Educational framework, not a ranking or endorsement: This page does not name a "best" company or publish a numbered ranking. It gives verifiable criteria to evaluate any provider. Some links on this site may be sponsor links, and the site owners may be compensated if customers request information from companies mentioned; that material connection does not change the framework, and readers should verify every fact independently. Customers should speak to a financial or tax advisor before making decisions. Goldco does not offer tax or legal advice. Past performance does not guarantee future results.

Regulators advise customers to compare spot value, retail price, dealer spread, commissions, storage, insurance, and the amount available from an immediate resale. They also warn that a self-directed IRA custodian normally holds and administers assets but does not evaluate the quality of the metal purchase or the promoter (FINRA: 10 Things to Ask; Investor.gov: Self-Directed IRAs and the Risk of Fraud).

Best Gold IRA Investment Companies: Why "Best" Depends on the Account

The phrase "top gold IRA companies" can suggest that one list works for every retirement saver. In practice, the decision can change with the amount being transferred, the products requested, the need for phone support, the desired storage arrangement, and the importance of written pricing before a call. A company with a high purchase minimum may not fit a smaller account. A company with a low stated minimum may still have a wide dealer spread or higher long-term fees. A provider with strong educational material may not publish every price online, while another may publish more data but offer fewer service options. The word "best" is therefore a conclusion reached after comparing documents — it is not a fact created by a star rating, an advertisement, or a prominent position on an affiliate page.

Affiliate funding also deserves attention. The FTC states that an affiliate marketer earning a commission from a purchase link should disclose that relationship clearly and close to the recommendation so readers can decide how much weight to give the endorsement (FTC: Endorsement Guides). An affiliate relationship does not prove that a comparison is inaccurate — it creates a material connection that should be visible before the company recommendation or call to action. A useful comparison explains how companies were selected, whether compensation affects placement, which facts were checked, and when company records were last reviewed.

Understand the Three Main Parties

A Gold IRA company comparison becomes clearer when the roles are separated.

Precious-Metals Dealer

The dealer sells the coins or bars, and sets the retail price, product premium, spread, sales compensation, and any internal buyback policy. FINRA and the CFTC recommend obtaining all prices, fees, commissions, and repurchase terms in writing before payment (CFTC: 10 Things to Ask).

Self-Directed IRA Custodian

The custodian establishes and administers the IRA, processes directions, maintains records, and reports required account information. Investor.gov states that self-directed IRA custodians generally do not sell the asset, provide advice, evaluate the legitimacy of the promoter, or verify the financial information supplied for the asset. The IRS maintains a list of approved nonbank trustees and custodians and states that the list is updated as entities are added or removed; banks may also serve as IRA custodians under applicable rules (IRS: Approved Nonbank Trustees and Custodians). A custodian relationship should not be treated as an endorsement of a dealer or metal product.

Depository or Storage Facility

The storage facility holds the physical metal under the custodian's arrangement. The IRS states that qualifying bullion must be in the physical possession of a bank or approved nonbank trustee, and that the same rule applies when an IRA-owned limited liability company acquires the metal (IRS: Retirement Plans FAQs Regarding IRAs). The comparison should identify the legal custodian, the physical storage facility, the storage type, insurance disclosures, annual charges, and distribution process. Customers should speak to a financial or tax advisor before making decisions involving allocation, a rollover, IRA custody, distributions, or taxes. Goldco does not offer tax or legal advice.

The Verifiable Criteria That Actually Matter

The following criteria can be checked without relying on a company's claim to be among the best precious metals IRA companies.

