating, customer-review score, complaint totals by period, complaint categories, business responses, closure descriptions, alerts or government-action notices, and the date the profile was viewed. This research did not verify a BBB profile that could be confidently matched to Forge Trust Co. as of July 2026, so no Forge Trust BBB rating, accreditation status, customer-review score, or complaint total is asserted here. A later profile may appear or change, and similar names and former names can also affect search results — any record should be matched to the exact legal entity and dated. The South Dakota Division of Banking provides an online process for complaints against institutions it regulates, and its consumer page states that the Division regulates state-chartered trust companies and provides links for verifying trust-company status and filing complaints. A public rating or complaint count does not determine whether a company is appropriate for any individual.

Custodian Fee Schedule: What to Get in Writing

Forge Trust fees should be taken from the current fee schedule and account agreement, not from an old review, a search snippet, or another custodian's pricing. As of July 2026, Forge Trust's Forms page included a section for Terms and Disclosures and a link labeled "Fee Schedule and Financial Disclosure," and linked to account disclosures and custodial agreements for several account types; the page can change and should be re-checked directly (Forge Trust: Forms). This article does not reproduce specific Forge Trust fee amounts because the current amounts should be confirmed from the company's live disclosure before an account is opened or transferred.

A complete custodian fee schedule should address new-account establishment, annual account administration, cash or asset transfers, wire/check/ACH processing, asset purchase and sale processing, per-asset or asset-value charges, private-investment review or maintenance, real-estate administration, IRA-LLC administration, precious-metals transaction processing, annual valuation handling, tax-form or special-reporting charges, distribution and in-kind distribution charges, required minimum distribution processing, Roth conversion processing, account termination and transfer-out, expedited/correction/research/special-service charges, and third-party dealer/storage/insurance/legal/appraisal/state fees. The schedule should state which amounts are one-time, annual, transaction-based, asset-based, or paid to third parties, and explain when fees are collected, whether cash must remain in the account, what happens when cash is insufficient, and whether pricing differs by asset type. A low annual fee can be offset by transaction, asset, wire, distribution, valuation, storage, or termination charges, so a useful comparison should calculate the first-year cost and the normal recurring-year cost under the same assumptions. The Gold IRA Comparison Workbook can be adapted to compare custodian fees, dealer spreads, depository charges, and transaction costs side by side.

Depository Relationships and How IRA Metals Are Stored

A gold IRA custodian is not normally the retail metals dealer, and the custodian's office is not automatically the storage location. As of July 2026, Forge Trust's precious-metals page stated that the account owner is responsible for choosing the precious-metals dealer, selecting the metal, and negotiating the purchase, and that the IRA owner cannot take possession and must select a metals depository to hold the metal on behalf of Forge Trust as custodian (Forge Trust: Precious Metals IRA). Forge Trust's Forms page described precious-metals administration as purchasing and managing metals, including authorizing storage with a third-party depository, and included purchase, liquidation, and maintenance forms — those procedures can change and should be re-checked directly.

The IRS states that metals and coins are generally collectibles, subject to limited exceptions; qualifying bullion must meet the statutory requirements and be kept in the physical possession of a bank or approved nonbank trustee, and the physical-possession rule applies to indirect arrangements such as an IRA-owned LLC buying the bullion (IRS: Investments in Collectibles; IRS: Retirement Plans FAQs). The storage file should identify the IRA custodian, the metals dealer, the depository or trustee, the exact account title at the depository, the storage method, insurance terms, audit or inventory procedures, shipment instructions, authorized transaction parties, valuation records, liquidation and distribution procedures, and all custodian/dealer/shipping/storage charges. Segregated and commingled storage can have different operational and fee features — the Segregated vs Commingled Storage guide explains the terms and the questions that should be asked. Customers should speak to a financial or tax advisor before making decisions involving an IRA, rollover, precious-metals purchase, depository, personal possession, valuation, liquidation, or distribution. Goldco does not offer tax or legal advice.

Red Flags Across Self-Directed IRA Custodians

Red flags are reasons to pause and verify. They are not automatic findings about Forge Trust or any other custodian.

- The legal entity cannot be confirmed. A custodian should have a verifiable legal name, regulator, charter or approval path, address, account agreement, and payment instructions.

- Custodian acceptance is presented as investment approval. Investor.gov warns that self-directed IRA custodians may not evaluate the legitimacy, quality, price, or suitability of an investment or promoter.

- The fee schedule is incomplete. The written schedule should include setup, annual, transaction, asset, valuation, distribution, transfer-out, termination, and third-party costs.

- Dealer, custodian, and depository roles are blended. Each legal entity should be named separately — the dealer sells the asset, the custodian administers the account, and the depository or trustee holds eligible physical metal.

- Complaint totals are used as a verdict. Complaint counts require context such as account volume, business history, response quality, closure status, and the exact legal entity.

- Valuation duties are unclear. Alternative assets may require annual fair-market-value documentation; Forge Trust's Forms page includes valuation forms and states that annual valuations must be submitted for IRA assets. The required method and supporting evidence should be confirmed for the specific asset.

- Personal possession of IRA metals is suggested. The IRS states that qualifying bullion must remain in the required physical-possession arrangement; personal possession or home-storage claims require independent tax and legal review.

- No complaint or escalation process is provided. The custodian should provide internal escalation contacts and the correct state or federal regulator. The South Dakota Division of Banking provides a complaint process for state-chartered trust companies.

