Educational only: This is a neutral verification framework, not a fact-asserting review or an endorsement. As of July 2026, current Broad Financial primary-source material could not be reliably retrieved, so no fees, ratings, complaint totals, or custodian relationships are attributed to it here. A public rating or complaint count does not determine whether a company is appropriate for any individual. Customers should speak to a financial or tax advisor before making decisions. Goldco does not offer tax or legal advice. Past performance does not guarantee future results.

Quick Answer: What to Verify Before Using a Self-Directed IRA Provider

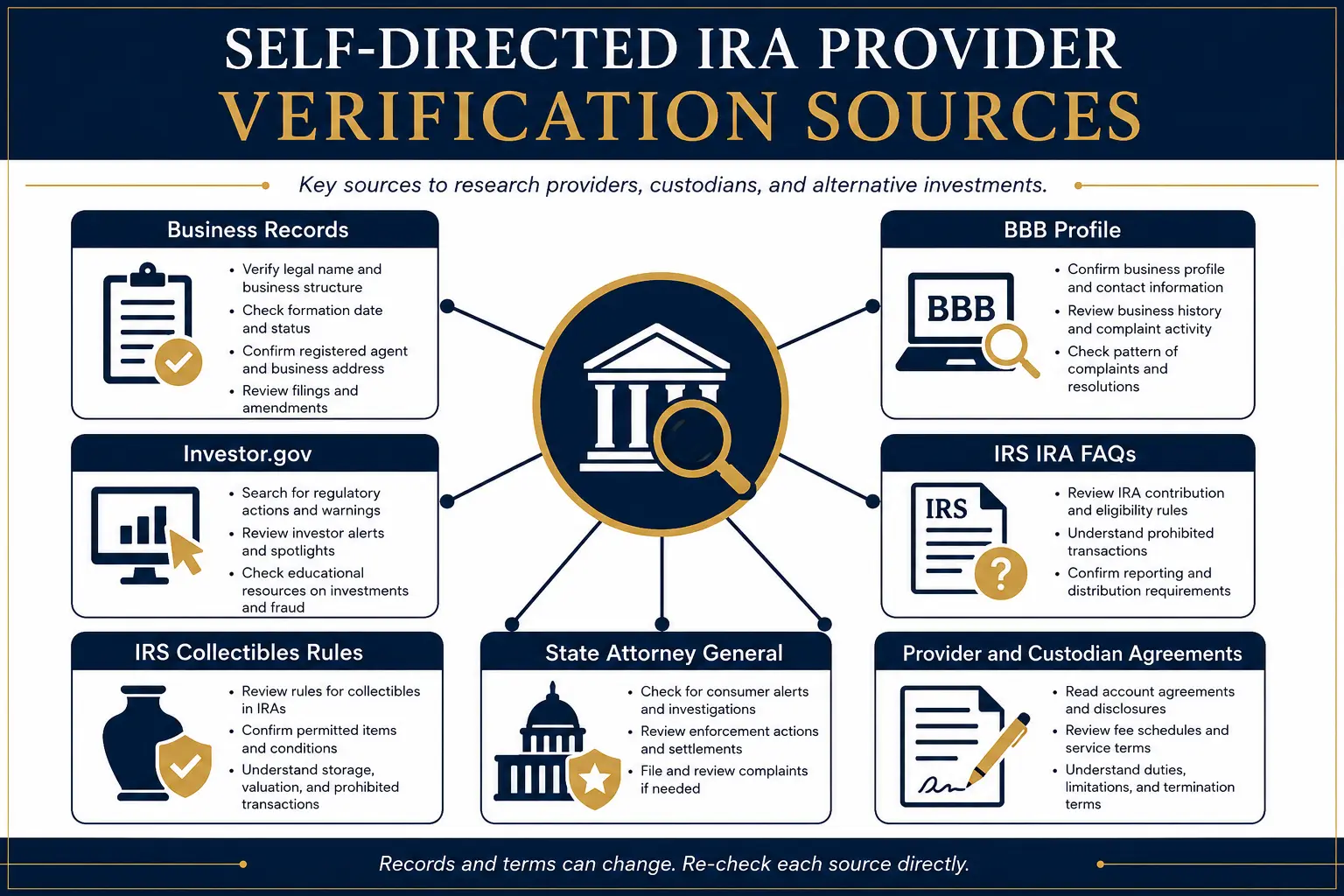

Self-directed IRA provider verification begins by identifying each party and each contract. First, determine whether the company is the IRA custodian, an administrator, a facilitator, an LLC-document provider, or a coordinator that works with a separate custodian. Investor.gov explains that a self-directed IRA custodian generally holds and administers the account but may not evaluate the quality, legitimacy, or financial merit of an alternative asset or promoter (Investor.gov: Self-Directed IRAs and the Risk of Fraud). Second, confirm which legal entity signs each agreement — the provider agreement, custodian application, LLC operating agreement, bank account documents, asset-purchase instructions, and storage agreement may involve different entities. Third, confirm every fee is listed in dollars, covering setup, legal-document preparation, state LLC filing, registered agent, custodian establishment, annual administration, asset holding, transaction processing, wires, checks, termination, tax reporting, storage, insurance, and amendments.

Fourth, determine who has legal possession or control of each asset. The IRS states that an IRA must be held by a trustee or custodian that is a bank, federally insured credit union, savings and loan association, or another entity approved by the IRS (IRS: Retirement Plans FAQs Regarding IRAs). Fifth, determine whether the proposed asset, transaction, bank account, payment, or personal role could create a prohibited transaction. The IRS describes prohibited transactions as improper uses of an IRA by the owner, beneficiary, or a disqualified person, including certain sales, exchanges, loans, extensions of credit, transfers, or uses of plan assets (IRS: Prohibited Transactions). Sixth, confirm the structure has received independent tax and legal review — an IRA-LLC can add control, but it also adds entity law, banking, recordkeeping, valuation, prohibited-transaction, and custody questions. Customers should speak to a financial or tax advisor before making decisions involving an IRA, rollover, LLC, asset purchase, distribution, prohibited transaction, or custody arrangement. Goldco does not offer tax or legal advice. The Questions to Ask Before Opening a Gold IRA guide provides a related checklist.