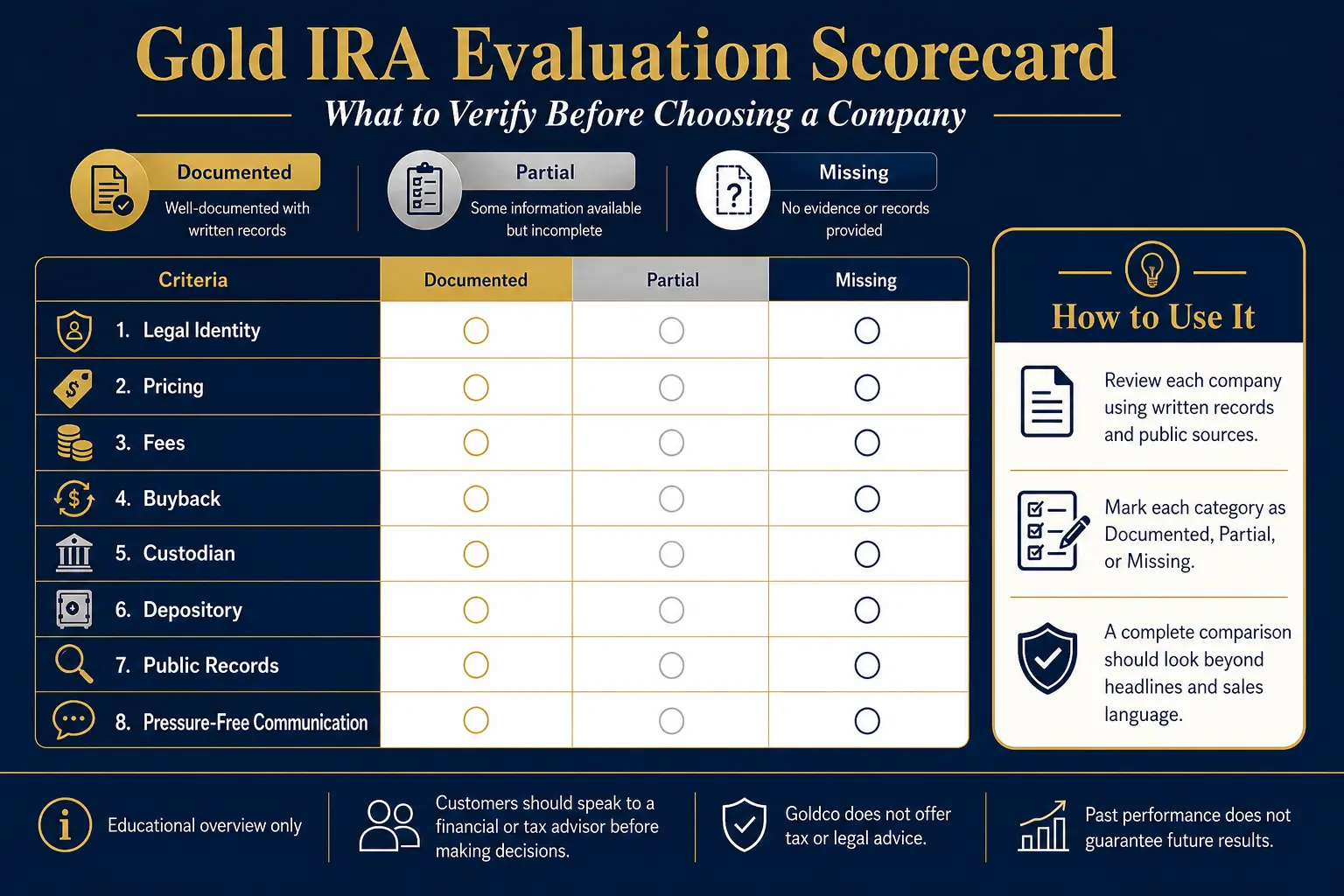

1. Legal Identity and Operating Record

The file should contain the company's exact legal name, physical address, telephone number, website, state registration, ownership information when public, and payment instructions. FINRA and the CFTC advise checking a dealer's physical address, operating history, owners or salespeople, state attorney general, state securities regulator, and relevant professional registration records; retail physical-metal dealers are not regulated at the federal level in the same way as securities brokerage firms. A salesperson claiming to provide regulated investment, securities, or commodity advice should be checked through the matching regulator, such as FINRA BrokerCheck, the SEC or state adviser database, or NFA BASIC when derivatives activity is involved (Investor.gov: Check Out an Investment Professional).