How Forge Trust Fits a Broader Comparison

A comparison should not rank Forge Trust from a single fee, review score, or marketing statement. As of July 2026, Forge Trust's official pages described the company as a self-directed custodian serving alternative assets, including real estate, private investments, promissory notes, IRA LLCs, and precious metals, and its Forms page showed separate workflows for account opening, funding, investments, valuations, distributions, and disclosures — those descriptions can change and should be re-checked directly. A broader comparison should use the same fields for each custodian: legal and regulatory status, account types, accepted asset types, current fee schedule, transaction turnaround standards, online account access, valuation process, distribution process, precious-metals procedures, depository flexibility, customer-service contacts, complaint and escalation channels, transfer-out and termination terms, and cybersecurity and privacy disclosures. A blank or unverified field should remain blank — it should not be filled with an estimate from another custodian. The Gold IRA Companies Comparison can provide broader dealer and provider context, and the Gold IRA Quiz can help organize research questions, but neither tool determines whether an account or custodian is appropriate.

Questions to Ask Before Opening an Account

- What is the custodian's exact legal name, and is the entity a bank, credit union, state-chartered trust company, or IRS-approved nonbank trustee?

- Which regulator or authority verifies that status, and what is the current charter, license, or approval record?

- What former names or affiliated entities should appear in searches?

- Which IRA and plan account types are supported, and which alternative assets are accepted or not accepted?

- What is the complete current fee schedule, and which fees are one-time, annual, transaction-based, or asset-based?

- Which third-party fees may apply, and how much cash must remain in the account for fees?

- How are investment instructions submitted and approved, and what documents are required for each asset type?

- Which valuation documents are required each year, and how are tax forms and account statements delivered?

- What are the normal transaction-processing times, and how are errors or disputed instructions handled?

- Which internal escalation contacts are available, and which regulator accepts complaints?

- For metals, who selects the dealer and the depository, and which depositories can be used?

- How is the depository account titled, and what storage, insurance, and audit records are provided?

- How are metals sold or distributed, and what transfer-out and account-closing charges apply?

- Does the custodian evaluate the investment or promoter, and which responsibilities remain with the account owner?

- Will every material term be provided in writing before funding?

Frequently Asked Questions

Is Forge Trust a self-directed IRA custodian?

As of July 2026, Forge Trust's official site identified Forge Trust Co. as a self-directed custodian. The South Dakota Division of Banking's current trust-company records also listed Forge Trust Co. as a public trust company. Those records can change and should be re-checked directly.

Is Forge Trust on the IRS approved nonbank trustee list?

No claim is made here about Forge Trust appearing on the IRS nonbank list. The company and South Dakota records identify Forge Trust as a state-chartered trust company. The IRS nonbank list is a separate verification route for entities approved under Treasury Regulation Section 1.408-2(e). Both the legal category and the correct regulator should be confirmed.

Does Forge Trust evaluate investments or precious-metals dealers?

Forge Trust states that it does not provide due diligence or evaluate, recommend, or endorse investments, dealers, platforms, sponsors, or service providers. Investor.gov gives the same general caution about limited self-directed IRA custodian duties.

What Forge Trust fees should be compared?

The comparison should include setup, annual administration, transactions, asset maintenance, wires, distributions, valuations, transfer-out, termination, and third-party dealer or storage charges. The current Forge Trust Forms page links to its Fee Schedule and Financial Disclosure, which should be reviewed directly.

Does Forge Trust store IRA metals at its office?

The company's precious-metals page states that a selected metals depository holds the metal on behalf of Forge Trust as custodian. The exact depository, storage method, insurance, and account title should be confirmed in the transaction documents.

Does custodian acceptance mean an asset is legitimate?

No. Investor.gov warns that acceptance by a self-directed IRA custodian does not mean the custodian has checked the quality, legitimacy, price, or suitability of the investment or promoter.

Conclusion

A useful Forge Trust review should not depend on one rating, fee number, or company statement. The stronger process confirms the legal entity, state charter, regulatory status, custodian agreement, current fee schedule, complaint channel, transaction procedures, valuation duties, and depository arrangement — and keeps the custodian separate from the dealer, asset sponsor, and storage provider. As of July 2026, official Forge Trust and South Dakota records supported the company's identity as a self-directed custodian and state-chartered public trust company; those records do not decide whether a specific account, asset, dealer, fee structure, or storage arrangement is appropriate. Public records and account terms can change — each source should be re-checked directly. A public rating or complaint count does not determine whether a company is appropriate for any individual.

Sources

- Forge Trust. Official Website.

- Forge Trust. About Forge Trust.

- Forge Trust. How It Works.

- Forge Trust. Forms & Disclosures.

- Forge Trust. Precious Metals IRA.

- South Dakota Division of Banking. Trust Companies.

- South Dakota Division of Banking. Information for Consumers.

- Internal Revenue Service. Approved Nonbank Trustees and Custodians.

- Internal Revenue Service. Investments in Collectibles in Individually Directed Qualified Plan Accounts.

- Internal Revenue Service. Retirement Plans FAQs Regarding IRAs.

- Investor.gov. Self-Directed IRAs and the Risk of Fraud.

- Better Business Bureau. Overview of BBB Ratings.

- Better Business Bureau. Complaint Process.

Article reviewed and edited by Daniel M. — editor, 401kToGoldIRA.org. A neutral verification framework sourced to the company's own dated records, the South Dakota Division of Banking, the IRS, Investor.gov, and the BBB; educational only, not an endorsement, verdict, or tax or legal advice.