Broad Financial Reviews: Verify the Provider Before the Product

A defamation-safe review does not begin with a verdict — it begins with a document trail. A Broad Financial review should first confirm the full legal business name, state of formation, business address, telephone number, website domain, assumed names, and the entity that receives payment. A state business filing can help confirm formation and status, but it does not measure service quality, tax compliance, pricing fairness, or suitability. The exact service should also be named: "self-directed IRA," "checkbook IRA," "checkbook control IRA," and "IRA LLC" can describe related but different arrangements. The account may include a provider that prepares or coordinates documents, a custodian that administers the IRA, an LLC owned by the IRA, a bank account titled to the LLC, and one or more underlying investments.

As of July 2026, this research did not retrieve a Broad Financial company page or fee schedule reliably enough to quote current terms. Therefore, no Broad Financial fees, minimums, custodian identity, annual charges, or included services are stated here. That research result is not a finding about the company — it means the current provider agreement, custodian agreement, LLC documents, and fee schedules should be obtained directly and preserved before funds move. A public rating or complaint count does not determine whether a company is appropriate for any individual.

Provider vs. Custodian: Who Is Responsible for What

The word "provider" can create confusion because it does not always identify the regulated account custodian.

The Provider or Facilitator

A provider may explain the structure, coordinate account opening, prepare an IRA-LLC package, arrange state filings, provide educational material, or connect the customer with a third-party custodian — the exact scope depends on the contract. The provider's agreement should state whether the provider gives legal, tax, investment, valuation, accounting, or compliance advice. A disclaimer should not be treated as a substitute for understanding which tasks remain with the account owner and outside professionals.

The Independent Custodian

The IRA custodian administers the retirement account. Investor.gov warns that self-directed IRA custodians may have limited duties and generally do not investigate or validate the underlying investment merely because the custodian accepts the asset for administration. A custodian may process contributions, rollovers, purchases, sales, distributions, statements, and tax reporting, and the account agreement controls which assets the custodian will accept and which procedures apply. Custodian acceptance does not establish that an asset is lawful, fairly priced, appropriate, liquid, or free from conflicts — self-directed IRA due diligence remains separate from account administration.