2. Clear Product Identification

Every quote should identify the metal, mint or manufacturer, product name, weight, purity, quantity, and condition. A quote that groups several products into one total can make the true premium difficult to measure. FINRA distinguishes standard bullion from rare or collectible coins and states that "semi-numismatic" is an industry label without a special standard meaning, and notes that collectible products can be less liquid than bullion. The IRS generally treats metals and coins as collectibles, with limited exceptions for certain coins and qualifying bullion held under the required custody arrangement (IRS: Investments in Collectibles).

3. Written Retail Pricing

The product quote should show the spot value, retail price, dollar premium, percentage premium, dealer compensation, and total purchase amount. The CFTC defines spot as the cash price for immediate delivery and explains that a dealer normally sells above spot and buys below spot — the difference is the dealer spread. A simple premium calculation is: Premium percentage = (retail product price − metal spot value) ÷ metal spot value × 100. The spot quote and retail quote should use the same timestamp; a later spot price can distort the result.

4. Immediate Repurchase Quote

A buyback policy should not be judged only by words such as "easy," "liquid," or "no hassle." The useful number is the amount the company would pay to repurchase the same product at the time of the purchase quote. FINRA and the CFTC recommend asking what the dealer would pay if the metal had to be sold back the next day; the gap between the all-in purchase amount and the immediate repurchase amount shows the transaction's starting spread. The written buyback terms should state whether repurchase is optional for the company, how the price is calculated, when the quote becomes final, whether the company repurchases every product it sells, minimum transaction amounts, shipping/insurance/wire/processing charges, and the expected settlement time. A dealer buyback program is a business policy, not an IRS feature of a Gold IRA.