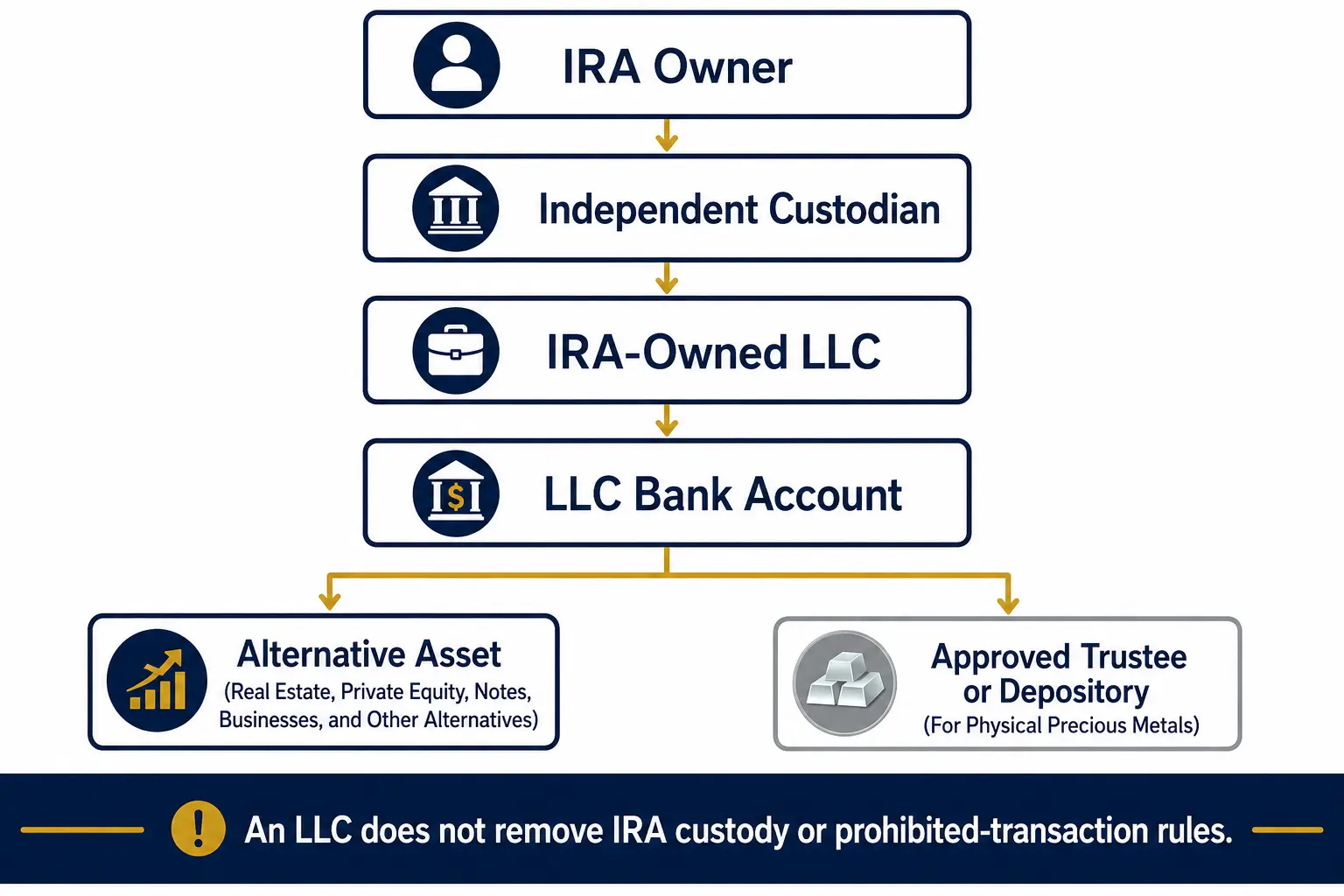

The IRA-Owned LLC and the Other Parties

In a checkbook IRA structure, the IRA may acquire an ownership interest in an LLC, which may then hold a bank account and acquire assets under the operating agreement. That layer does not remove the IRA rules: the LLC's funds remain retirement assets when the IRA owns the entity, and payments, contracts, benefits, related parties, compensation, personal use, and possession still require analysis under the tax rules. A bank may hold the LLC checking account, an asset sponsor may issue a private investment, a dealer may sell physical metal, and a depository may hold qualifying bullion — each entity should be verified separately. The Gold IRA Companies Comparison can provide broader provider-research context, but it does not replace verification of the actual custodian or account agreement.

Checkbook Control and the IRA-LLC Structure

A checkbook IRA commonly uses an LLC owned by the IRA. The account holder may serve as manager of the LLC and direct payments from an LLC bank account, often to reduce the need for a custodian to process each underlying payment. That description does not decide whether a specific structure or transaction complies with tax law — the documents, parties, asset, manager powers, payment flow, personal benefit, and possession arrangement matter. The verification file should include the custodian's account agreement, the IRA application and adoption documents, the LLC articles or certificate of formation, the operating agreement, the employer identification number record, the bank account title and signature card, the provider agreement, the provider and custodian fee schedules, asset-purchase contracts, valuation and annual reporting procedures, distribution procedures, a written prohibited-transaction review, and independently obtained tax and legal opinions.

The operating agreement should state that the IRA owns the membership interest, the bank account title should identify the LLC rather than a personal account, and personal funds and retirement funds should not be mixed. A checkbook control IRA can create operational speed, but speed does not reduce the need for documentation — an immediate payment can make a prohibited transaction easier to complete before a custodian or professional sees it. The IRS prohibited-transaction page lists dealings that can create problems, including certain sales or exchanges between the plan and a disqualified person, loans or extensions of credit, furnishing goods or services, transfers of plan income or assets, and self-dealing by a fiduciary. Customers should speak to a financial or tax advisor before making decisions involving a checkbook IRA, checkbook control IRA, IRA LLC, bank account, manager role, asset purchase, or related-party transaction. Goldco does not offer tax or legal advice.

The IRS Custody Rule for IRA Metals

Physical precious metals create a separate custody question. The IRS states that IRA investments in collectibles are generally treated as distributions; the collectible category includes art, rugs, antiques, metals, gems, stamps, coins, alcoholic beverages, and certain other tangible personal property, subject to statutory exceptions for specified coins and qualifying bullion (IRS: Investments in Collectibles). For qualifying bullion, the metal must be in the physical possession of a bank or an approved nonbank trustee — that rule should be reviewed before a checkbook IRA or IRA-owned LLC buys, receives, ships, stores, or moves physical metal.

The custody path should identify the IRA custodian, the IRA-owned LLC when one is used, the metals dealer, the trustee or depository holding the metal, the account or subaccount title at the storage facility, the party permitted to issue instructions, the distribution process, the insurance and audit records, the valuation process, and the chain of possession from purchase through storage. A provider's marketing statement should not replace written confirmation from the custodian, depository, and an independent tax professional. The Gold IRA Storage Options guide can help organize questions about storage type, custody, insurance, and account records.

The Home-Storage Risk and the McNulty Case

The 2021 McNulty v. Commissioner case is important because it addressed personal possession of IRA-owned coins through an LLC structure. A summary in the Journal of Accountancy reported that the Tax Court treated IRA gold held at home by the account owners as taxable, describing a case in which a couple stored IRA-owned coins at home and faced substantial tax and penalty consequences after the court's ruling (Journal of Accountancy). The lesson should be stated narrowly: McNulty does not mean that every IRA-owned LLC is invalid — it shows that an LLC layer does not automatically permit personal possession of IRA metals or erase the custody requirements.

A proposed home-storage IRA arrangement should therefore receive independent legal and tax review before any purchase or transfer, addressing the exact product, statutory coin or bullion exception, trustee requirement, physical possession, LLC manager powers, storage location, personal control, insurance, distribution treatment, and reporting. A structure that may work for one type of nonphysical asset should not be assumed to work for coins or bullion — the custody rule applies to the metal, not only to the name on the LLC documents. Customers should speak to a financial or tax advisor before making decisions involving home storage, an IRA-owned LLC, precious metals, custody, possession, or distributions. Goldco does not offer tax or legal advice.