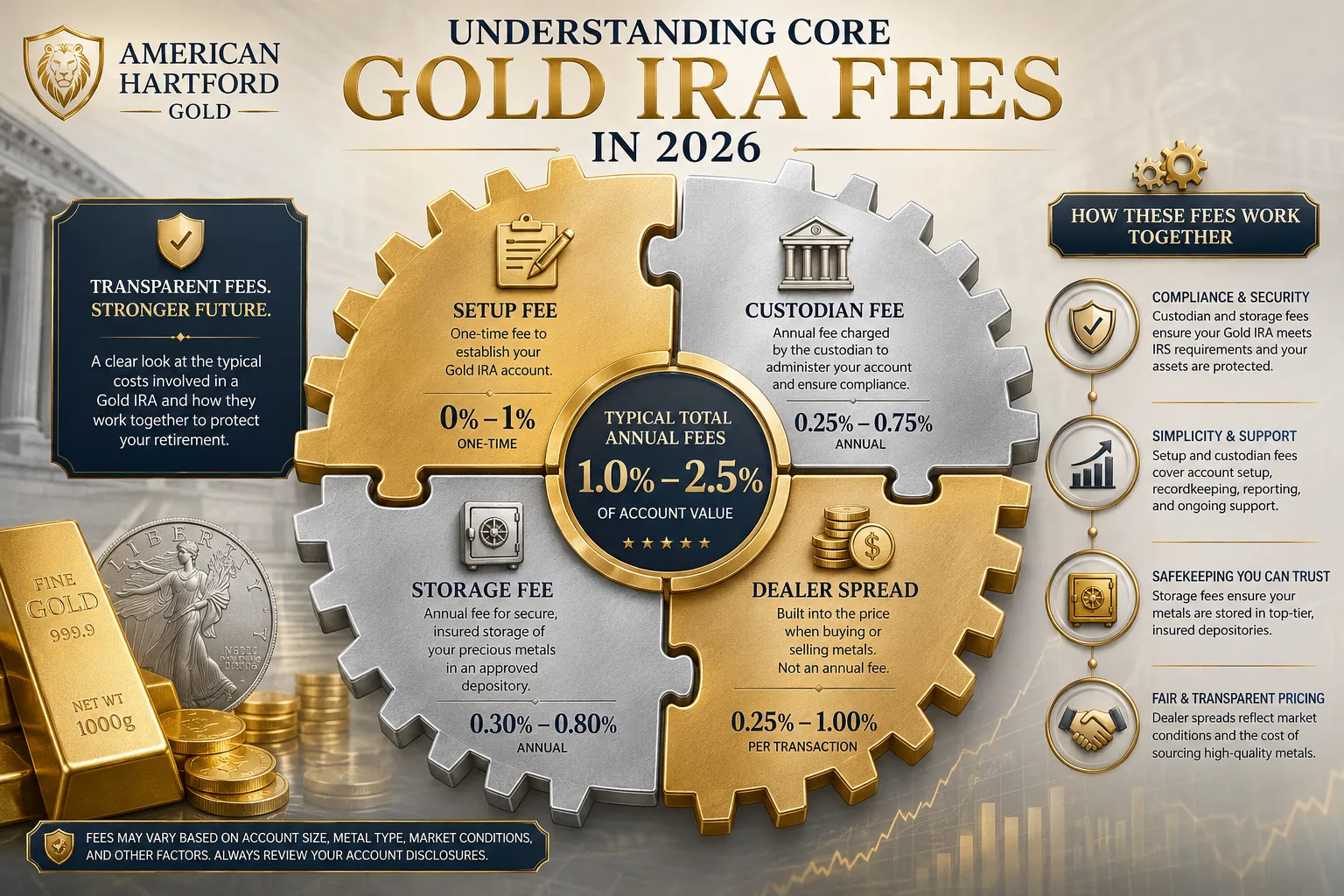

Fees, Minimums, and Pricing Transparency

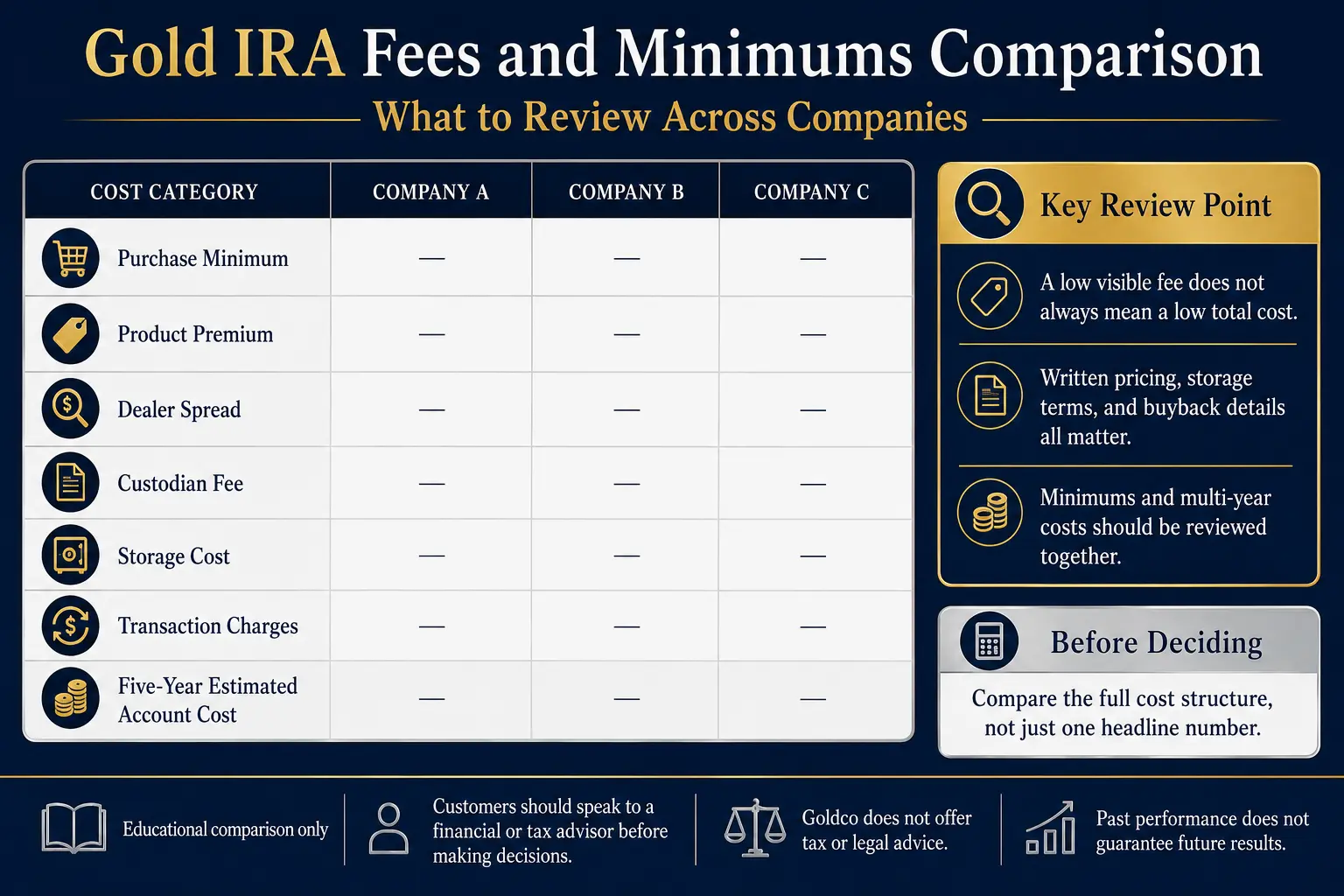

Compare the Full Cost, Not One Fee

Self-directed IRA expenses can include account setup, annual administration, asset-specific charges, storage, insurance, wires, transactions, distributions, transfers, and account closing. Investor.gov states that self-directed IRA fees can be significantly higher than fees for other investment accounts and that fee structures vary among custodians. FINRA also identifies storage, insurance, administration, and possible tax consequences as costs that should be considered alongside the dealer price. A fair comparison separates four cost layers: dealer product premium and spread; custodian establishment and administration charges; depository storage and insurance charges; and future sale, shipping, distribution, transfer, and closing charges. The Gold IRA fees benchmark and Gold IRA quote checklist can help organize those figures.

Minimums Are Company Policies

A universal federal Gold IRA purchase minimum could not be verified in the reviewed IRS, FINRA, CFTC, or Investor.gov guidance. Stated minimums should therefore be treated as company policies rather than general Gold IRA rules. A gold IRA company minimum should be confirmed on a dated company page or in a written email, stating whether the minimum applies to account funding, the first precious-metals purchase, each future transaction, or a specific promotional program. Minimum size should be compared with annual fixed fees: a small account can face a larger percentage cost when fixed charges are spread over fewer assets, while a large account can face higher dollar charges when storage or administration is based on asset value.

Compare Five- and Ten-Year Costs

A one-year fee sheet may not show the long-term effect of recurring charges. A written model can include first-year setup and transaction costs, annual custodian charges, annual storage and insurance, assumed future transaction frequency, distribution or liquidation cost, and transfer or termination fee. No unsourced market-wide average is needed — each provider can be modeled from its own dated fee schedule.

Custodian, Depository, and Buyback Disclosure

Custodian Verification

The best gold IRA custodian for one account may not fit another. The custodian should support the intended products, depository, service level, beneficiary setup, valuation process, distributions, and fee model. The IRS approved-nonbank list is a useful verification source for nonbank custodians, but Investor.gov notes that it is not a complete list of every possible custodian, so a missing name requires additional research rather than an automatic conclusion. The account documents should identify which party performs each task and which fees belong to the custodian rather than the dealer.

Depository Disclosure

A provider should name the depository, facility location, storage arrangement, insurance disclosure, audit description, shipping process, and in-kind distribution procedure. The phrase "approved depository" should not replace custodian verification: the IRS directly approves nonbank trustees and custodians, while the custodian's program documents identify the storage facility used for the IRA. The Gold IRA company comparison database can be used to place custodian and storage disclosures beside dealer pricing.