Reading the BBB Profile and Complaint Records

A BBB profile can be one part of broad financial complaints research, but it should be read carefully. As of July 2026, the BBB's rating overview stated that its letter grade reflects the organization's opinion about how a business is likely to interact with customers, listing factors such as complaint history, business type, time in business, transparency, licensing or government actions known to the BBB, advertising issues, and failure to honor commitments, and that customer reviews do not determine the letter grade (Better Business Bureau: Overview of Ratings). As of July 2026, the BBB complaint-process page explained that businesses are generally asked to respond within 14 calendar days and that complaints are commonly closed with descriptions such as resolved, answered, unresolved, unanswered, or unpursuable (Better Business Bureau: Complaint Process).

A Broad Financial BBB review should record the exact legal name and address, accreditation status, letter rating, customer-review score, complaint totals by time period, complaint categories, business responses, closure descriptions, alerts or government-action notices, and the date of observation. As of July 2026, this research did not verify a Broad Financial BBB profile that could be confidently tied to a confirmed legal entity, so no rating, accreditation status, customer-review score, or complaint total is stated here — that can change, and any later record should be dated and re-checked directly because similar names can create false matches. State attorney general websites may also publish alerts, settlements, lawsuits, or other public records; the National Association of Attorneys General provides a directory for locating the appropriate state office (NAAG: Find My AG). The FTC accepts consumer reports through its reporting channel, which is not a public company-rating database (FTC: ReportFraud). A public rating or complaint count does not determine whether a company is appropriate for any individual.

Fee Schedule and Account Terms to Get in Writing

Broad Financial fees should not be estimated from an old review, a directory listing, or another company's schedule. The written cost file should separate the provider from the custodian and other parties, identifying the provider setup fee, LLC drafting or document fee, state formation fee, state annual report or franchise fee, registered-agent fee, custodian establishment fee, custodian annual administration fee, asset-based or asset-count fee, transaction fee, wire/check/ACH fee, precious-metals dealer spread, depository storage and insurance, valuation fee, tax-form or special-reporting fee, account amendment fee, distribution fee, LLC dissolution fee, and account termination or transfer-out fee. The schedule should say which charges are one-time, annual, transaction-based, asset-based, or payable to a third party, and any promotional waiver should state its duration and the regular charge after it ends.

The account agreement should also explain service limits: a provider may prepare documents without monitoring later transactions, a custodian may report the account without reviewing each LLC payment, and an attorney may review the formation but not future asset purchases — those boundaries should be clear. A low setup price can be offset by annual entity, custodian, banking, storage, transaction, or professional-service costs, so a single total for the first year and a separate normal-year estimate provide a better comparison. The Gold IRA Comparison Workbook can be adapted to compare provider, custodian, LLC, dealer, and storage charges side by side.

Red Flags Across Self-Directed IRA Providers

Red flags are reasons to pause and verify. They are not automatic findings about Broad Financial or any named provider.

- The provider and custodian are described as the same party. A facilitator or document provider should not be assumed to be the IRA custodian.

- Fees are split across several documents. Every provider, custodian, state, bank, dealer, depository, and professional fee should be combined into a total-cost worksheet.

- Custodian acceptance is presented as investment approval. Investor.gov states that a self-directed IRA custodian may not evaluate the underlying investment — administrative acceptance is not investment due diligence.

- Checkbook control is presented as an exception to IRA rules. An LLC does not remove prohibited-transaction, collectible, custody, valuation, distribution, or reporting rules.

- Home possession of metals is presented without independent review. The IRS physical-possession rule and the McNulty outcome should be addressed in writing before any metal is stored, received, or controlled personally.

- Related-party transactions are treated casually. A transaction involving the account owner, family members, controlled businesses, service providers, personal guarantees, personal labor, personal use, or indirect benefit should receive professional review.

- No ongoing compliance plan exists. Formation documents are only the start — annual valuations, state filings, bank records, investment records, tax forms, distributions, RMD planning, and entity maintenance may continue for years.

Questions to Ask Before Opening an Account

- What is the provider's full legal name, and is the company the custodian, administrator, facilitator, or LLC-document provider?

- What is the independent custodian's legal name, and which entity holds the IRA account?

- Which entity prepares the LLC documents, and who provides tax or legal advice (if anyone)?

- What services are excluded?

- What is the complete first-year cost and the expected annual cost after setup?

- Which fees are paid to third parties, and which state LLC fees apply?

- Who serves as registered agent, and who opens and controls the LLC bank account?

- How must the bank account be titled, and which signatures are permitted?

- Which transactions require custodian approval, and which occur directly through the LLC?

- How are prohibited transactions reviewed, and how are related parties identified?

- How are assets valued each year, and which tax forms may be issued or required?

- How are distributions and in-kind distributions processed?

- For metals, which trustee or depository has physical possession, and has the custodian confirmed product and custody eligibility?

- How are storage, insurance, and audits documented?

- What happens if the LLC is dissolved, and what transfer-out and termination fees apply?

- Which public records match the legal entities, and will every material answer be supplied in writing?

The Gold IRA Quiz can help organize research topics but does not determine whether a structure is appropriate.

Frequently Asked Questions

What is Broad Financial?

This article does not state a current Broad Financial service description as a verified fact because the live research did not retrieve enough current primary-source material to confirm the company's legal entity, pricing, custodian relationship, or service terms as of July 2026. Current company and custodian documents should be reviewed directly.

Is Broad Financial an IRA custodian?

No custodian claim is made here. A self-directed IRA provider may be a custodian, administrator, facilitator, document provider, or coordinator. The custodian's exact legal name and account agreement should identify the regulated account administrator.

What is a checkbook IRA?

A checkbook IRA generally uses an IRA-owned LLC with a bank account that allows the LLC manager to execute certain transactions. The structure remains subject to IRA rules, prohibited-transaction rules, custody requirements, entity law, and account documentation.

Is an IRA LLC allowed to hold gold at home?

No broad approval should be assumed. The IRS states that qualifying bullion must be in the physical possession of a bank or approved nonbank trustee. The McNulty case involved adverse tax treatment when IRA-owned coins were personally held at home. Independent tax and legal review is essential.

Does custodian approval mean an investment has been checked?

No. Investor.gov warns that self-directed IRA custodians generally do not investigate or evaluate the investment merely because it is accepted for account administration.

Which fees should be compared?

The comparison should include provider setup, LLC formation, state charges, registered agent, custodian setup and annual administration, transaction fees, asset fees, banking costs, dealer charges, storage, insurance, valuation, distributions, transfer-out, and termination.

Conclusion

A useful Broad Financial review should not rely on a single rating, marketing statement, or fee number. The stronger method confirms the legal entities, separates the provider from the custodian, maps the IRA-LLC and bank-account roles, collects every fee, reviews prohibited transactions, verifies asset custody, and preserves independent tax and legal advice. No Broad Financial fees, complaint totals, BBB ratings, custodian relationships, or service terms are asserted here because current primary-source verification was incomplete as of July 2026. Public records can change — each record should be re-checked directly. A public rating or complaint count does not determine whether a company is appropriate for any individual.

Sources

- Internal Revenue Service. Retirement Plans FAQs Regarding IRAs.

- Internal Revenue Service. Retirement Topics — Prohibited Transactions.

- Internal Revenue Service. Investments in Collectibles in Individually Directed Qualified Plan Accounts.

- Investor.gov. Self-Directed IRAs and the Risk of Fraud.

- Journal of Accountancy. Gold Coins Kept at Taxpayer's Home Caused Taxable IRA Distributions (McNulty v. Commissioner).

- Better Business Bureau. Overview of BBB Ratings.

- Better Business Bureau. Complaint Process.

- Federal Trade Commission. ReportFraud.ftc.gov.

- National Association of Attorneys General. Find My AG.

Article reviewed and edited by Daniel M. — editor, 401kToGoldIRA.org. A neutral verification framework sourced to the IRS, Investor.gov, the Journal of Accountancy (McNulty), the BBB, FTC, and NAAG; educational only, not an endorsement, verdict, or tax or legal advice.