Buyback Disclosure

A gold IRA company buyback statement should be tested with a number, not accepted as a broad promise. The scorecard should capture the immediate repurchase price, pricing formula, refusal rights, quote duration, product limits, transaction minimum, shipping responsibility, and settlement method — and the same questions should be asked of every provider.

Complaint Records and How to Read Them

BBB Ratings Are One Data Point

BBB states that its letter rating is its opinion about how a business is likely to interact with customers. BBB ratings are not a promise of reliability or performance, and customer reviews are not included in the letter-grade calculation (BBB: Overview of Ratings). BBB accreditation and the BBB letter rating are separate measures, and BBB states that many good businesses are not accredited and that non-accredited businesses may still cooperate with the complaint process (BBB: How Complaints Are Handled). A gold IRA company ratings review should record the observation date, letter rating or no-rating status, accreditation status, complaint count and reporting period, complaint topics, company responses, closing status, and customer-review count and date range. A public rating or complaint count does not determine whether a company is appropriate for any individual.

Review Counts Need Context

The FTC's Consumer Reviews and Testimonials Rule, effective October 21, 2024, addresses deceptive practices involving fake reviews, paid sentiment, review suppression, and false indicators of influence (FTC: Consumer Reviews and Testimonials Rule). A large review count is not enough on its own — the review dates, platform rules, verified-transaction controls, response patterns, and repeated wording should also be examined, and company-owned testimonials should be separated from independent platform reviews. The absence of complaints does not prove that no customer has experienced a problem, since records can have limited reporting windows, jurisdiction rules, and voluntary participation.

Red Flags and High-Pressure Sales Tactics

The following are general warning signs from regulator guidance, not findings about any named company:

- Unsolicited calls, emails, mailers, or social-media messages.

- A pitch built mainly around economic fear.

- Pressure to decide during the call.

- A claim that a price outcome is certain.

- Refusal to provide fees and retail prices in writing.

- A large free-metal offer without a clear explanation of how the company earns money.

- Recommendations about product type or allocation from an unverified salesperson.

- A quote that hides weight, purity, product premium, or spread.

- Claims that the custodian has approved the quality of the purchase.

- Resistance to independent tax, legal, or financial review.

FINRA and the CFTC identify cold outreach, high-pressure sales, large markups, unclear compensation, and fear-based promotion as reasons for additional caution. The CFTC states that gold and other precious metals can be volatile and that past performance is not a reliable predictor of future returns (CFTC: Gold Is No Safe Investment).

A Written Comparison Scorecard for Any Company

The scorecard should use document status rather than a popularity score. Documented: a current written record answers the question. Partial: some information is available, but a key term remains unclear. Missing: the company has not supplied the requested document or number.

| Comparison item | Company A | Company B | Company C |

|---|---|---|---|

| Legal name and address verified | — | — | — |

| Current fee schedule | — | — | — |

| Minimum purchase policy | — | — | — |

| Exact products itemized | — | — | — |

| Spot timestamp provided | — | — | — |

| Dollar and percentage premium | — | — | — |

| Sales compensation explained | — | — | — |

| Immediate repurchase quote | — | — | — |

| Written buyback method | — | — | — |

| Custodian independently verified | — | — | — |

| Depository and location named | — | — | — |

| Storage and insurance disclosed | — | — | — |

| Five-year cost modeled | — | — | — |

| BBB and state records dated | — | — | — |

| Affiliate relationship disclosed | — | — | — |

| No-pressure research period | — | — | — |

The comparison workbook can hold supporting screenshots, fee schedules, quotes, and dated public-record notes. No total score is required — a missing price or buyback number can matter more than several positive marketing features.

Matching a Company to Account Size and Goals

Smaller accounts. A smaller account may place greater weight on the minimum purchase, fixed annual fees, product premiums, and whether the provider accepts partial rollovers. A low minimum does not automatically mean a lower total cost.

Larger accounts. A larger account may place greater weight on tiered pricing, percentage-based storage, product concentration, repurchase capacity, multiple depository locations, and service continuity.

Bullion-focused research. A customer seeking standard bullion may prioritize low premiums, narrow spreads, simple product lists, and clear like-kind buyback terms.

Specialty-product research. A customer considering collectible or specialty coins should request independent pricing evidence, grading information, resale quotes, and a clear separation between melt value and collector premium. FINRA notes that collectible products can be less liquid than standard bullion.

Service and education. Some households place greater value on patient explanations, written materials, spouse participation, and time to review documents. Pressure-free communication is a real comparison factor because a rollover can affect a long-term retirement plan. The best Gold IRA companies page can support additional research without replacing the written scorecard, and the Gold IRA quiz can help organize account size and research priorities before a company discussion. Customers should speak to a financial or tax advisor before making decisions involving retirement allocation, rollovers, IRA products, distributions, or taxes. Goldco does not offer tax or legal advice.

Frequently Asked Questions

Is there one best Gold IRA company for every account?

No. Account size, product preferences, fee structure, service needs, custodian access, storage, and buyback terms can change the fit. A fixed ranking cannot account for every household's facts.

What is the most important Gold IRA fee to compare?

No single fee shows the full cost. The comparison should include the dealer premium and spread, custodian fees, storage and insurance, transactions, shipping, distributions, transfers, and account closing.

Do Gold IRA companies have the same minimum purchase?

No universal federal minimum was found in the reviewed regulator guidance. Company minimums are business policies and should be confirmed in dated written records.

Does an IRA custodian approve the dealer or metal purchase?

Not generally. Investor.gov states that self-directed IRA custodians usually hold and administer assets but do not evaluate the quality or legitimacy of the investment or promoter.

How should a Gold IRA buyback program be compared?

The file should include an immediate repurchase quote, the pricing formula, products covered, refusal rights, quote duration, minimums, shipping, deductions, and settlement timing.

Can BBB ratings identify reputable Gold IRA companies?

BBB ratings can provide useful context, but BBB states that a rating is not a promise of reliability or performance. Complaint details, responses, public records, pricing, and written terms should also be reviewed.

Conclusion

The phrase best gold IRA investment companies is most useful as a research question, not a ranking label. A careful comparison verifies the legal company identity, exact metal products, spot value, premium, total fees, immediate repurchase amount, custodian, depository, storage, complaint records, and affiliate relationship. It also separates the dealer from the custodian and storage facility. The strongest provider for one account may not fit another: a smaller account may focus on minimums and fixed fees, a larger account may focus on tiered pricing, storage costs, and liquidation capacity, and a bullion-focused buyer may prioritize price transparency while another household places more weight on education and support. The reader reaches the conclusion after reviewing the same documents for every company. No single badge, star score, or affiliate list replaces that process. Past performance does not guarantee future results.

Sources

- FINRA. 10 Things to Ask Before Buying Physical Gold, Silver or Other Metals.

- Commodity Futures Trading Commission. 10 Things to Ask Before Buying Physical Gold, Silver, or Other Metals.

- Investor.gov. Investor Alert: Self-Directed IRAs and the Risk of Fraud.

- Internal Revenue Service. Investments in Collectibles in Individually Directed Qualified Plan Accounts.

- Internal Revenue Service. Retirement Plans FAQs Regarding IRAs.

- Internal Revenue Service. Approved Nonbank Trustees and Custodians.

- Better Business Bureau. Overview of Ratings.

- Better Business Bureau. How BBB Complaints Are Handled.

- Federal Trade Commission. FTC's Endorsement Guides: What People Are Asking.

- Federal Trade Commission. The Consumer Reviews and Testimonials Rule: Questions and Answers.

- Commodity Futures Trading Commission. Gold Is No Safe Investment.

- Commodity Futures Trading Commission. Precious Metal Frauds.

- FINRA. About BrokerCheck.

- Investor.gov. Check Out an Investment Professional.

Article reviewed and edited by Daniel M. — editor, 401kToGoldIRA.org. An evaluation framework sourced to FINRA, the CFTC, Investor.gov, the IRS, the BBB, and the FTC; educational only, not a ranking, an endorsement, or tax or legal advice.